- Discover our Weekly Market Outlook, exploring themes and events that forged financial flows throughout the week.

- Markets are subject to significant repricing after the confirmation of Kevin Warsh as the next Fed Chairman, and this theme should continue to price throughout the coming week.

- A few inflation releases, including Canada and UK CPI, will continue to provide clarity into the market situation.

- Get ready for next week’s action by exploring upcoming events across global markets.

Week in Review: Earnings Break Records, Pulling Markets Higher

Stock markets reached spectacular new highs just yesterday, heavily profiting from relentless artificial intelligence trends and a massive wave of record corporate earnings.

The S&P 500 aggressively breached the monumental 7,500 milestone, while the Dow Jones Industrial Average temporarily reclaimed the historic 50,000 mark as global risk appetite peaked.

Adding to this initial bullish momentum, the highly anticipated summit between President Trump and Chinese President Xi Jinping delivered a highly constructive geopolitical tone.

The two leaders established aligning views regarding the ongoing Middle East conflict and the general world order, with the two superpowers needing to collaborate.

Investors are now looking ahead to the next encounter between the two leaders, with an official invitation extended for President Xi to visit Trump in the United States in mid-September.

However, while these diplomatic developments generated better hopes for a sustainable peace process, financial markets are already rapidly turning the page on this theme.

Despite the midweek ecstasy, a much more dominant macroeconomic theme is now aggressively gripping the markets and causing widespread bloodshed ahead of the weekend.

Following the official Senate confirmation of Kevin Warsh as the next Federal Reserve Chairman, risk assets are subject to a brutal, significant repricing.

Ruthless bearish flows wiped out recent equity, metals and crypto gains as the US Dollar exploded higher at the direct expense of virtually all other asset classes.

Markets are hyper-focusing on the severe, long-term implications of a Warsh-led Federal Reserve. Institutional capital is actively preparing for a massive, systematic emptying of the central bank’s balance sheet, which remains one of the new Chair’s dearest ambitions.

