- After hawkish Fed, dollar traders turn to preliminary PMI data.

- Pound set for a busy week amid inflation, PMI and retail sales numbers.

- Japan’s CPI to determine how likely an April BoJ hike is.

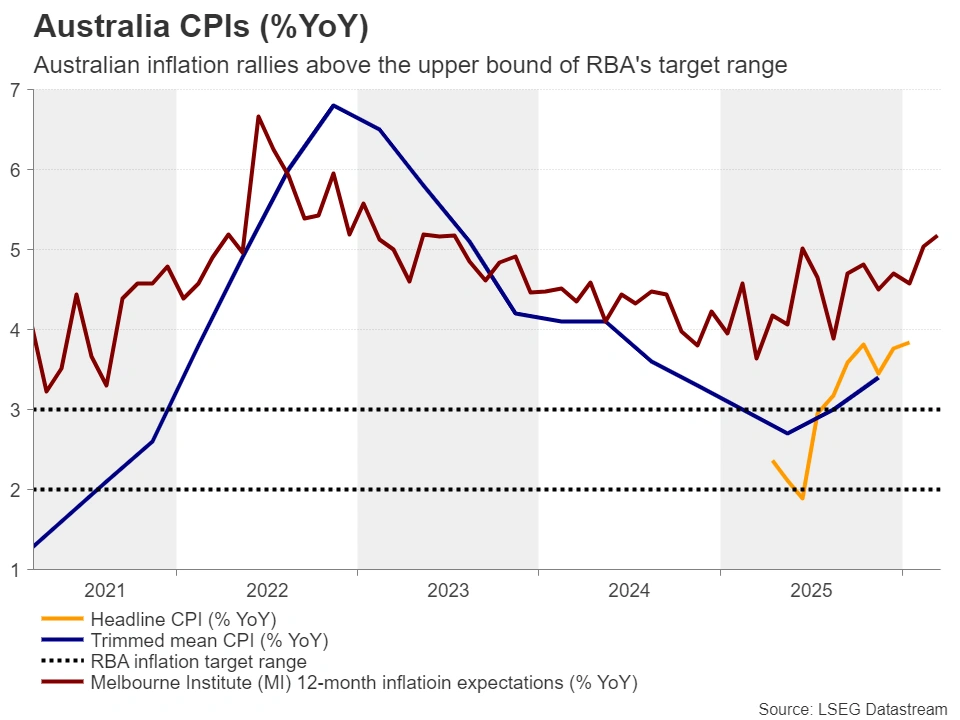

- Australia’s CPI could solidify the case for a third consecutive RBA hike.

- After the central bank spree, agenda becomes lighter.

Following a very busy week, with news about the war in the Middle East flowing continuously and seven major central banks deciding on monetary policy amidst all this geopolitical uncertainty and the profound energy crisis, the calendar becomes notably lighter next week.

