United States:

- Existing Homes Sales (Monday), Tax Day (Wednesday), Fed Speak (Thursday & Friday)

G10 Economies:

- Australia Employment (Thursday), U.K. Monthly GDP (Thursday)

Emerging Markets:

- China GDP (Thursday)

U.S. Week Ahead

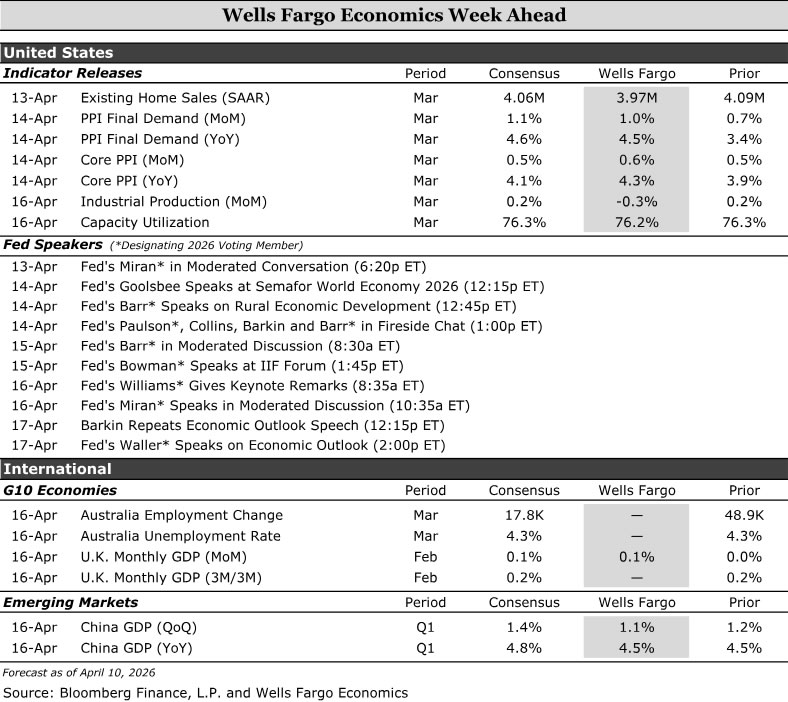

Existing Home Sales • Monday

Next week kicks off with the latest read on residential activity. The recent spurt in mortgage rates ahead of the critical spring selling season has placed housing in the spotlight. We note that existing sales measure contract closings, which typically take a month or two to complete. And so, March’s existing sales report will largely reflect conditions that predate the Iran conflict and the resulting ~40 bps increase in mortgage rates.

But even before geopolitical tensions intensified, buyer demand appeared soft on account of ongoing affordability challenges. Mortgage purchase applications declined 13% in February and rose just 6% in March. Pending home sales, which are signed contracts, did gain modestly in February. Nevertheless, the recent unexpected spike in rates are likely to lead to cancellations and mortgage qualification failures, likely resulting in a slower pace of final sales than what the pending sales number suggests. With that in mind, we expect March resales to have declined to a 3.97 million unit pace, below the current consensus of 4.06 million.

