The ceasefire between the US and Iran has reset the Fed outlook, shifting market focus away from near-term inflation data toward the broader policy path. With oil prices falling and supply risks easing, the markets could be willing to look through both FOMC minutes today and a likely elevated March CPI reading on Friday.

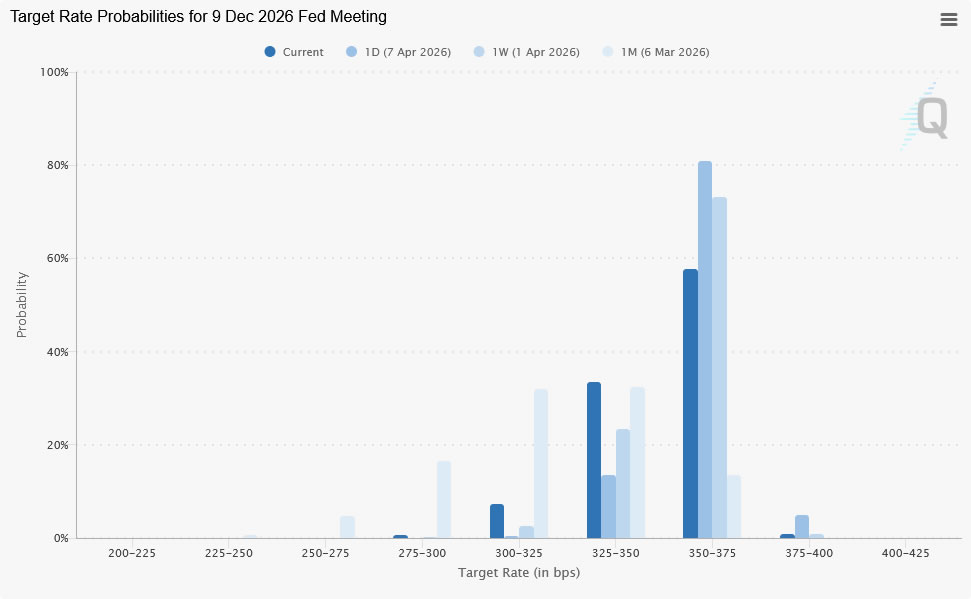

The repricing has been swift. Odds of the Fed holding at 3.50–3.75% through year-end have dropped from around 80% to near 58%, with roughly 42% now pricing in at least one rate cut. More importantly, the possibility of a rate hike has been effectively erased. This marks a clear transition from a higher-for-longer mindset toward a more balanced outlook. Just days ago, markets were positioning for a prolonged inflation shock driven by surging energy prices. That narrative has now been disrupted.

As a result, this week’s key events are losing relevance. The March FOMC minutes, due today, will likely reflect a Fed grappling with a potential wartime shock, with oil prices approaching $120. Even if the tone appears hawkish, markets are expected to largely ignore it. The reason is straightforward. The primary driver behind that hawkish stance—the risk of sustained energy disruption—has been partially resolved. The ceasefire has effectively reset the clock, rendering the minutes outdated upon release.

The same logic applies to CPI. March inflation is almost certain to print high, capturing the peak of the energy shock. But with Brent already down sharply, markets are set to treat the data as rear-view mirror inflation, focusing instead on forward-looking indicators.

However, the disinflation path is not immediate. The reopening of the Strait of Hormuz is gradual, with shipping networks expected to take six to eight weeks to normalize. During this period, oil prices are likely to remain elevated, sustaining some inflation pressure in the near term.

This creates a transitional phase where inflation remains firm, even as the underlying drivers begin to fade. But importantly, many Fed officials are likely to view this as transitory. As long as inflation expectations remain anchored, policymakers can afford to look through short-term volatility. This supports a patient stance in the near term while keeping the door open for easing once the temporary effects dissipate.

By early second half, the data should begin to reflect a clearer disinflation trend if traffic through the Strait of Hormuz is fully normalized. As base effects from the energy shock roll off and supply conditions improve, the case for Fed’s monetary policy normalization will strengthen. That makes a year-end rate cut a logical baseline scenario.

However, this repricing remains highly conditional. Vice President JD Vance described the ceasefire as a “fragile truce”, underscoring the risk that the current optimism may prove premature. Execution risk is particularly high around the Strait of Hormuz. Iranian Foreign Minister Abbas Araghchi noted that passage is currently managed “via coordination with Iran’s Armed Forces.” Any disruption or miscalculation could quickly reintroduce war premium.

For now, markets are effectively priced for perfection. Dollar has come under broad pressure, reflecting the shift in expectations, while risk currencies are benefiting from improved sentiment. Ultimately, the Fed itself has not changed—but the environment around it has. The path toward rate cuts is now visible, but it depends on sustained, tangible progress in the US-Iran negotiations. Until then, markets will continue to price easing cautiously, with one eye firmly on geopolitics.

In currency markets, Dollar is the clear underperformer today, with broad-based selling pressure. Loonie follows as the second weakest, weighed down by falling oil prices, while Yen also lags. On the other side, Kiwi leads gains, supported by RBNZ’s hawkish hold, followed by Sterling and Swiss Franc. Euro and Aussie are trading in the middle of the pack.

