Risk aversion continue to be a main theme in the markets, ahead of quarter end. At the time of writing, major European indices are trading in red. DAX leads again by losing -1.27%, CAC down -0.76% and FTSE down -0.44%. DOW futures also point to more losses. Oil prices continue recent rally after making four year high. WTI crude is currently at 72.5 after marginally missing 73 handle. Spot gold is trying to defend 1250 but strengthen is non-existing so far.

In the currency markets, Canadian Dollar is trading broadly higher today, with help from oil price. The Loonie is followed by Euro as EUR/USD recovers ahead of 1.15 support. EUR/GBP also finally breaks out of month long range. New Zealand Dollar is trading as the weakest one for today after dovish RBNZ, followed by Sterling. For the week, though, Dollar remains the strongest one, followed by Yen. Nonetheless, at the other hand, Kiwi and the Pound are still the weakest.

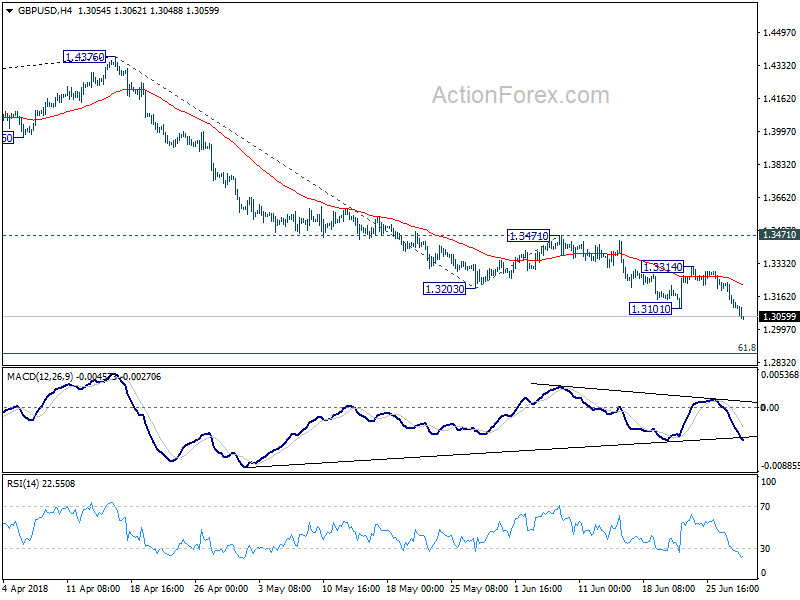

Technically, GBP/USD’s solid break of 1.3101 support confirm resumption of recent decline from 1.4375. It should now head to 1.2875 fibonacci level. EUR/GBP’s break of 0.8844 also indicate resumption of rise from 0.8620 and should target 0.8697 resistance next. While EUR/USD recovered ahead of 1.1507, there is no follow through buying. Focus will remain on this support, and break could trigger more broad based rally in the greenback. USD/CHF’s 0.9989 minor resistance will also be watched.

US initial jobless claims rose 9k to 227k. Q1 GDP revised down to 2.0%

US initial jobless claims rose 9k to 227k in the week ended June 23, above expectation of 220k. Four week moving of initial claims rose 1k to 221k. Continuing claims dropped -21k to 1.705m in the week ended June 16. Four week moving average of continuing claims dropped -3.75k to 1.7195. This is the lowest level since December 1973.

Q1 GDP growth was finalized at 2.0%, revised own from 2.2% and missed expectation of 2.2%. GDP price index was revised up to 2.2%, from 1.9%.

EU Malmstrom: To take provisional safeguard measures for steel industry starting mid-July

EU Trade Commissioner Cecilia Malmstrom said there could be provisional safeguard measures for the steel industry starting mid-July. The European Commission is still in process of investigation the measures needed after US steel and aluminum tariffs.

Malmstrom said “this is an investigation that will probably take until the end of the year before we can get the full picture.” But she emphasized that “we are seriously contemplating to have provisional measures in place, I would say mid-July could be some provisional measures. Exactly what form that will take is still under discussion.”

