Dollar retreats broadly in early US session as this week’s rally lost some momentum. The greenback might need some help from tomorrow’s non-farm payrolls report if it’s to extend the rise. Still, Australian and New Zealand Dollar are the weakest ones on monetary policy divergence and risk aversion. Sterling is so far the strongest one for today on news that Brexit negotiation is making progress. Also, UK’s new Irish border solution is hailed as a step to the right direction. But so far there is no details on what progress was made. Yen follows as the second strongest, then Euro.

In other markets, DAX is the relative better performing one as it’s trading up 0.08% at the time of writing. FTSE is down -1.0% while CAC is down -1.12%. In Asia, Nikkei closed down -0.56%, Hong Kong HSI down -1.73%, Singapore Strait Times down -1.1%. China is still on holiday. Treasury yields catch a lot attentions globally today. German 10 year bund yield is up 0.043 at 0.519. UK 10 year gilt yield is up 0.0674 at 1.511. Japan 10 year JGB yield closed up 0.178 at 0.159. Eyes will be on whether US yield could extend yesterday’s strong rally.

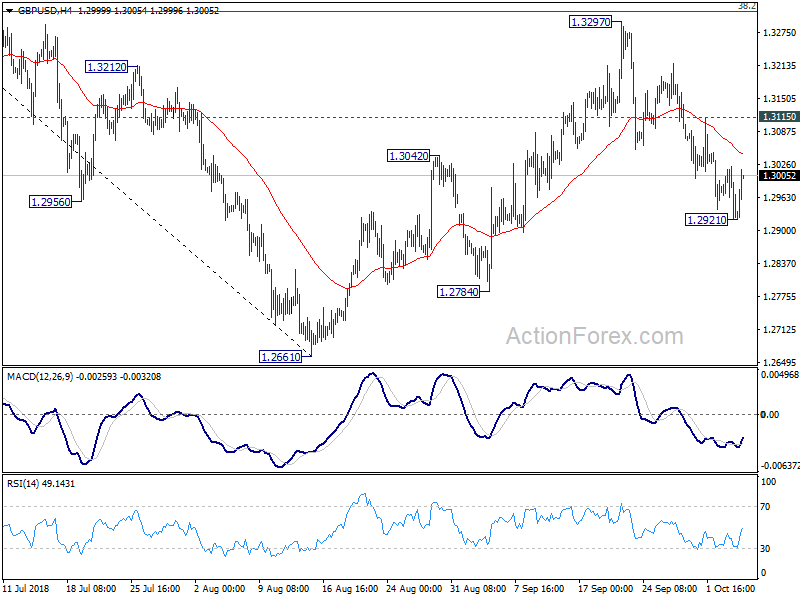

Technically, USD/JPY retreats quite deeply ahead of 114.73 resistance. With 113.51 minor support intact, further rise is still in favor. But break would indicate short term topping and bring lengthier consolidation. Sterling will also be a focus in US session. GBP/USD could have formed a temporary bottom already and stronger recovery might be seen to 1.3022 minor resistance and above. Meanwhile, EUR/GBP’s break of 0.8847 low invalidated our view and could be extending the fall from 0.9097.

US initial jobless claims dropped -8k to 207k

US initial jobless claims dropped -8k to 207k in the week ended September 29, slightly expectation of 206k. Four-week moving average of initial claims rose 0.5k to 207k. Continuing claims dropped -13k to 1.65m in the week ended September 22. Four-week moving average of continuing claims dropped -15.25k to 1.6645m, lowest since October 27, 1973.

ECB Rehn: Market expectations on first hike consistent with ECB statements

ECB Governing Council member Olli Rehn said “financial market expectations concerning the timing of the first interest rate rise are consistent with the Governing Council’s statements.” That is, ECB said in forward guidance that interest rates will remain at present levels at least through summer of 2019.

Meanwhile, he also added that “the need for extended forward guidance on monetary policy will also diminish, once inflation has reached sufficient progress towards the price stability objective.”

Regarding a hot recent topic of Italy, Rehn said ECB’s Governing Council “primarily looks at the development of the whole euro zone, and firstly from the mid-term price stability target point of view”. And, “monetary policy will be done based on that, not looking at just one member state but the whole euro zone.”

