Canadian Highlights

- The outlook is now clouded by the Iran conflict, overshadowing signs of easing inflation.

- Retail sales showed strong momentum early in the year, but higher energy prices are set to erode real spending in the coming months.

- Core inflation was near target with excess capacity in the economy, giving the BoC some buffer as the energy shock hits.

U.S. Highlights

- Energy markets remain volatile as physical damage and data opacity deepen uncertainty around the Middle East conflict.

- The Fed held rates steady, emphasizing caution as higher oil prices complicate the inflation outlook.

- Softer housing data underscore growing sensitivity to higher yields and tighter financial conditions.

Canada – What Might Have Been

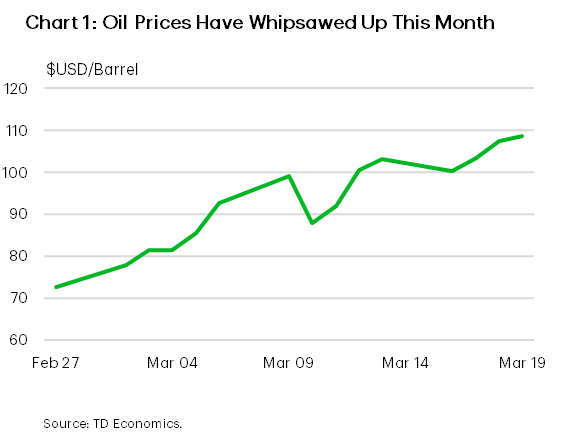

This week’s data releases and Bank of Canada (BoC) statement describe a world that could have been, with a domestic backdrop that showed signs of easing inflation. The war in Iran has upended that. With escalatory strikes on energy infrastructure this week, WTI oil prices are holding at $94 (as of the time of writing). All the focus is now on how big and persistent the energy shock will be – with the prospect of stagflation looming.

It is unfortunate that households and businesses will face this new pinch, because this morning’s retail sales data sent some positive signals. Real volumes posted a solid gain in January, taking the three-month gain to 7.7% (annualized) and February’s preliminary estimate of the nominal figure showed another solid month could be expected. After a year of fits and starts, it looks like things were just starting to turn a corner. The expected surged in gasoline and energy prices in March will muddy the picture and likely eat into the real spending figures in the months ahead.

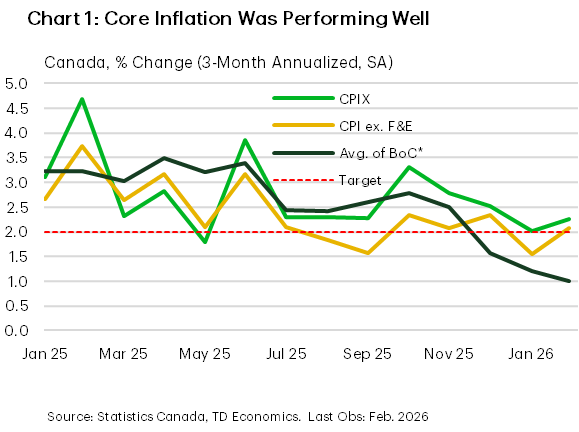

On the path of future inflation, this week’s economic news came as a silver lining. First off, it looks like inflation is going to be starting this shock from a pretty good place. Measures of near-term core inflation all showed signs of softening price momentum. The main measures were all roughly in line with the 2% target rate on a three-month annualized basis (Chart 1). Moreover, this trend has been building for a while – the rate of annualized change over the past six months showed the average of the BoC’s measures (1.7%), CPIX (2.5%) and CPI excluding food and energy (2.1%) all roughly in line with target. The positive progress suggests that officials were well on track to meet the 2% target before the most recent shock. These subdued near-term price changes despite the disruptions to supply chains from tariffs suggest that the economy is operating with some excess capacity.

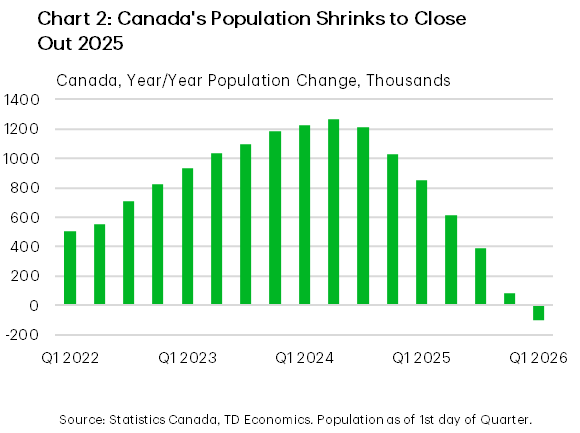

Another major development happening in the background is the country’s population turning modestly lower in 2025 (Chart 2). On the surface, declining population should help to relieve pressure on housing markets and weigh on rental growth, putting further downward pressure on shelter inflation. However, it is also leading to some tightening in labour supply, limiting spare capacity. On balance, we don’t see labour demand improving much in the coming months, but tighter labour supply will help to offset some rise in the unemployment rate.