In Europe, at the time of writing, FTSE Is up 2.96%. DAX is up 5.14%. CAC is up 4.75%. UK 10-year yield is down -0.215 at 4.623. Germany 10-year yield is down -0.177 at 2.909. Earlier in Asia, Nikkei rose 5.29%. Hong Kong HSI rose 3.16%. China Shanghai SSE rose 2.03%. Singapore Strait Times rose 0.81%. Japan 10-year JGB yield fell -0.046 to 2.364.

Silver to Rally Toward 84 on Ceasefire Euphoria—Is “Day 10” a Trap?

Silver has broken out on ceasefire-driven Dollar weakness, with 84 now in focus. But the rally may be time-limited, as “Day 10” of the ceasefire window could bring back risk and trigger a reversal. Read More.

RBNZ Holds, Warns of “Decisive” Hikes if Inflation Expectations De-Anchor

RBNZ kept rates unchanged—but signaled it won’t hesitate to act. A warning of “decisive” hikes has put inflation expectations at the center of the policy outlook. Read More.

Eurozone Producer Inflation Falls -0.7% mom in February on Energy Drop

Eurozone PPI fell in February as energy prices dropped, signaling easing pipeline pressures. However, core components remained firm, suggesting underlying inflation is not fully fading. Read More.

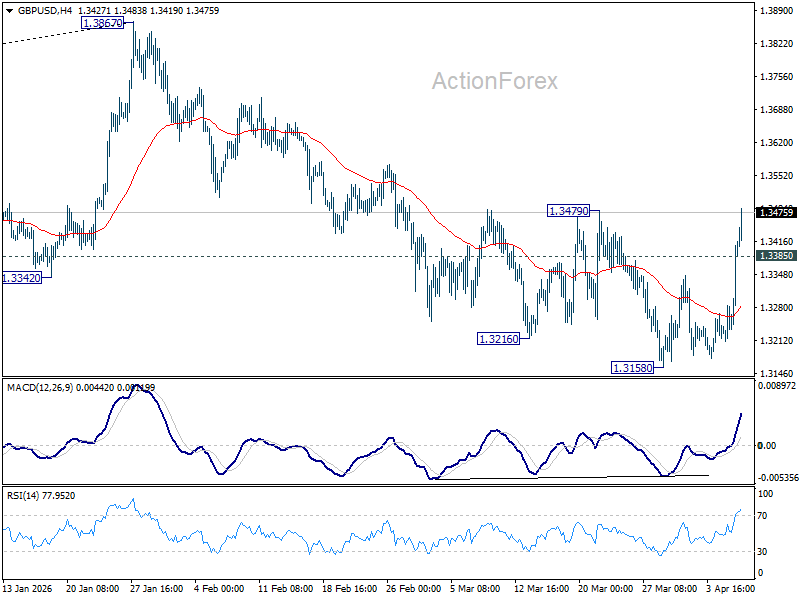

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3236; (P) 1.3268; (R1) 1.3327; More…

GBP/USD’s break of 1.3479 resistance argues that fall from 1.3867 has completed as a correction at 1.3158. Intraday bias is back on the upside. Further rally should be seen to retest 1.3867 high. On the downside, below 1.3385 will turn intraday bias neutral and bring consolidations first. But retreat should be contained well above 1.3158 low to bring another rally.

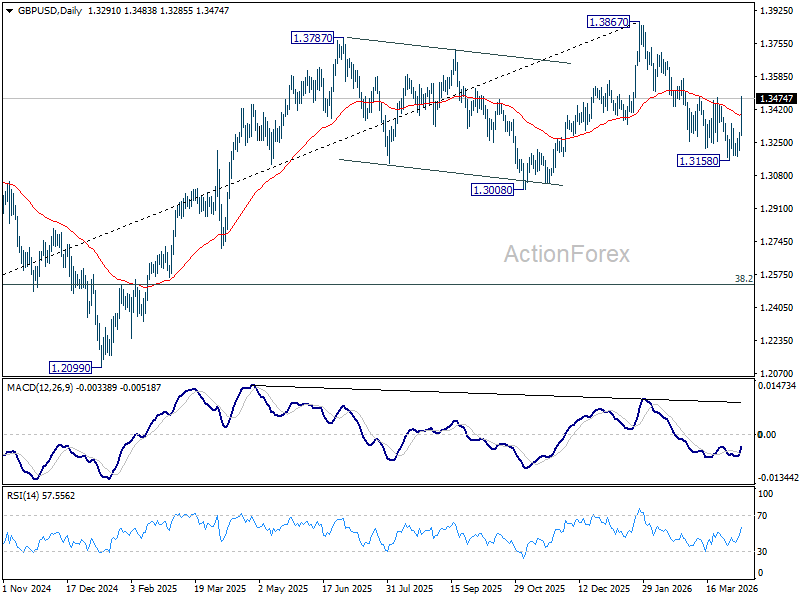

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).

{kind=link}