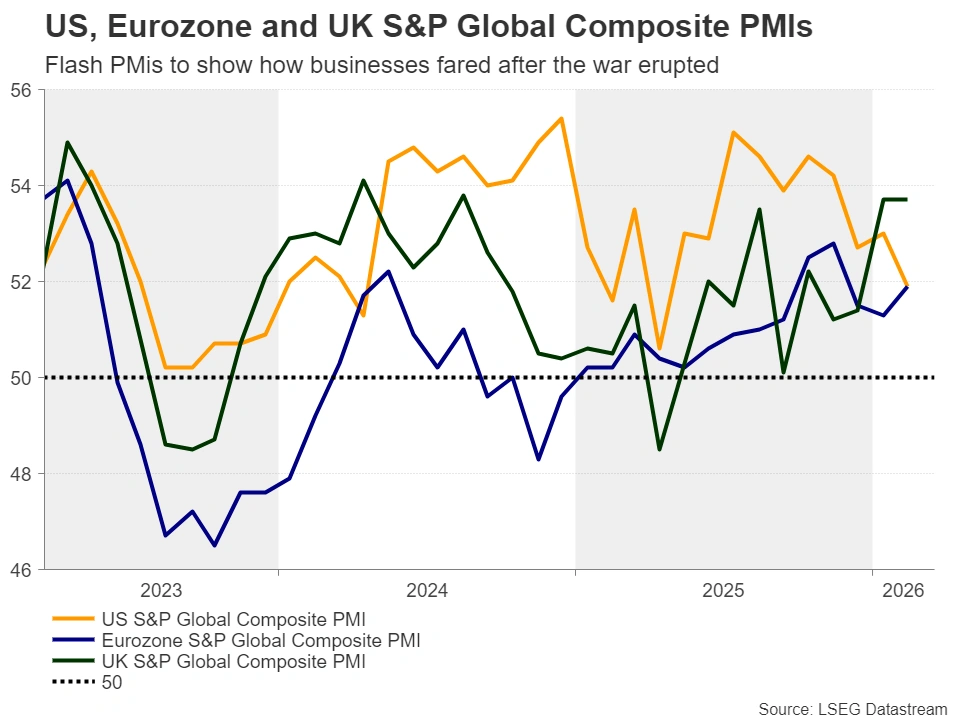

Of course, this does not mean that there are no data releases for traders to pay attention to. The spotlight may be on the preliminary PMIs for March from several major economies as they will provide a first glimpse of how business activity fared after the war erupted and what the impact of skyrocketing energy prices were.

How will the US PMIs impact Fed expectations?

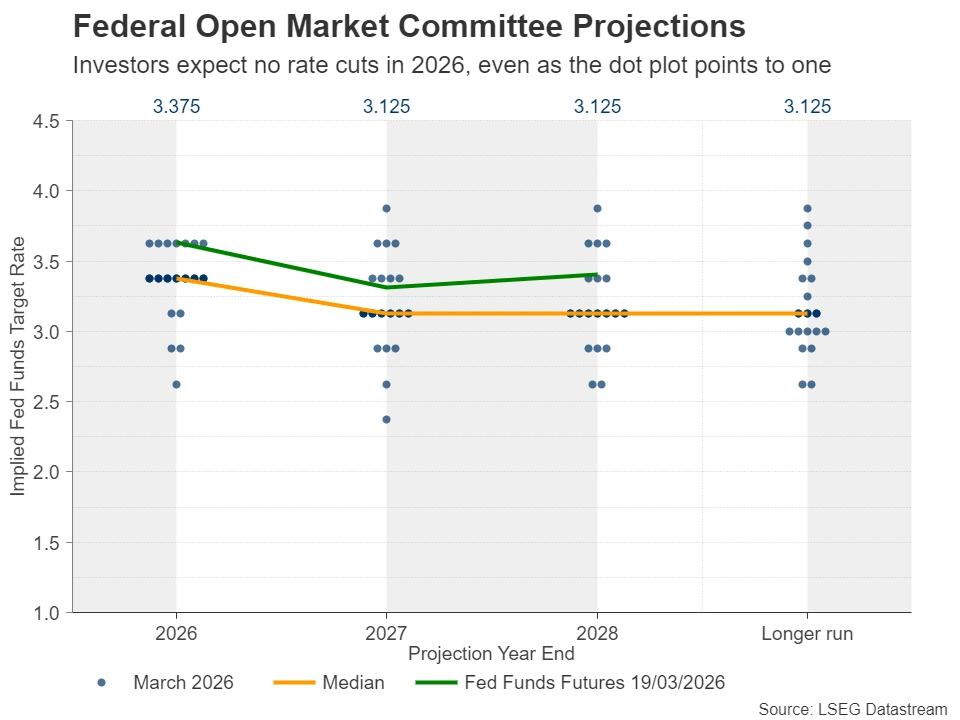

Getting the ball rolling with the US, the Fed decided to hold interest rates unchanged as expected and projected higher inflation and steady unemployment. Although the new dot plot continued to point to a single 25bps rate reduction by the end of 2026, Fed Chair Powell said that the uncertainty surrounding the rate path has increased markedly amid the war in the Middle East, and that a “meaningful” number of his colleagues are now favoring less easing than they did three months ago. Indeed, according to the plot, the number of officials favoring interest rates to remain untouched by the end of the year has increased to seven from four in December.

This prompted investors to further scale back their rate cut bets, assigning only a mere 15% chance of a quarter-point cut by the end of the year, and thereby allowing a fresh spree of dollar buying. Wall Street slipped again, while gold extended its tumble, falling below the key support zone of $4,840.

With all that in mind, should the flash PMIs, released on Tuesday, reveal that business activity was hurt severely by the energy crisis, investors will have to face a dilemma. Sell the dollar on signs of slowing economic growth or buy it due to concerns about accelerating prices charged by companies, which could lead to higher inflation and thereby an even more hawkish Fed.