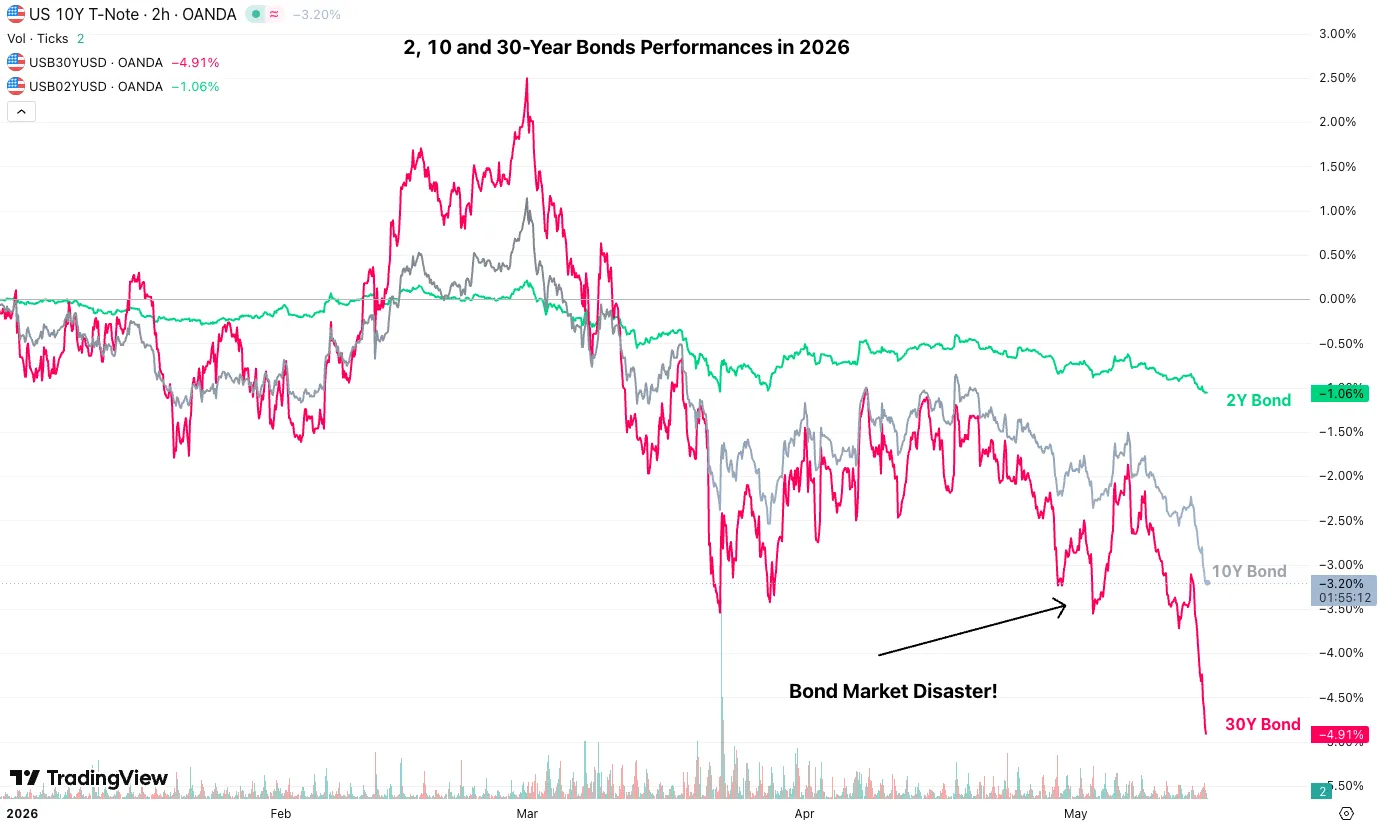

You can see this in the shocking action in bond markets, which threatens to trigger cascading effects into the broader market regime.

Broad US bond market since the beginning of 2026. Source: TradingView, May 15, 2026.

This aggressive trajectory possesses the terrifying potential to severely impact the foundational liquidity system that has supported global markets since the post-Great Financial Crisis era.

As this historic recalibration drains speculative excess from the financial system, this structural liquidity shift is the exact theme that continues to heavily dictate price action heading into next week and the coming months.

