Using Oxford Economics’ global model, we assess the potential implications for growth and inflation of three different scenarios for the conflict.

The US–Israel attack on Iran over the weekend and Iranian response has disrupted shipping in the Persian Gulf and spiked oil prices. The broader economic impact is highly uncertain, depending on how long the hostilities last and whether there is lasting damage to transport infrastructure. Using the Oxford Economics model, we trace through three different scenarios for their impacts on Australia and New Zealand. These are model results only, and do not represent a forecast of either the conflict or central bank reactions.

What is the extent of the conflict?

Over the past three days, the US and Israel have struck an array of military and infrastructure targets across Iran. Iran’s Supreme Leader Ayatollah Ali Khamenei was killed along with many other senior leaders. Iran retaliated against US military assets in the region, Israel and other infrastructure assets across the region, including Dubai’s airport. President Trump has stated that combat operations will “continue until all of our objectives are achieved”, without elaborating beyond an initial projection of “four to five weeks”. Comments from Israeli Prime Minister Benjamin Netanyahu also alluded to military strikes increasing in intensity in “coming days”.

How has regional trade been affected?

As of 3rd March, the all-important Strait of Hormuz is officially closed to oil, LNG and container trade. A few ships have reportedly been hit, and existing insurance policies have been revoked. Even if this proves short-lived, high insurance costs could stymie any quick resumption in transit. Bloomberg reports DP World has also suspended work at their Jebel Ali port in Dubai.

The conflict has also shut all air traffic across the region, affecting global passenger travel and freight until further notice, including between Europe and Australia / New Zealand.

How have financial markets reacted?

Yesterday, the price of Brent oil opened almost 14% higher at US$82.37. It has remained volatile since but currently trades just below US$78.00 (7% higher than Friday’s close). This is on top of the rise through January and February that occurred in anticipation of conflict. Spot Brent is 32% higher in US dollars than it was in mid-December.

The Australian and New Zealand dollars are little changed overall, down 0.2% and 0.9% since Friday’s close. Equity markets are cautious. Most, including Australia’s ASX 200 have seen little net change, awaiting a better sense of the duration and scale of the conflict. Though Europe’s exposure to energy supplies from the region saw a marked decline in the Continent’s bourses overnight.

How might oil prices respond?

If, as was the case in mid-2025, military conflict is short, the price of oil is likely to retreat quickly and physical trade return to normal. The hit to global trade, inflation and financial markets would be negligible.

However, if the conflict intensifies in coming days and/or persists for weeks, financial market participants are likely to become more anxious. Under these circumstances, Brent oil around US$100 is possible, with consequences for both global growth and inflation. Equities and pro-risk currencies would also come under significant pressure.

Iran produces around 4 million barrels per day (mb/d) of crude and other liquids, roughly 4% of global oil production, with China the largest import market – a manageable supply shock at the global level. The Strait of Hormuz, however, is the main route for 20mb/d of oil supply and circa 30% of global container shipping.

There is significant uncertainty over the potential for disruption, but as a guide we consider three illustrative scenarios using Oxford Economics’ global model.

- A disruption to Iranian production only could see the price of oil rise another US$25 per barrel to around US$100. However, inventory draws, a potential release of strategic reserves and/or an increase in supply from other producers would likely ease concerns and see the price of oil retreat quickly. The implications for LNG, container and air trade would also be transitory.

- If shipping through the Strait of Hormuz is affected for up to a month, Brent could instead spike to US$113 per barrel.

- A disruption of three or more months could see the price of Brent oil rise to US$185 per barrel.

The longer and more intense the disruption, the greater the real economy cost and hit to sentiment. Oil and LNG inventories held by both the private and public sector are also finite, and workarounds for supply are limited. Note, these scenarios also assume no damage to oil and LNG production and freight facilities. A permanent loss of supply would prolong the cost to the real economy and financial markets via the price of oil and related energy products.

In addition, we would also likely see lasting supply disruptions across an array of goods globally given the complex nature of global trade and manufacturing. As for oil, the longer the disruption the greater the cost. Arguably, Europe would be most affected given their exposure, but ramifications would be seen across the globe.

How might higher oil prices affect the Australian and New Zealand economies?

