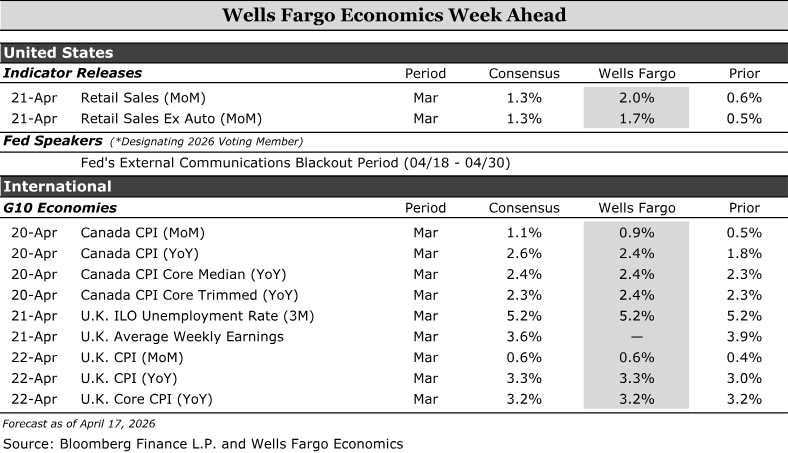

United States:

- Retail Sales (Tuesday), Kevin Warsh Confirmation Hearing (Tuesday)

G10 Economies:

- Canada CPI (Monday), U.K. Labor Market & CPI (Tuesday & Wednesday)

U.S. Week Ahead

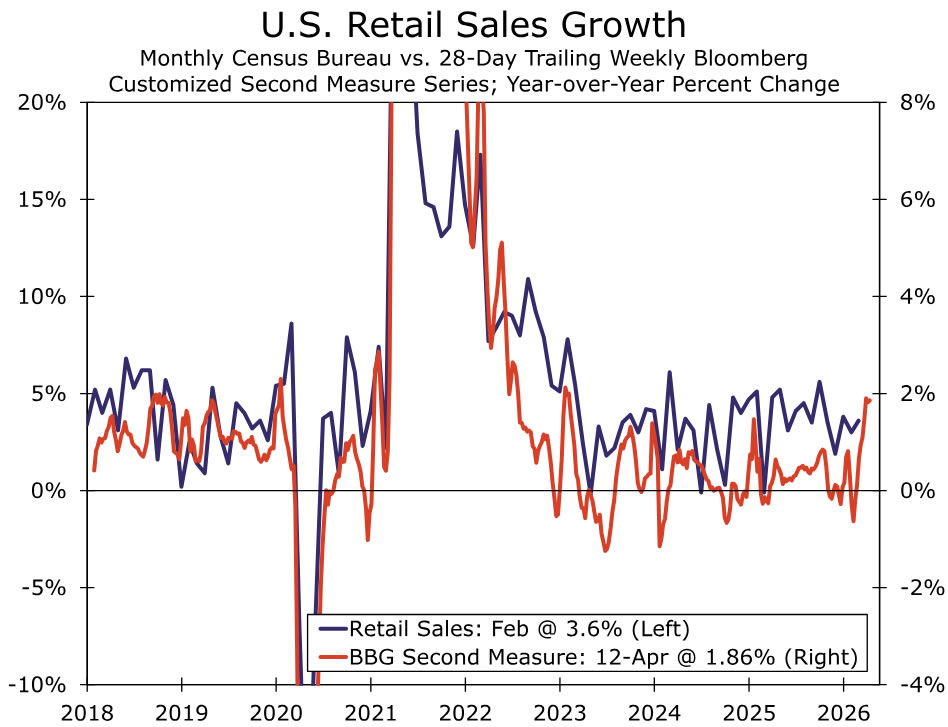

Retail Sales • Tuesday

Consumers have largely been unfazed by the initial move higher in prices at the pump. High-frequency credit card data from Bloomberg suggests households have continued to spend into early April (chart), and we forecast broader retail sales popped 2.0% in March.

That gain, however, partially reflects higher prices rather than increased sales volume given retail sales are reported nominally. Overall sales were likely still broad in March, but we expect an outsized gain will stem from gasoline sales specifically reflecting higher prices. Consumer goods prices jumped 2% in March from a month earlier. In stripping out the price effects, sales were weaker last month than the headline data will suggest.