Nonetheless, concerns about growth could outweigh inflation worries as productivity and profitability damage may prompt businesses to keep prices as competitive as possible. This may weigh on the US dollar as some traders become more convinced about a rate cut by the end of the year. On the other hand, a decent headline print accompanied by accelerating prices could suggest that the economy can withstand unchanged rates for a longer period of time, thereby allowing even more dollar buying.

The weekly ADP employment change could also provide a hint on how the private sector is faring as a further slowdown could translate as a first indication that businesses are indeed struggling.

Will the UK data corroborate bets of BoE rate hikes?

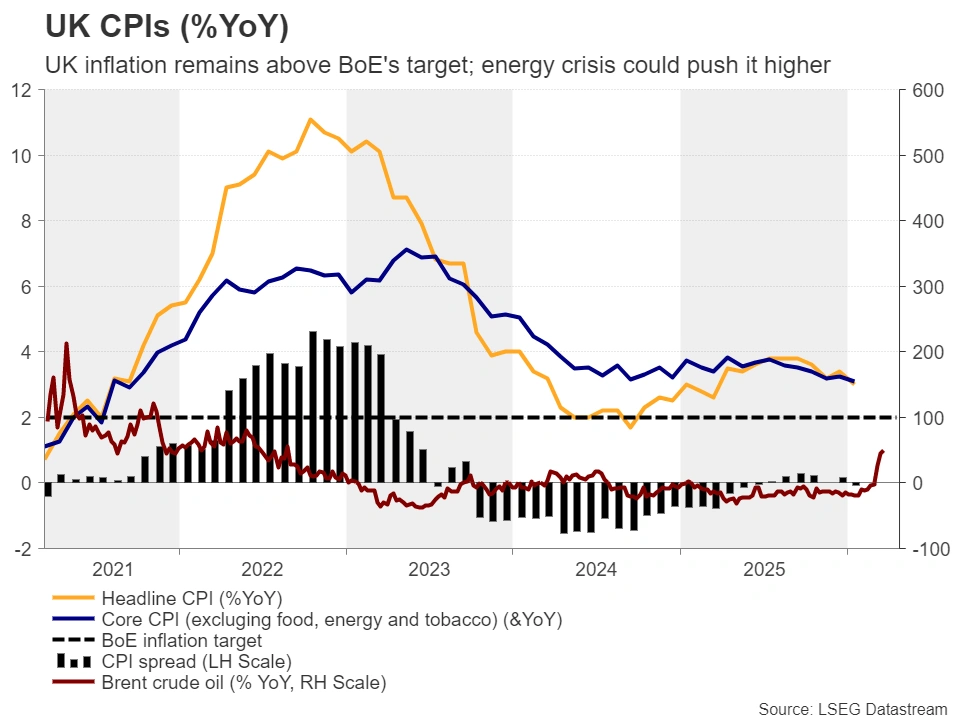

Pound traders will remain extra busy next week as, after this week’s Bank of England decision, the UK flash PMIs for March will be released on Tuesday, followed by Wednesday’s UK CPI data and Friday’s retail sales, both for February.

The BoE also stood pat this week, as the war in Iran dramatically shifted expectations away from rate cuts. What was surprising, though, was that the decision was unanimous, which means that even the most dovish members were convinced that they needed to buy some time.

With policymakers also indicating that they stand ready to act to ensure inflation’s return to their 2% objective, investors bolstered their rate hike bets, penciling in a 40% probability of a 25bps increase at the next gathering, and a total of 60bps by the end of the year. This translates into two quarter-point hikes and a decent 40% chance of a third.

Thus, should the CPI data reveal still-sticky inflation in February, and should the PMIs suggest that the skyrocketing energy prices have sent consumer prices even higher in March, the BoE’s implied path could become steeper, and the pound could recover more ground. It could even outpace the US dollar as the shift in the BoE’s rate path has been more dramatic than the Fed’s.

The euro also enjoyed some gains after the ECB adopted a similar stance to the BoE’s, highlighting the upside risks to inflation and noting that they remain determined to ensure that inflation remains near 2%.Investors are now expecting 60bps worth of rate hikes by the ECB and the Tuesday’s Eurozone PMIs could prove key in supporting or disregarding that view.

Will Japan’s inflation figures cement an April rate increase?