Higher oil prices feed rapidly into headline CPI via petrol and transport costs, and indirectly via energy-intensive products such as fertilisers. Under the three scenarios petrol prices could increase by A$0.25 to A$1.00 per litre, dependent on movements in the Australian dollar and refinery margins.

Higher inflation reduces real household disposable income, weighing on consumption, while higher input costs weaken investment. External demand also softens as global growth slows, weighing on exports, with reduced imports providing only a partial offset.

The net impact is consistently larger in New Zealand because there are no offsetting export income effects. LNG and coal prices also rise, partially insulating Australian incomes via higher export revenue, and dampening any exchange rate depreciation. However, it does not fully neutralise the drag from higher fuel costs.

How might Australia and NZ GDP growth and inflation be affected?

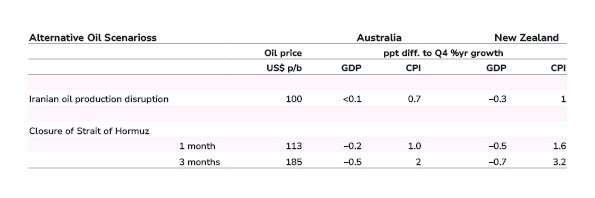

If only Iranian oil supply is impacted, the Australian CPI rises by around 0.7ppts (see table), while the near-term impact on real GDP is marginal – GDP growth at Q4 2026 is less than 0.1ppt lower.

If supply from the Strait of Hormuz is disrupted for one month, the Australian CPI lifts by around 1ppt, with GDP growth around 0.2ppt lower. A three-month disruption could see the CPI temporarily spike by around 1.5ppts at the peak, with GDP 0.5ppts lower by end-2026.

In New Zealand, the same shock transmits more forcefully as higher oil prices represent a negative terms-of‑trade and income shock. Under the Iranian supply scenario, the CPI rises by around 1ppt and GDP is circa 0.4ppts lower. With more severe disruptions, the divergence widens. A one‑month Strait of Hormuz closure raises CPI by around 1.6ppts and lowers GDP by around 0.5ppts. A three‑month disruption lifts the CPI by around 3ppts and lowers GDP by around 0.7ppts, reflecting a larger and more persistent squeeze on real household incomes.

How will the RBA and RBNZ interpret the oil price shock?

These three oil supply scenarios represent temporary supply shocks. The price level increases, not ongoing inflation. Typically, central banks look through such shocks, but in these scenarios, the RBA and RBNZ would have to balance the risk that inflation expectations lift against the medium-term effects on activity. They will also be watching for signs of pass-through of higher costs into inflation more broadly.

The conflict in Iran and related impact on oil prices adds to the risks that inflation remains higher for longer. In Australia, Trimmed Mean was already expected to remain above the RBA’s 2–3% inflation target range for a few quarters; an extended conflict would lengthen that period. Similarly, inflation would be expected to remain in the upper part the RBNZ’s target band for an extended period.

What if oil prices spike to US$100 per barrel or US$150 per barrel and remain there?

The policy risks increase if higher oil prices persist and begin to generate secondary inflationary pressures through wages and other goods and services. The Oxford Economics model represents these risks by modelling central bank actions based on a simple (Taylor) reaction rule.

If oil prices were to increase to US$100 per barrel, around US$25 above current levels and stay there, model estimates suggest it could tilt the balance of risks to the RBNZ raising rates by a further 25bps in 2027, relative to 125bp in our baseline, with rates around 25bps higher over the forecast period. For Australia, where the inflation passthrough is comparatively smaller, the balance of risks would be for rates to settle around 25bps higher over the longer term.

Under a US$150 per barrel scenario, monetary policy could diverge. Central banks could look through the first-round inflation effects given the expected negative spillovers to activity as long as inflation expectations remain anchored. However, in New Zealand persistently higher inflation, combined with a low starting point for interest rates, could lead the RBNZ to raise rates by a further 50bps in 2027, to contain ongoing core inflationary pressures. In contrast, in Australia, where interest rates are already restrictive, the drag from higher inflation on household spending and activity may allow the RBA to remain on hold with a hawkish bias.

Note: The Oxford Economics Global Economic Model is an integrated forecasting and scenario model covering 87 key economies, including Australia and New Zealand, and regional blocs. A global commodity block based on country demand and supply allows scenario analysis for price or demand and supply shocks with feedback channels back to demand, prices, monetary policy and other financial asset prices.

{kind=link}