Source: NAR, MBA and Wells Fargo Economics

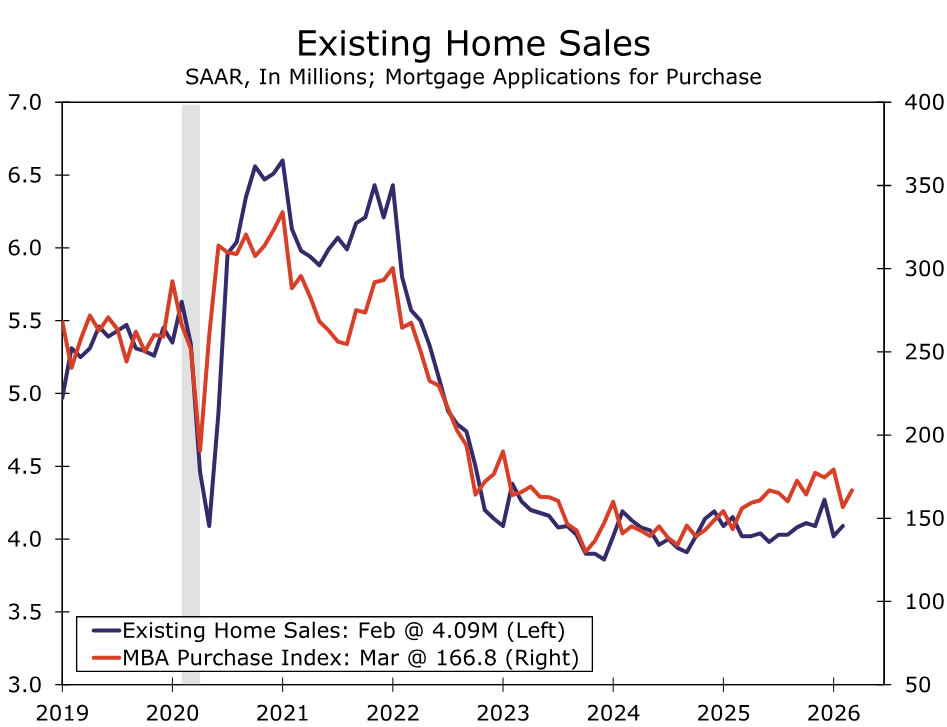

Tax Day • Thursday

Next Wednesday marks the official end to the 2025 tax season. To date, non-withheld income tax receipts (the amount of money flowing into the Treasury from households) haven’t shown any major surprises and are tracking along pretty smoothly compared to previous years (chart).

Individual income tax refunds have tracked a little lighter than we had expected at the start of tax season—around 11% higher than last year, compared to our expectation for 18% growth. Smaller than expected refunds likely means many households had lower annual tax payments, which may result in smaller April-nonwithheld tax receipts to the Treasury. We therefore expect low- to mid-teens growth for April compared to last year. Remember, smaller tax payment flow to the Treasury = smaller rise in the Treasury General Account = more benign funding market conditions for repo, etc.

Fed Speak • Thursday & Friday

There are a number of Fed speakers on the docket next week. Williams (Thurs.) and Waller (Fri.) strike us as the most noteworthy. We consider Williams as a good proxy for the more academically-minded members of the Fed. He doesn’t usually shock markets, but his comments will be closely scrutinized for signals on a higher‑for‑longer stance versus the timing of any potential cuts. He has recently stressed that policy is “well positioned,” so any subtle shift in language in the wake of the Iran conflict could be meaningful. Waller, on the other hand, isn’t shy about changing his mind publicly. While he voted with the Committee at the most recent meeting, he dissented in favor of a cut at the one prior. More recently, he has emphasized data dependence and a willingness to hold rates if the data firm, while remaining opposed to hikes.