We expect continued but slower spending in the wake of the ongoing conflict in Iran as higher tax refunds and after-tax incomes are largely offsetting the initial hit from higher gas prices. The longer this goes on, and the broader inflationary pressure becomes, the more concerned we grow on consumer resilience.

Kevin Warsh Confirmation Hearing • Tuesday

The Senate Banking Committee is scheduled to hold a confirmation hearing for Kevin Warsh on April 21. Warsh’s nomination to be the next Chair of the Federal Reserve has been in limbo since President Trump chose Kevin Warsh for the position on January 29. Completing his confirmation hearing is an important step toward eventually becoming Fed Chair, but a major hurdle still looms, with Senator Thom Tillis (R-NC) still promising to block Warsh’s nomination until the criminal probe by the Department of Justice into the Fed is lifted. Powell’s term as Chair ends in May, but if Warsh is not confirmed by then, Powell will continue to serve as Chair pro tempore until his replacement has been confirmed.

Warsh’s confirmation hearing will be a helpful update on his views on the monetary policy outlook and the Federal Reserve more generally. Warsh’s last public comments on monetary policy came way back in November in a Wall Street Journal opinion piece. We are particularly interested in Warsh’s near-term views on the appropriateness of the current level of the fed funds rate, the longer run neutral rate and Fed policy implementation questions, such as its communication tools and balance sheet.

We suspect Warsh will play it safe and try to be as vague as possible in most of his answers, a strategy designed to avoid alienating Senate support as well as members of the FOMC. But, he will not be able to duck all the questions, and given his lack of recent public comments and the wide range of views across the Committee at present, any tips or clues on core views will be extremely helpful for understanding the outlook.

