Markets remain in full risk on mode this week. DJIA gained 232.23 pts or 1.12% to close at 20996.12 overnight. S&P 500 also rose 14.46 pts or 0.61% to close at 2388.61. Both indices took out structural resistance at 20887.5 and 2378.36 respectively and should be heading for new record highs. Meanwhile, NASDAQ maintains its lead and closed at new record high at 6025.49, up 0.7%. Treasury yields also jumped with 10 year yield closing up 0.054 at 2.327. That compares to last week’s low at 2.177 and structural resistance at 2.391. A break above 2.391 will pave the way for a test on 2.621 key near term resistance. Dollar stays weak against European majors though. But the dollar index is losing some downside momentum below 98.85 support.

Trump administration to deliver tax reform

Markets continue to re-price in June Fed hike. Fed fund futures now suggest over 75% chance of a 25bps hike by Fed at June meeting. And, it was below 50% last week. But the expectation would very much depends on what US President Donald Trump would deliver regarding his tax reforms today. There are talks that Trump would push to lower public companies’ income tax rate to 15%, down from 35%. Besides, there would be cut on top tax rate on "pass through" businesses, from 39.6% to 15%. And there would also be tax rate cut on offshore earnings which are repatriated, down from 35% to 10%. Meanwhile, there won’t be a so called "border-adjustment" tax on imports. Treasury Secretary Steven Mnuchin and National Economic Director Gary Cohn are scheduled to have a joint pressure conference around 1:30pm ET today, from the White House Briefing Room.

UK required to pay EU contributions until 2020

In UK, it’s reported that EU would require UK to pay the committed budget until 2020 before getting reasonable Brexit terms. On the other hand, UK Prime Minister Theresa May would only agree to it in exchange for a transitional deal that both sides would agree on. Meanwhile, May could offer an "ongoing payments" of some sort in exchange for a Free Trade Agreement after Brexit. European Commission President Jean-Claude Juncker and EU’s chief Brexit negotiator Michel Barnier will arrive in London today for a meeting with May. EU officials will discuss and approval their own negotiation plan in a summit on April 29.

BOJ Kuroda: G20 and IMF agreed to its monetary policies

Ahead of the two day BoJ monetary policy meeting, Governor Haruhiko Kuroda said yesterday that the G20 and IMF officials agreed with the central bank’s monetary policies. Kuroda told the parliament that "the IMF released a statement that re-affirms previous agreements that central banks should pursue their mandate to support economic activity and attain price stability." And he earned "the understanding that we are conducting policy to meet our inflation target."

Meanwhile, it’s expected that BoJ would lower inflation forecast in the quarterly Outlook for Economic Activity and Prices report, to be released on Thursday after the policy announcement. But the central bank may upgrade growth forecast. In January forecast, BoJ projected core CPI to hit 1.5% yoy in this fiscal year. But core CPI is currently standing at 0.2% yoy in February with weak momentum in price growth. On the other hand, IMF raised Japan’s growth forecast to 1.2% in 2017, up from January estimate of 0.8%. BoJ could share similar view.

Australian CPI back in RBA’s target range

Australia CPI rose 0.5% qoq and 2.1% yoy in Q1, up from prior quarter’s 0.5% qoq, 1.5% yoy. But missed expectation of 0.6% qoq, 2.2% yoy. That’s the first time inflation is back in RBA’s target range since 2014. RBA said earlier this month that it expected headline inflation to pick up over the course of 2017. However, it also expected that recovery in underlying inflation to be "a bit more gradual" due to subdued wage growth. Trimmed mean CPI rose to 1.9% yoy, up from 1.6% yoy and beat expectation of 1.8% yoy. Weighted median CPI rose to 1.7% yoy, up from 1.5% yoy, but missed expectation of 1.8% yoy.

Elsewhere…

Japan all industry activity index rose 0.7% mom in February. Swiss UBS consumption indicator will be released in European session. Canada will release retail sales later today.

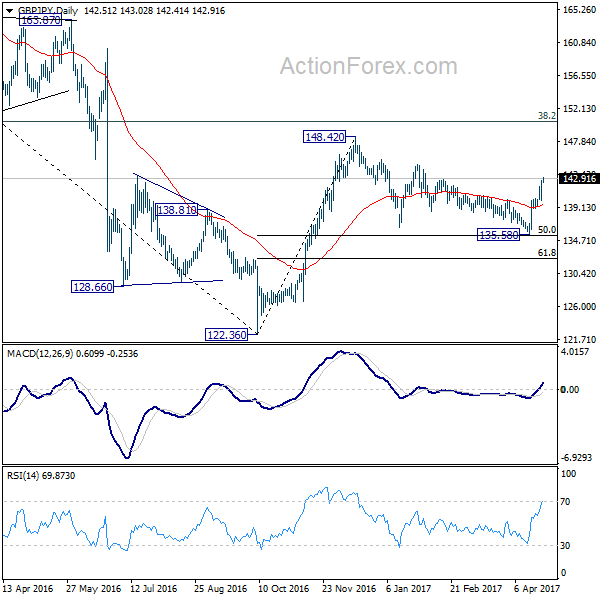

GBP/JPY Daily Outlook

Daily Pivots: (S1) 140.86; (P) 141.76; (R1) 143.47; More….

GBP/JPY’s rally continues and reaches as high as 143.20 so far. Intraday bias remains on the upside for 144.77 resistance. Consolidation pattern from 148.42 should have completed three waves down to 135.58, after hitting 135.39 fibonacci level. Break of 144.77 should extend whole rise from 122.36 through 148.42. On the downside, break of 140.04 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, price actions from 122.36 medium term bottom are still seen as a corrective pattern. As long as 50% retracement of 122.36 to 148.42 at 135.39 holds, another rising leg would be seen to 38.2% retracement of 195.86 to 122.36 at 150.42 and possibly above. However, firm break of 135.39 will bring retest of 122.36, with prospect of resuming the larger down trend from 195.86.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:30 | AUD | CPI Q/Q Q1 | 0.50% | 0.60% | 0.50% | |

| 1:30 | AUD | CPI Y/Y Q1 | 2.10% | 2.20% | 1.50% | |

| 1:30 | AUD | CPI RBA Trimmed Mean Q/Q Q1 | 0.50% | 0.50% | 0.40% | |

| 1:30 | AUD | CPI RBA Trimmed Mean Y/Y Q1 | 1.90% | 1.80% | 1.60% | |

| 1:30 | AUD | CPI RBA Weighted Median Q/Q Q1 | 0.40% | 0.50% | 0.40% | |

| 1:30 | AUD | CPI RBA Weighted Median Y/Y Q1 | 1.70% | 1.80% | 1.50% | |

| 4:30 | JPY | All Industry Activity Index M/M Feb | 0.70% | 0.60% | 0.10% | -0.40% |

| 6:00 | CHF | UBS Consumption Indicator Mar | 1.5 | |||

| 12:30 | CAD | Retail Sales M/M Feb | 0.20% | 2.20% | ||

| 12:30 | CAD | Retail Sales Less Autos M/M Feb | -0.30% | 1.70% | ||

| 14:30 | USD | Crude Oil Inventories | -1.0M |

{kind=link}