Separately, UK International Trade Minister Liam Fox said separately in the parliament that “we are looking to see what impact there may be from any diversion and whether we need to introduce safeguards to protect UK steel producers.” And,

“the earliest time that is likely to happen would be early to mid-July. We are already seeing some movements that I think may justify that.” He added that “as soon as we have the evidence to be able to justify such a decision, we would take it.”

ECB: Rise in protectionism could be significant risks to global activity

In its monthly bulletin, ECB noted that “euro area economic expansion remains solid and broad-based across countries and sectors, despite recent weaker than expected data and indicators.” In the June Eurosystem macroeconomic projections, annual real GDP growth is projected to be at 2.1% in 2018, 1.9% in 2019 and 1.7% in 2020.. HICP inflation is projected to be at 1.7% in 2018, 2019 and 2020.

On the global scale, ECB noted, that “following a year of strong and highly synchronised growth, global momentum slowed somewhat in the early part of 2018.” While, growth is expected to rebound in near term, it warned that “the implementation of higher trade tariffs, amid ongoing discussions of further protectionist measures, represents a risk to the global economic outlook.”

The US steel and aluminium tariffs so far “affect only a small proportion of global trade and are expected to have only a small global macroeconomic effect”. However, “the risks of further protectionist steps have risen”. Firstly, US “threatened to increase tariffs on USD 50 billion of Chinese goods, to which China pledged to retaliate. Secondly, “the United States launched an investigation into the national security implications of automobile imports.”

ECB added that “expectations of an escalation in the dispute could affect investment decisions, with potential effects on global growth”. And, “risks to global activity from a widespread rise in protectionism could be significant.”

Eurozone economic sentiment dropped sligthly by -0.2

Eurozone economic sentiment index (ESI) dropped a mere -0.2 to 112.3 in June, slightly above expectation of 112.1. Among the Eurozone countries, ESI rose 1.2 in Italy and 1.0 in France. however, there was a notable -1.8 decline in the Netherlands and -0.8 in Germany.

Eurozone industrial confidence was unchanged at 6.9, above expectation of 6.5. Services confidence was unchanged at 14.4, below expectation of 14.3. Consumer confidence was finalized at -0.5. The business climate indicator dropped -0.05 to 1.39, above expectation of 1.2.

ECB: Rise in protectionism could be significant risks to global activity

German Gfk consumer sentiment unchanged at 10.7. Economic expectations tumbled on protectionist Trump

German Gfk consumer climate for July (in June) was unchanged at 10.7, slightly above expectation of 10.6. Among the components, there is notable 14.1pts drop in economic expectations from 37.4 to 23.3. GFK blamed US trade policy as the driver of the decline. It said in the statement that “the American President’s protectionist trade policy, which affects both Germany and other export-oriented countries such as China, casts further gloom over the economic forecast.” As a result, “economic experts are currently predicting that the economic dynamics of the global economy will decline.”

As an export nation, Germany is affected “naturally”. Gfk pointed to the study of German Institute for Economic Research (DIW) and the ifo Institute, which projected the German economy will “drop down a gear” this year. These two institutes lowered GDP forecasts by around half a percent to 1.9% and 1.8% respectively.

Nonetheless, income expectations improved from 54.2 to 57.6. Propensity to buy also rose from 55.9 to 56.3. The improvements offset deterioration in economic expectations.

Also from Germany, CPI slowed to 2.1% yoy in June, down from 2.2% yoy and met expectation.

RBNZ More Dovish in June Meeting

RBNZ left the OCR unchanged at 1.75%. While the central bank reiterated its “neutral” monetary policy stance, the accompanying statement revealed that policymakers have turned slightly more dovish than previous months. The members were concerned about global trade tensions and the resulting financial market volatility. They also acknowledged more spare capacity at home as driven by the weaker than expected first quarter GDP growth. The members are ready to leave the policy rate at the current low level and get prepared to lower it, when necessary.