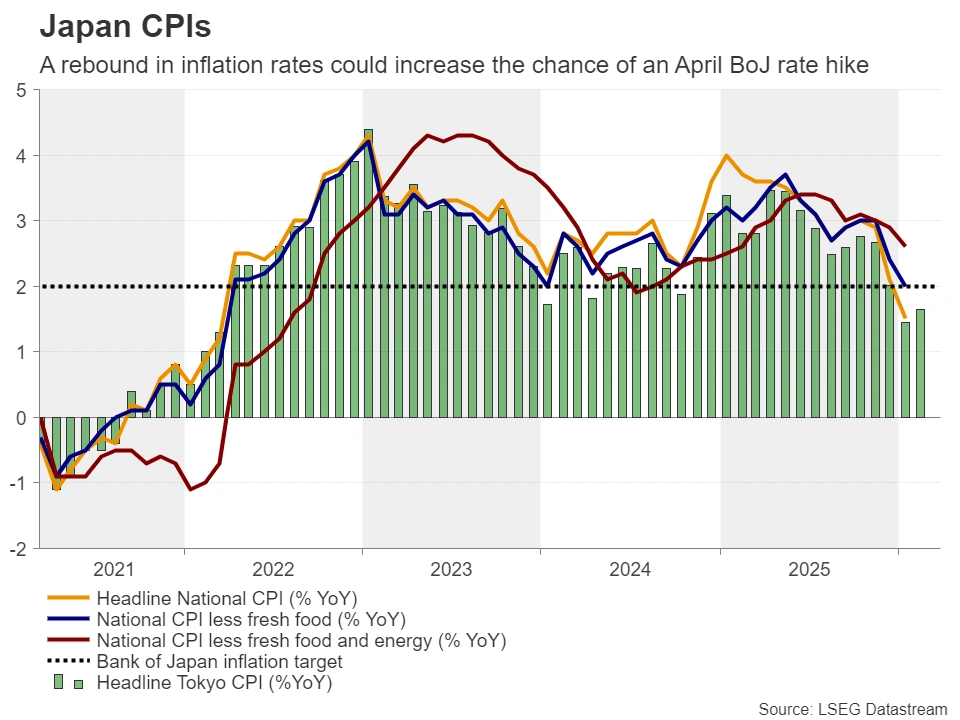

In Japan, BoJ officials also decided to remain sidelined on Thursday, but they appeared concerned about the impact of surging oil prices on underlying inflation. Board member Takata repeated his proposal to raise rates up to 1.0%, while another hawk joined him to dissent the view that inflation will durably hit 2% sometime after October, arguing that this could happen as soon as April. On top of that, Governor Ueda said he believes the outcome of this year’s spring wage negotiations may be better than previous years.

The hawkish message pushed dollar/yen slightly lower as market participants took the probability of a rate hike in April above 50%, but the already strong dollar kept the pair within the 158-160 zone, prompting finance minister Katayama to warn for the umpteenth time that they remain ready to intervene in the FX market at any time.

The next test for the Japanese currency may be the National CPI numbers for February, due out during the Asian session on Tuesday. In January, both the headline and core CPI rates slipped to 1.5% y/y and 2.0% y/y from 2.1% and 2.4%, respectively, suggesting that the upside risks to inflation stemming from the tumbling yen had yet to materialize.

A further slowdown in February could somewhat weigh on the sense of urgency for a BoJ hike in April and thereby allow further yen selling. However, this could trigger actual intervention from the finance ministry as Katayama has been very vocal about it lately. On the other hand, accelerating price pressures could corroborate the BoJ’s view and perhaps push the yen instantly higher. In any case, it seems that the risks surrounding the yen may be tilted to the upside, especially with the dollar/yen pair hovering near the 160.00 zone.

Is the RBA headed for a third straight quarter-point hike?

The RBA is the only major central bank raising interest rates consistently. After enacting a tightening cycle on February 3, delivering its first quarter-point rate hike since November 2023, the Bank decided to proceed with a back-to-back rate increase in March. Officials of this Bank also warned of a “material” risk to inflation amid geopolitical tensions in the Middle East and kept the door open to further increases.

Following the decision, the Australian overnight index swaps (OIS) market pointed to a strong chance of a third consecutive rate hike at the May meeting. The probability for another 25bps increase in May is currently standing at around 60%.

Thus, Australia’s CPI data for February could attract special attention. If the numbers point to stickier inflation even before the rally in oil prices, the probability of a May rate hike could move closer to certainty and the aussie is very likely to resume its prevailing uptrend.

{kind=link}