G10 Week Ahead

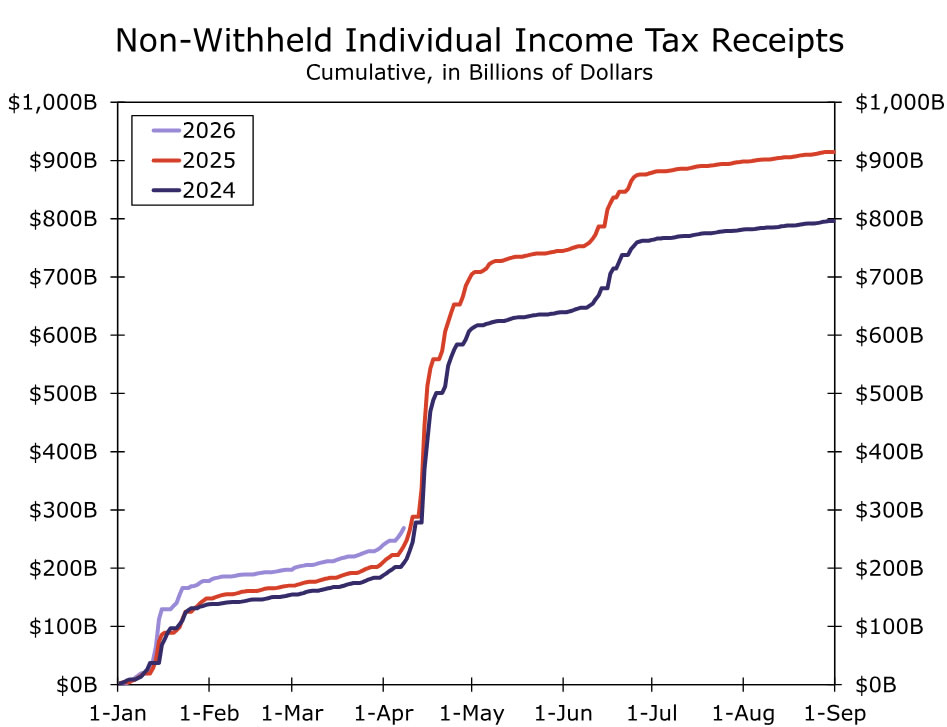

Australia Employment • Thursday

Next week’s Australian employment report for March should offer an early read on economic conditions in early 2026, as it is the first labor market release to partially overlap with the onset of the Middle East conflict. That said, it remains too soon for the data to materially affect the RBA’s Cash Rate outlook, given any momentum would largely predate the conflict. In February, the unemployment rate edged up to 4.3% from 4.1%, even as employment rose by 48.9K, driven entirely by gains in part-time jobs that more than offset declines in full-time employment. For March, consensus expects the unemployment rate to hold steady, with job gains slowing to 17.8K.

Absent a significant upside surprise, the RBA’s focus is likely to remain squarely on inflation and the anchoring of inflation expectations. Domestic price pressures are already facing additional upside risks from higher energy costs, which have begun to show up in domestic fuel prices. After reversing course on easing and delivering back-to-back rate hikes that have lifted the Cash Rate to 4.10%, we see the growth and labor market outlook as arguing for greater restraint. While markets have priced in three additional hikes this year, we expect policy to remain on hold, though risks remain skewed toward further tightening should inflation expectations continue to rise.

Source: Bloomberg Finance L.P. and Wells Fargo Economics

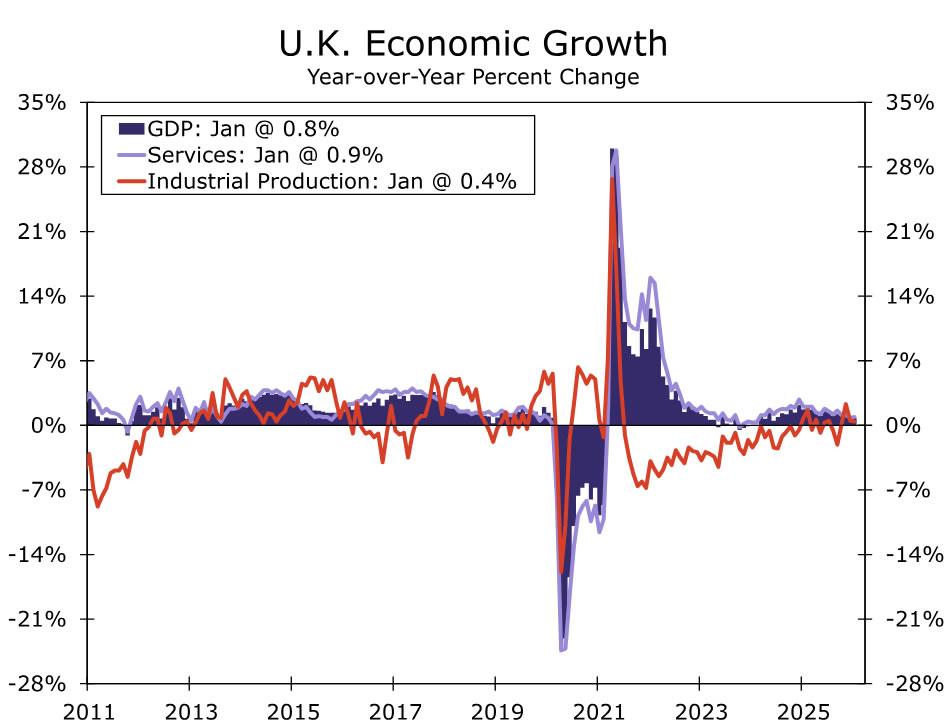

U.K. Monthly GDP • Thursday

We expect UK’s February GDP to rise 0.1% month-over-month, following a flat print in January. Despite the modest improvement, the outlook for Q1-2026 remains subdued after a weaker-than-expected January and a pullback in retail sales volumes in February. Growth is likely to be mixed across sectors, with some gains in industrial production and services largely offset by weakness in construction. February PMIs were broadly unchanged to slightly weaker compared with January, with the notable exception of construction, where activity declined more sharply. And even if growth were to surprise to the upside, the data predate the escalation of the conflict, which is likely to limit the weight policymakers place on the release.