G10 Week Ahead

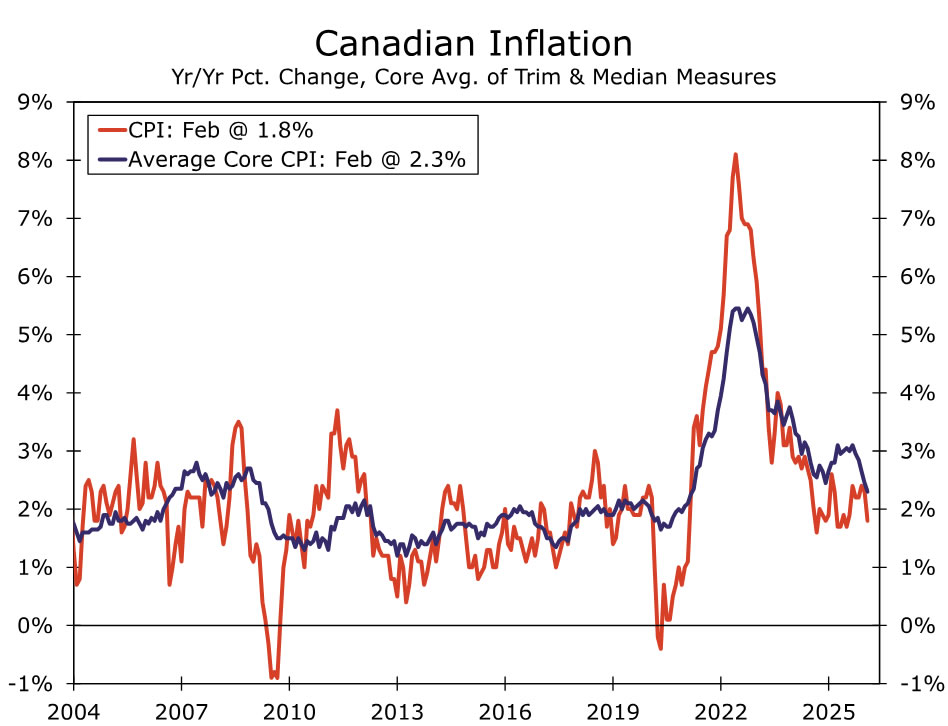

Canada CPI • Monday

We expect March headline CPI to print 0.9% month-over-month implying 2.4% year-over-year, which would be a significant acceleration from 1.8% in February. The February print was deceptively soft on account of the GST/HST holiday, and the March reading will be the last to carry those effects. At the same time, the energy supply shock as a result of the US-Iran conflict will add substantially to the March reading with additional carryover for April. In fact, our early estimate for April inflation is for the year-over-year print to be close or above 3%. On the core measures, we expect a slower move higher with both the year-over-year median and trimmed CPI at 2.4%. We continue to believe the overall effect of higher energy prices is a small positive for growth and more of an inflationary concern for the Bank of Canada (BoC). As such, the BoC’s calculus has likely shifted from a hold-cut decision to hold-hike in upcoming meetings. A +3% inflation reading is a breach of the upper bound of the BoC’s target range and implies negative real rates in Canada at least through end-2026 if current policy is maintained. An April 29 hold looks certain to us with the BoC likely to lean heavily on optionality given uncertainty in the Middle East and the USMCA renegotiation. With a clean reading on the effect of higher energy prices more likely starting in the April reading, June is the earliest possible timing for a BoC hike. We think that the BoC may opt to delay a hike decision till July, especially with the looming USMCA renegotiation deadline for July 1 and a broader presentation of its outlook in the July Monetary Policy Report.

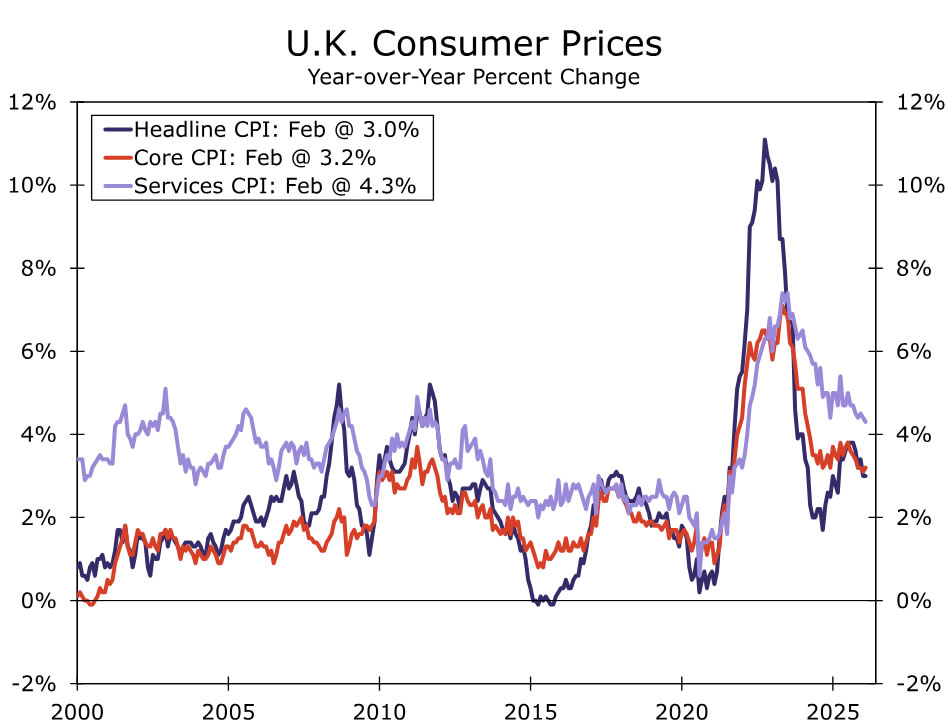

U.K. Labor Market & CPI • Tuesday & Wednesday

Next week will be busy for U.K. data releases, which market participants will closely scrutinize as they assess the economic impact of the conflict in the Middle East and its implications for Bank of England (BoE) policy.

The key release will be the March CPI report. We expect headline inflation to rise to 3.3% year-over-year from 3.0%, driven by the energy supply shock, while core inflation is expected to hold at 3.2%, matching February and in line with consensus expectations. This would mark a significant reversal in the progress toward disinflation seen in the U.K. through February and is likely to persist for several months.

CPI will not be the only release next week. We expect further moderation in wage growth over the three months through February, an unchanged unemployment rate at 5.2% in March and a subdued March retail sales reading, likely reflecting higher fuel prices. Taken together, these data should reinforce the case, in our view, for continued BoE caution and data dependence. While a higher headline inflation print may be viewed as a tightening signal, as long as wage pressures remain contained amid weak growth and elevated unemployment, we expect the BoE to remain on hold at 3.75% this year. Risks are skewed to the upside, particularly if underlying dynamics shift and second-round effects become more prominent.

still promising to block Warsh's nomination until the criminal probe by the Department of Justice into the Fed is lifted. Powell's term as Chair ends in May, but if Warsh is not confirmed by then, Powell will continue to serve as Chair pro tempore until his replacement has been confirmed.){kind=link}