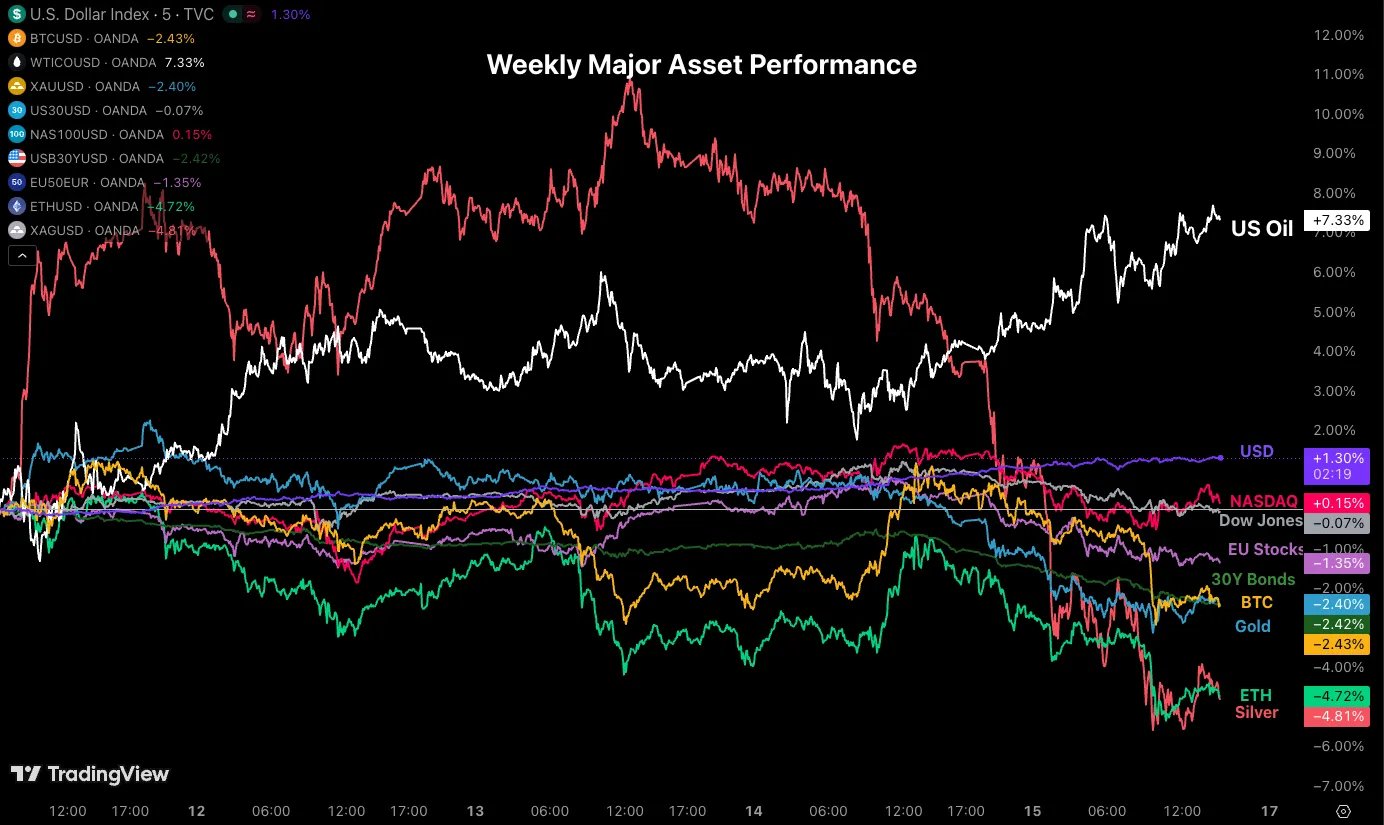

Weekly Performance Across Asset Classes

Weekly asset performance. Source: TradingView, May 15, 2026.

What could have been a dream-like week for major assets quickly turned into a dramatic rewinding, which took out more than what it gave.

When markets fear a drain in liquidity, it quickly brings back gigantic fears of a much more ruthless pre-GFC regime, where demand gets pushed and pulled by cyclical factors rather than the continuous support that it had seen in the past 17 years.

Stock markets, cryptos and metals, which had started the week on a rocketship, quickly turned back in the other direction, with most assets now down on the week.

The only exceptions remain WTI crude and the US Dollar.

The Week Ahead: G7 Meeting, UK and Canada CPI, and High-Tier PMI Reports

One of the key geopolitical events is the G7 meeting, which aims to provide more collaboration among members: Canada, France, Germany, Italy, Japan, the United Kingdom, and the United States.

In terms of broader markets, players will want to focus on the Kevin Warsh trade, bullish for the US Dollar and bearish on everything else.

Asia Pacific Markets: Australian Employment and Broad Economic Indicators

Next week’s APAC calendar brings heavy volatility across major economies.

China kicks off with high-impact Industrial Production forecast at 5.9% and Retail Sales at 2.0%, before the PBoC holds interest rates at 3.0%.

Japan faces critical Q1 GDP data, with expectations for a 1.7% annualized print, ahead of Thursday’s National CPI.

Australia navigates the RBA meeting minutes and Wednesday’s pivotal employment report, projecting a steady 4.3% unemployment rate.

Finally, New Zealand traders prepare for Thursday’s Q1 Retail Sales data.

Europe and UK Markets: UK Employment and Inflation, Along With Flurries of Economic Data

Get ready for a ton of action for the Old Continent.

In the UK, traders brace for Tuesday’s 4.9% unemployment rate and Wednesday’s critical CPI report, with headline inflation forecast at 3.3%. Thursday’s UK Services PMI is expected at 52.7.

In Europe, focus shifts to PMIs, projecting contraction in Germany at 48.4 and the broader Eurozone at 48.8.

Friday caps off the week with German Q1 GDP growth anticipated at 0.3%.

And do not forget a high number of ECB and BoE speakers throughout the week.

North American Markets: Canadian CPI, FOMC Minutes and US PMIs

Next week, North American markets face pivotal data as traders seek fresh direction. In Canada, Tuesday’s crucial CPI report takes center stage, with previous core YoY inflation sitting at 2.5%, followed by Friday’s retail sales forecast at 0.6%.

Meanwhile, US markets will hyper-focus on Wednesday’s critical FOMC minutes for monetary policy clues.

The US narrative then shifts to economic health on Thursday, highlighted by preliminary Manufacturing PMI, previously 54.5, and Services PMI, previously 51.0.

Keep a close eye on US markets and bonds, particularly after the end-of-week turmoil.

Next Week’s High-Tier Economic Events

Next week’s economic calendar. Source: TradingEconomics.

Safe trades and keep an eye on US-Iran developments, along with the Warsh trade.

{kind=link}