No confirmation on US–Iran talks means no conviction in markets—for now. The focus shifts to Kevin Warsh’s testimony before the Senate Banking Committee at 14:00 GMT. With geopolitics offering no clear signal, investors are turning to Warsh’s testimony for guidance on the future direction of the Federal Reserve and the credibility of its policy framework.

Warsh’s prepared remarks have already been made public through advanced copies of his opening statement. He is focusing on three primary pillars to secure his confirmation:

Central Bank Independence: His most emphasized point is a vow to keep monetary policy “strictly independent.” He is expected to tell the committee, “The Fed must stay in its lane,” arguing that independence is at greatest risk when the central bank strays into fiscal or social policies.

Inflation Commitment: He has expressed a firm commitment to fighting inflation and achieving price stability, a move likely intended to calm markets concerned about potential political pressure for rapid rate cuts.

Response to Political Pressure: Addressing the friction between the White House and current Chair Jerome Powell, Warsh’s remarks suggest he views the Fed’s insulation from short-term political pressure as a “mechanical necessity” for a stable economy.

With Powell’s term ending on May 15, today’s testimony is the critical hurdle for Warsh to clear if the transition is to remain on schedule for mid-May.

In the currency markets, Kiwi is currently the strongest one for the week so far, boosted by today’s Q1 NZ inflation data. Swiss Franc is the second best, and then Loonie. Yen is sitting at the bottom, followed by Aussie, and then Dollar. Euro and Sterling are positioning in the middles.

In Europe, at the time of writing, FTSE is down -0.14%. DAX is up 0.39% CAC is down -0.23%. UK 10-year yield is up 0.026 at 4.862. Germany 10-year yield is down -0.005 at 2.980. Earlier in Asia, Nikkei rose 0.89%. Hong Kong HSI rose 0.48%. China Shanghai SSE rose 0.07%. Singapore Strait Times rose 0.22%. Japan 10-year JGB yield fell -0.012 to 2.386.

US Retail Sales Surge 1.7% mom in March, Core Spending Signals Resilient Demand

US retail sales rose 1.7% in March, beating expectations, with strong gains in ex-auto spending. Core sales growth also signed resilient consumer momentum. Read More.

ECB’s de Guindos Says ‘Keep a Cool Head’ as Energy Prices Drive Inflation Uncertainty

The ECB is not rushing to act. De Guindos urges a “cool head” as energy prices drive inflation—but the real question is whether it spreads across the economy. Read More.

German ZEW Sentiment Sinks to -17.2 as Iran War Hits More Than Just Energy Costs

Germany’s ZEW economic sentiment falls sharply as Iran war fuels fears of energy shortages and weak investment, highlighting deeper risks to economic growth. Read More.

NZD/JPY to Resume Up Trend to 96.50 as Inflation Boosts RBNZ Rate Hike Bets

NZD/JPY is breaking higher as inflation pressures remain firm. With non-tradable prices holding up, markets are strengthening bets on an RBNZ rate hike later this year. The cross now looks ready to resume the medium term up trend towards 96.50 target. Read More.

NZ Inflation Holds at 3.1% as Non-Tradables Stay Firm, Energy Pressures Build

New Zealand inflation isn’t easing as expected. With CPI holding at 3.1% and non-tradable prices still firm, the data points to persistent domestic pressure—keeping RBNZ rate hike expectations alive. Read More.

New Zealand Business Confidence Slumps as Conflict Weighs, Inflation Pressures Rise, RBNZ July Hike Expected

New Zealand business confidence has dropped sharply as geopolitical tensions weigh on outlook—but pricing pressures are rising. With firms still lifting prices, NZIER sees the RBNZ moving toward a July rate hike. Read More.

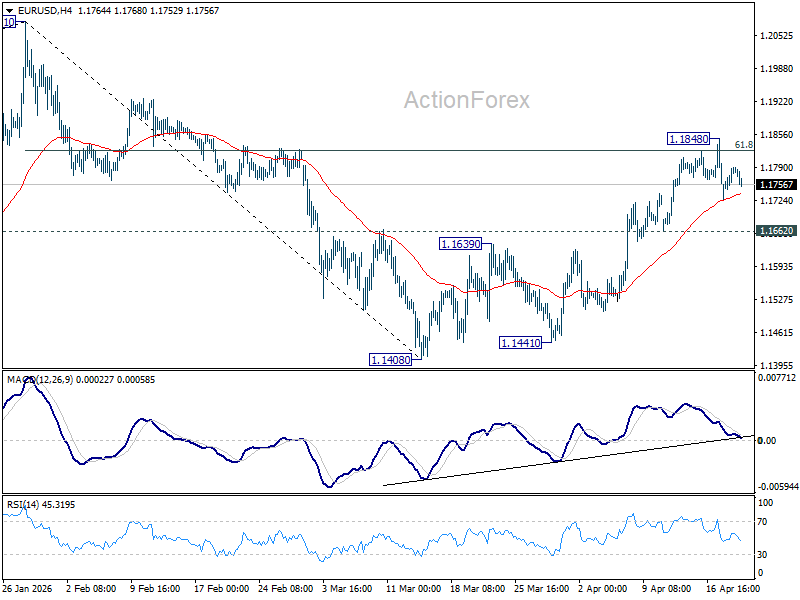

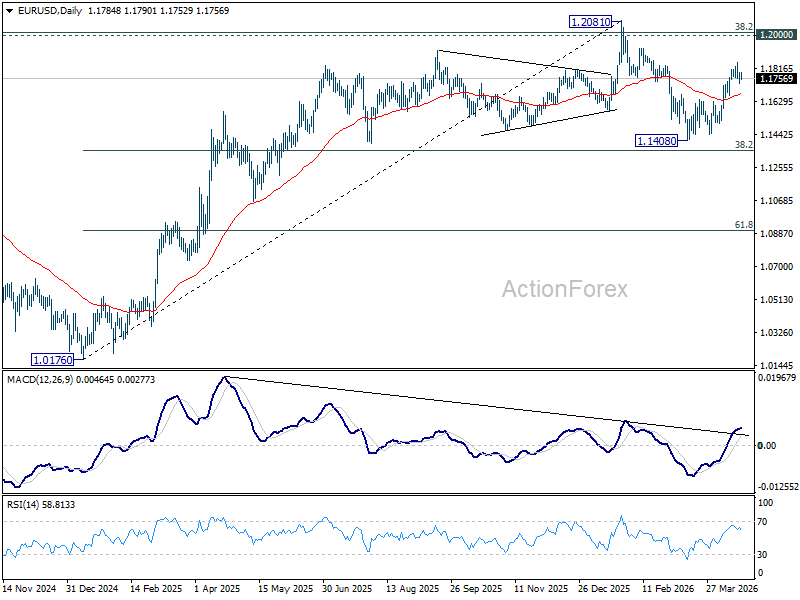

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1746; (P) 1.1768; (R1) 1.1809; More….

EUR/USD is still bounded in consolidations below 1.1848 and intraday bias remains neutral. With 1.1662 support intact, further rally is in favor. On the upside, sustained trading above 61.8% retracement of 1.2081 to 1.1408 at 1.1824 will pave the way to retest 1.2081 high. However, firm break of 1.1662 support will bring deeper decline back towards 1.1408 low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1507). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

{kind=link}