- Nonfarm payrolls enter spotlight after hawkish Fed.

- RBA prepares for its third straight interest rate hike.

- Canada employment report comes out alongside the NFP.

- Switzerland CPI and New Zealand jobs data also on tap.

Middle East tensions lift the Dollar and yields

The US dollar staged a recovery against its major peers this week, despite the ceasefire in the Middle East remaining in effect. The week began with a fresh wave of optimism as news hit the wires about Iran offering the US a proposal to end the conflict in the Middle East. However, the cheering was short-lived as, according to a US official, President Trump was unhappy with the proposition and remained willing to extend the blockade

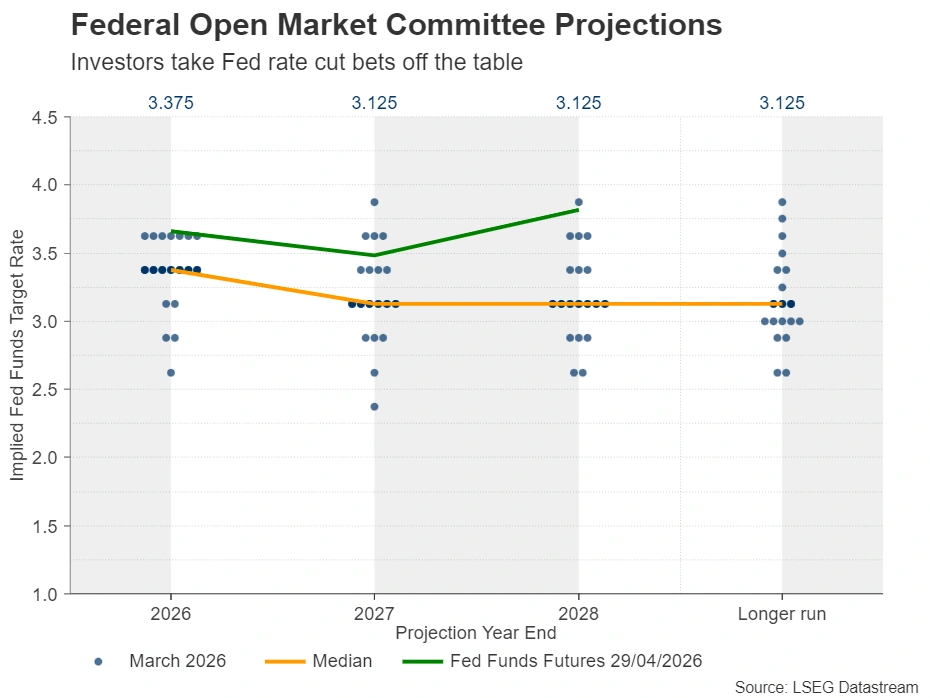

This pushed the US dollar and Treasury yields higher as anxiety about the Strait of Hormuz remaining closed for longer intensified. Fears that this could lead to even stickier inflation down the road prompted market participants to scale back their rate cut bets, with Wednesday’s Fed decision putting to bed any dim hopes about a potential reduction towards the end of the year.

The Fed decided to refrain from pressing the rate-cut button, citing still-too-high inflation. The decision was very divided, with one member voting for a rate cut at this gathering, but three others voting to remove or delay any signals of future rate cuts. This prompted investors to get their rate cut bets off the table and even pencil in a more-than-50% chance of a rate hike by April 2027.

Nonfarm payrolls to reshape Fed rate speculation

With the next meeting scheduled for June, and most probably the first under Kevin Warsh’s lead, investors could turn the spotlight on Friday’s NFP data as they try to gauge how the Fed may proceed from here onwards. The ADP report on the private employment sector will be released on Wednesday.