More in RBNZ More Dovish in June Meeting.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3066; (P) 1.3154; (R1) 1.3203; More…

GBP/USD drops to as low as 1.3048 so far today. Solid break of 1.3101 indicates resumption of larger decline from 1.4376. Intraday bias stays on the downside for 61.8% retracement of 1.1946 to 1.4376 at 1.2875 first. Break there will target 61.8% projection of 1.4376 to 1.3101 from 1.3471 at 1.2683 next. On the upside, break of 1.3314 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

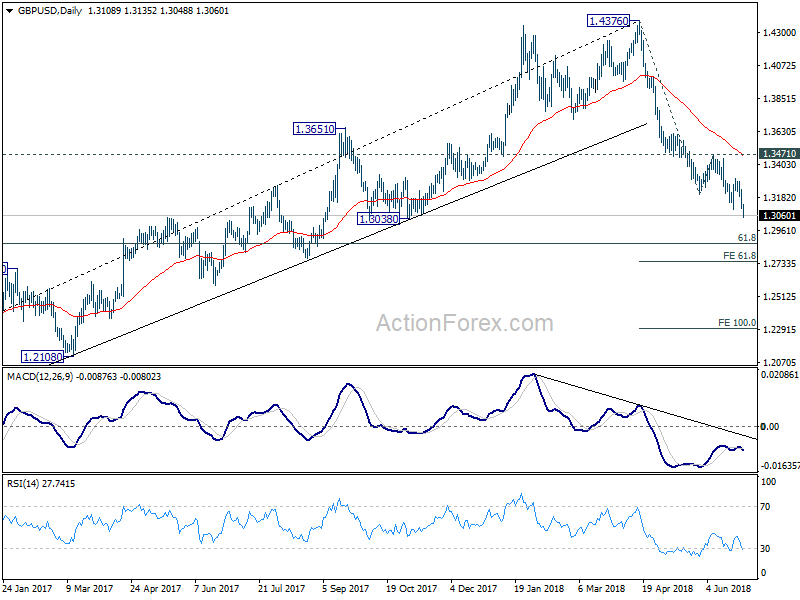

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4177). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We’ll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 1.3471 resistance holds, even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:00 | NZD | RBNZ Rate Decision | 1.75% | 1.75% | 1.75% | |

| 23:50 | JPY | Retail Trade Y/Y May | 0.60% | 1.20% | 1.60% | 1.50% |

| 06:00 | EUR | German GfK Consumer Confidence Jul | 10.7 | 10.6 | 10.7 | |

| 08:00 | EUR | ECB Monthly Economic Bulletin | ||||

| 09:00 | EUR | Eurozone Business Climate Indicator Jun | 1.39 | 1.2 | 1.45 | 1.44 |

| 09:00 | EUR | Eurozone Economic Confidence Jun | 112.3 | 112.1 | 112.5 | |

| 09:00 | EUR | Eurozone Industrial Confidence Jun | 6.9 | 6.5 | 6.8 | 6.9 |

| 09:00 | EUR | Eurozone Services Confidence Jun | 14.4 | 15.9 | 14.3 | 14.4 |

| 09:00 | EUR | Eurozone Consumer Confidence Jun F | -0.5 | -0.1 | -0.5 | -0.2 |

| 12:00 | EUR | German CPI M/M Jun P | 0.10% | 0.10% | 0.50% | |

| 12:00 | EUR | German CPI Y/Y Jun P | 2.10% | 2.10% | 2.20% | |

| 12:30 | USD | GDP Annualized Q/Q Q1 T | 2.00% | 2.20% | 2.20% | |

| 12:30 | USD | GDP Price Index Q1 T | 2.20% | 1.90% | 1.90% | |

| 12:30 | USD | Initial Jobless Claims (JUN 23) | 227K | 220K | 218K | |

| 14:30 | USD | Natural Gas Storage | 73B | 91B |

{kind=link}