We are now officially entering the fifth week of the US-Iran-Israel conflict, which sent bombs flying all over the Middle East, but more concerningly, sent Global Assets flying all over.

The main culprit was Crude Oil prices – rallying about 50% since its Monthly open, the commodity hasn’t failed to contribute its fair part in overall volatility.

After sustaining a broad, inverted correlation with most asset classes and currencies, this trend appears to be abating – Traders are now really looking to relax their preceding angst with the US entering into more consistent negotiations with their enemy-counterpart in the Islamic regime, and Israel also prepares for final waves of attack to dampen the military reconstruction efforts.

Black Gold is now at a spot where uncertainty is priced in, leaving only a premium for the proper lack of supply that would traditionally go through the infamous Strait of Hormuz.

Brent has been stuck above $110 since the weekly open, and WTI remains well above $100.

WTI 4H Chart – Source: TradingView. March 30, 2026

Key levels to watch for WTI:

To the upside:

- $106 ~ Closing above could maintain further bullish pressure

- $110 ~ Psychological level not seen since the mid-March spike

- $120 ~ War highs, above this, things could get catastrophic for the economy

To the downside:

- $100 ~ Correcting back below would boost the current ease in sentiment significantly

- $90 ~ Short-term momentum turns bearish for the commodity, Markets should pick up their rebound

- $85 ~ Any move below this would confirm that the situation is indeed not worsening, best sign for Markets – Every asset becomes a buy on a daily close below.

Oil rising isn’t such a surprise to most of us, but the more peculiar change in today’s flows comes from the fact that at a despite this rise, Bonds are rallying (yields lower – implying lower inflation expectations), Stocks bounced, but seem to remain under pressure (at least, not worsening for now) and Metals have formed what a more consistent bottom.

finviz perf 3003

An Unfamiliar Session in Markets – Courtesy of Finviz

If anything was dampening Market mood throughout last week, it was the fact that failed diplomatic attempts could not generate a much larger continuum of tranquility.

But if the current, more realistic, conversations really turn into something positive, the 5-week period could be precise, and next week could be a great opportunity to join a bounce.

It is, of course, very early to say, considering that the US President and his Administration are so unpredictable, and it would be a mistake to assume that the Iranian regime is not.

In any case, month-end is approaching and could bring significant changes to the flows Participants have been accustomed to throughout this long and crazy March.

US Treasuries are rallying, the most optimistic sign

US Bonds (and Fixed Income in general) were among the worst performers across all asset classes this month, under intense pressure from rising inflation expectations.

With the tumble in Fixed-Income (and rising yields), Bond Vigilantes were pricing out all types of Rate Cuts across the globe, implying that the repercussions of rising Oil would prevent lower rates and even lead to some Monetary Policy rises (as seen in Europe and England).

Why is it important to check bonds in this environment? This asset class is the most reactive to risk news and inflation expectations – If they ease, other assets will be subject to much less constraints (as Stocks tend to see delayed bounces in such an environment).

US Bonds since beginning March – Courtesy of Finviz

Despite their morning bounce, they still have a lot to recover, and their bounce is proving challenged by the fresh bid in Oil.

- For the 30Y Yield, keep a close eye on 5.00% to the upside, 4.75% to the downside.

- For the 2Y Yield, 4.03% to the upside (+ hikes priced in) and 3.75% to the downside.