With growth subdued, inflation starting from a lower trend, weak labor market and contained wage pressures, this backdrop strengthens the case for the Bank of England (BoE) to proceed cautiously and keep the Bank Rate on hold at 3.75%. This is especially true given that the policy rate is already near the top of the BoE’s estimated 2.75%–3.75% neutral range.

Source: Bloomberg Finance L.P. and Wells Fargo Economics

EM Week Ahead

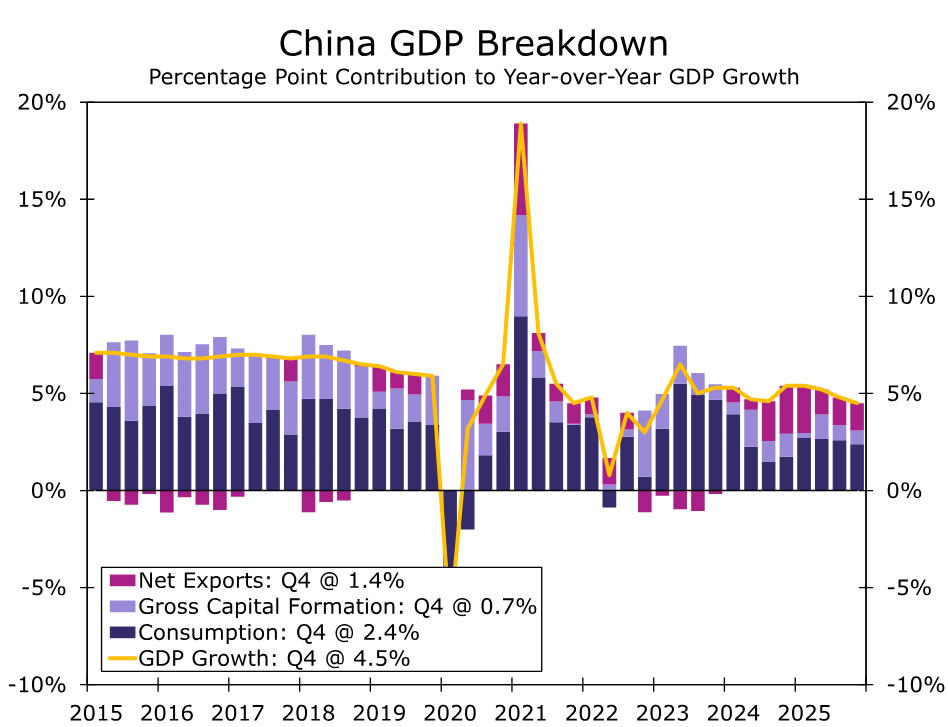

China GDP • Thursday

A slew of data will be released next week to gauge the health and direction of China’s economy. Q1 GDP as well as end of quarter activity data will all be closely monitored to see how Middle East tensions are impacting one of the largest oil-importing nations in the world. We forecast GDP growth that is slightly below consensus for Q1; however, March data may be parsed more closely as oil prices rose most sharply over the course of last month of the quarter.

But even if growth and activity surprise to the upside, repeating the 5% growth that was achieved last year will be challenging for China. As we have noted in the past, China has limited policy tools and less willingness to use policy support to spark activity due to negative tradeoffs. A real estate correction is still underway, which should be apparent when home price data are released, and tariffs and trade tensions with the U.S. also complicate China’s ambitions as world supplier. For now, we forecast China’s economy to grow 4.5% this year, and risks are tilted to the downside given the rise in energy prices. Perhaps Q1 gets off to a better start than we expect, but the later quarters may exhibit the bigger drag on overall growth.

and Waller (Fri.) strike us as the most noteworthy. We consider Williams as a good proxy for the more academically-minded members of the Fed. He doesn't usually shock markets, but his comments will be closely scrutinized for signals on a higher‑for‑longer stance versus the timing of any potential cuts. He has recently stressed that policy is “well positioned,” so any subtle shift in language in the wake of the Iran conflict could be meaningful. Waller, on the other hand, isn’t shy about changing his mind publicly. While he voted with the Committee at the most recent meeting, he dissented in favor of a cut at the one prior. More recently, he has emphasized data dependence and a willingness to hold rates if the data firm, while remaining opposed to hikes.){kind=link}