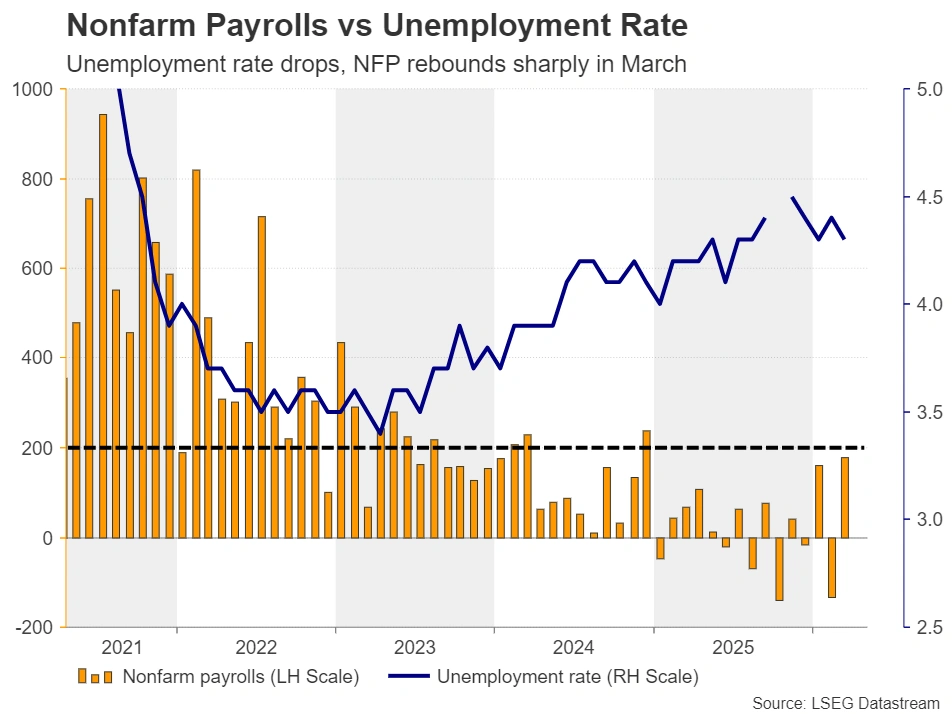

Nonfarm payrolls rebounded strongly in March, rising 178k after shrinking 92k in February, while the unemployment rate ticked down to 4.3% from 4.4% and average hourly earnings slowed to 3.5% y/y from 3.8%. Another month of solid job gains, accompanied by accelerating wage growth, which could intensify inflation concerns, could add further credence to the idea that the Fed does not need to further lower interest rates this year.

The 4-week moving average of the ADP weekly employment change has increased notably in April compared to previous months, corroborating the notion that, at least, the private sector has enjoyed strong jobs growth, tilting the risk to the ADP monthly print and, thereby, Friday’s NFP to the upside.

RBA set to hike again, will it maintain a hawkish stance?

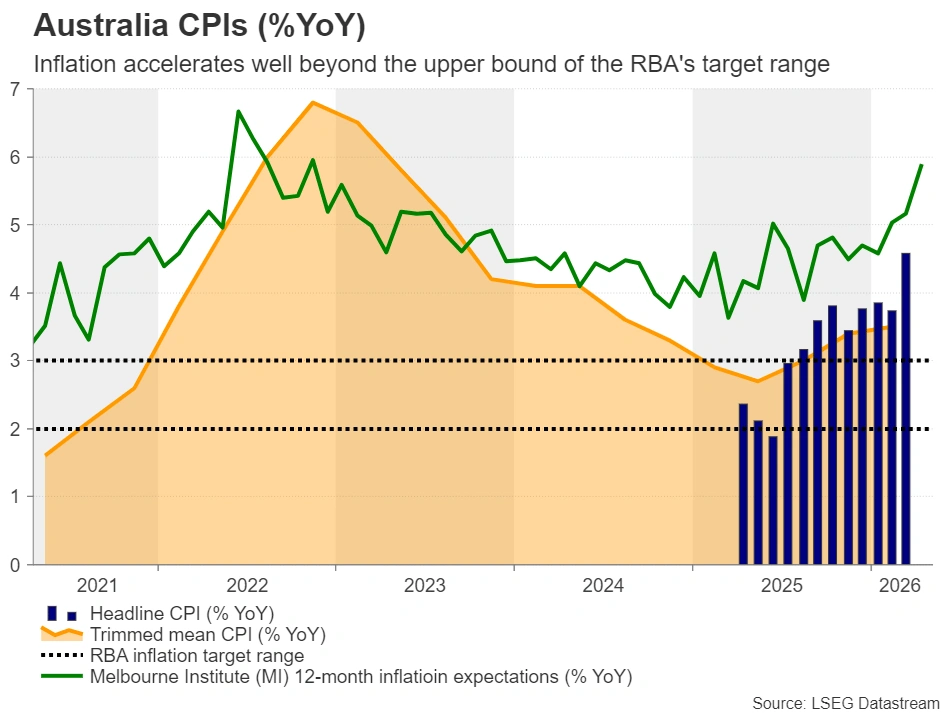

Following last week’s central bank barrage, on Tuesday, the torch will be passed to the Reserve Bank of Australia. At its latest gathering, on March 17, the Bank proceeded with its second consecutive quarter-point hike, citing elevated inflation and stronger-than-expected economic growth.