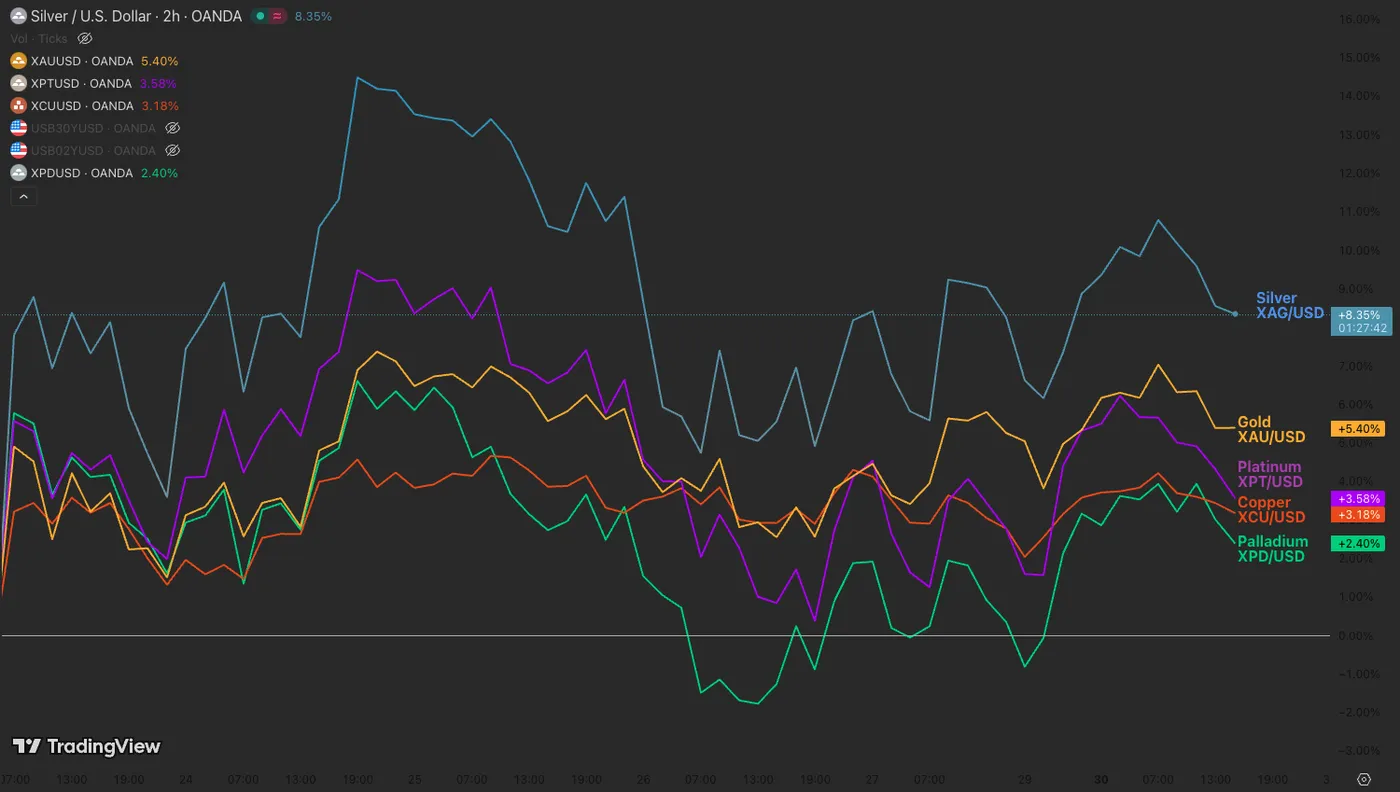

Metals rebound but still under pressure

Metals performance since last Monday – Source: TradingView

Metals have indeed marked their bottom, but the rest will be to see if they can actually maintain a higher path for longer.

Their nature as diversification asset hold them in the middle of two different narratives –

- Are they going to rally from the lower hike pricings?

- Are they going to resume their drops from the drop in uncertainty?

In this mix of fate, it seems that rangebound conditions may prevail in the precious commodities until a breakout follows.

The US Dollar remains on top of its game

Despite the easing narrative, the US Dollar remains a top-dog in this weekly open.

The Dollar Index is pointing towards a breakout, but failing here may also form a double-top, so expect this monthly close to be a significant indicator for what’s to come for FX Markets in April.

Dollar Index 4H Chart – Source: TradingView. March 30, 2026

The direction is for now difficult to predict, with the latest rally being very persistent – So the best is to wait for confirmation.

Rejecting back in the 100.30 resistance should see continuation to the downside.

Breaking and closing on the month above 100.60 could lead to a larger USD breakout.

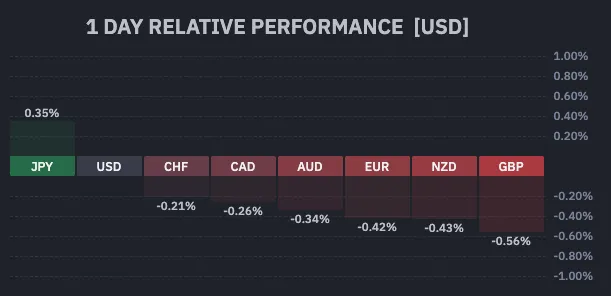

The current FX Session – Courtesy of Finviz

Markets are repricing an imminent FX Intervention for the JPY, prompting its outperformance in today – Apart from it, the US Dollar is flawless in its daily rally.

Month-end flows (throughout the session tomorrow) will be a preview of what’s to come!

Safe Trades and keep track of the conflict progress throughout this week!

{kind=link}