A solid starting point for inflation and domestic excess capacity give the BoC some wiggle room to deal with the evolving energy shock. As a result, we see core measures of inflation moving only modestly higher in the coming months, before moderating into 2027. Absent a more meaningful softening in the economy, this is likely to keep the BoC on hold indefinitely.

U.S. – The Fed Pauses, Inflation Persists

Financial markets remained on edge this week as the conflict in the Middle East escalated, with uncertainty expanding into physical energy supply rather than just shipping disruptions. Reports of damage to key oil and LNG facilities in the Gulf, including infrastructure that could take months—if not longer—to repair, have injected a persistent risk premium into energy markets. Oil prices have swung sharply day‑to‑day and remain well above pre‑conflict levels (Chart 1). This dynamic remains consistent with the base case in our Quarterly Economic Forecast, but risks of even higher prices are growing. Higher gasoline prices hurt consumer spending and the prolonged uncertainty raises downside risks in energy‑importing regions. We flagged these concerns this week in our State Economic Forecast, especially for states with higher exposure to transportation, manufacturing, and energy‑intensive industries.

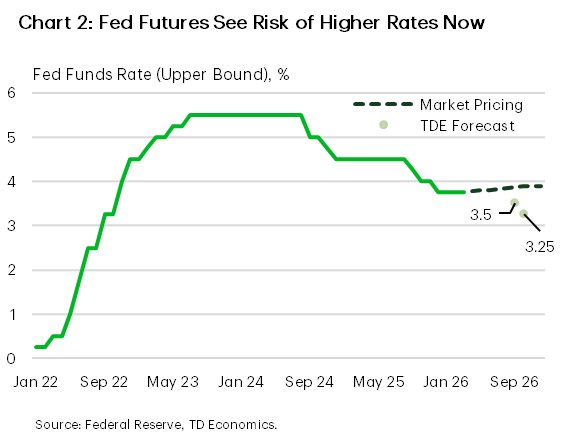

Against this backdrop, the Federal Reserve held its policy rate steady this week, as expected, but the statement was cautious. Chairman Powell acknowledged the heightened uncertainty stemming from the Middle East conflict, and revised projections showed higher inflation relative to December. The Fed continues to signal just one rate cut this year, reflecting concern that higher energy prices could slow the disinflation process at a time when core inflation is already proving sticky. Market reaction reinforced inflation concerns, with fed funds futures beginning to price a non‑trivial risk that the next move in rates may not be lower (Chart 2). Our commentary noted that the Fed appears intent on preserving flexibility, particularly given the risk that a prolonged energy shock could push the economy toward an uncomfortable mix of slower growth and firmer inflation.

Against this backdrop, markets continued to reprice risk this week in response to higher energy prices and a more cautious Federal Reserve. Equity markets struggled to find footing, while Treasury yields pushed higher as inflation risks moved back to the foreground. Incoming economic data offered a mixed picture. New home sales fell sharply in January, a reminder that interest‑rate‑sensitive sectors remain vulnerable to higher yields, though weather effects likely exaggerated the weakness. More broadly, the data flow reinforces that financial conditions are doing more of the near‑term adjustment work as the economy absorbs another external shock.

Looking ahead to next week, attention will undoubtedly remain on developments in the Middle East. Beyond the headlines, investors will also be watching how Fed officials are responding to the evolving situation and also the University of Michigan Consumer Sentiment Survey, a widely followed gauge of household confidence and inflation expectations. With energy prices and volatility high, these data could offer early signs of whether the current shock is beginning to weigh more materially on sentiment—or inflation expectations—an outcome that would further complicate the policy backdrop.

statement describe a world that could have been, with a domestic backdrop that showed signs of easing inflation. The war in Iran has upended that. With escalatory strikes on energy infrastructure this week, WTI oil prices are holding at $94 (as of the time of writing). All the focus is now on how big and persistent the energy shock will be – with the prospect of stagflation looming.){kind=link}