However, the decision was a close call, with 5 members voting in favor of a hike and 4 voting to hold. This makes next week’s decision even more interesting, despite market participants assigning a strong 75% chance that officials will pull the hiking trigger for a third straight time.

The reason for that may be the further acceleration in inflation, with all metrics moving further beyond the upper bound of the RBA’s 2-3% target range. In March, the headline CPI skyrocketed to 4.6% y/y from 3.7% in February, with the trimmed mean CPI remaining unchanged at 3.3%; and this with the job market remaining on a growth trajectory, adding 18k jobs in March and allowing the unemployment rate to rest at 4.3%.

A rate hike on its own is unlikely to shake the aussie much. Traders may need to see more members joining the hiking camp and receive stronger signals that the Bank remains willing to take interest rates higher if oil prices continue to pose a threat to inflation.

Canada and NZ jobs reports, Swiss CPI also in focus

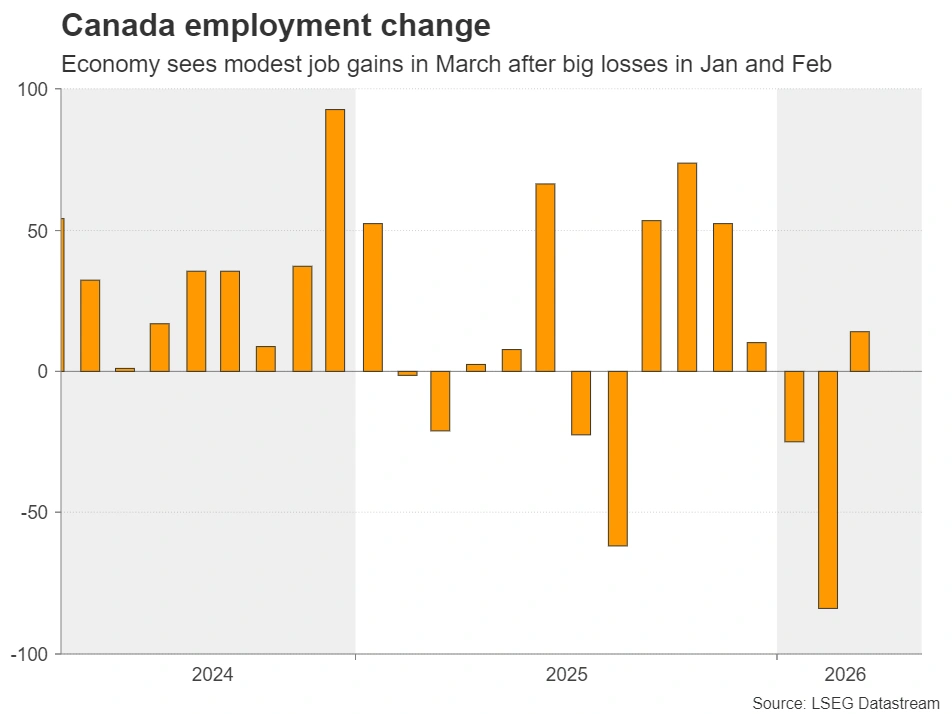

Flying to Canada, the nation’s employment report will be released at the same time as the US jobs data. The Bank of Canada also held its monetary policy decision on Wednesday. Officials decided to keep the policy rate untouched and although they acknowledged inflation is still above their objective, they regarded it as temporary pressure from oil prices. Therefore, even if the Canadian report comes in strong, a less hawkish message from the BoC compared to the Fed is unlikely to allow the loonie to outperform the US dollar.

Elsewhere, Switzerland’s CPI will be released on Tuesday, where a further uptick driven by the Middle East-related energy crisis could reduce pressure for the SNB to adopt negative rates and may also delay a potential intervention in the FX market. That said, despite the latest dollar gains, the franc remains extremely strong, and should it resume its prevailing uptrend, deflation concerns may resurface and the SNB could remain vigilant and willing to step into the FX market should it be deemed necessary.

New Zealand’s employment report is also on Tuesday’s agenda, but later in the day, during the early Asian session. Although the RBNZ signaled a “wait and see” stance at its April gathering, the stubbornly high oil prices have prompted investors to pencil in a 35% chance of a quarter-point hike at the May decision and a strong jobs report could take that percentage higher, thereby boosting the kiwi.

{kind=link}