IMF: Japan needs reinvigorated policies for reflation, growth and sustainable debt path

IMF said in a report that while Japanese economy continues to “grow above potential”, downside risks have increased. It urged that “reinvigorated policies are needed to reflate the economy, boost potential growth, and put public debt on a sustainable path.” And, coordinated effort should include (i) a well-specified medium-term fiscal framework; (ii) an ambitious effort toward labor, product market, and corporate reforms; and (iii) a continued accommodative monetary policy accompanied by clear forward guidance.

On monetary policy, IMF hailed that “BoJ’s recent emphasis on making the accommodative stance more sustainable is appropriate, and complements its shift to a more patient approach to reaching the inflation target.” However, IMF suggested that “the relationship between the forward guidance on the long-term interest rate target and the inflation target could be clarified and the quantitative guidance on JGB purchases could be removed.” Also, it suggested BoJ to publish staff baseline forecasts together with underlying policy assumptions to strengthen market communications.

On trade, IMF emphasized that “Continued advancement of multilateralism and bolder domestic policies are needed to mitigate inward spillovers, including from potential trade-war escalation.” Though, Japan’s leadership in furthering multilateralism can help mitigate the possible effects of trade-war escalation.

World Bank downgrades East Asia and Pacific growth forecasts

The World Bank downgraded East Asia and Pacific growth forecast in 2018 from 6.6% to 6.3%. It also projected growth to further slow to 6.0% in 2019, down graded from 6.1%. For China, growth is projected to slow to 6.5% in 2018, unrevised. But China’s growth projection in 2019 was revised lower from 6.3% to 6.2%.

Sudhir Shetty, World Bank chief economist for East Asia and Pacific region, noted that “the main risks to continued robust growth include an escalation in protectionism, heightened financial market turbulence, and their interaction with domestic fiscal and financial vulnerabilities”.

And, he added, “in this context of rising risks, developing EAP economies need to utilize the full range of available macroeconomic, prudential, and structural policies to smooth external shocks and raise potential growth rates.”

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2897; (P) 1.2960; (R1) 1.3001; More…

GBP/USD’s recovery suggests that a temporary low is formed 1.2921 and intraday bias is turned neutral for consolidations. Upside of recovery should be limited by 1.3115 resistance to bring another decline. We’ll holding on to the view that corrective rise from 1.2661 has completed and larger decline from 1.4376 might be resuming. Below 1.2921 will target 1.2784 support next. Nonetheless, break of 1.3115 will dampen our view and turn focus back to 1.3297 resistance instead.

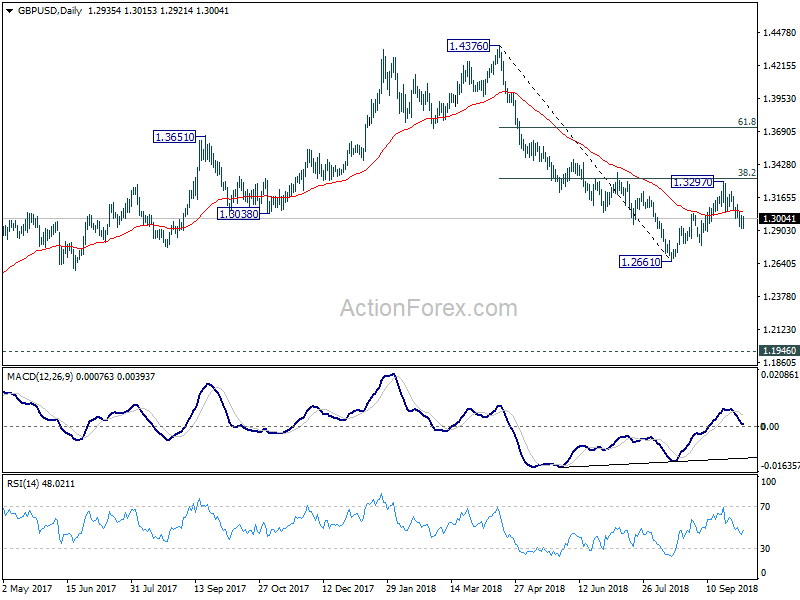

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA (now at 1.4062). The structure and momentum of the fall from 1.4376 argues that it’s resuming long term down trend. And this will be the preferred case as long as 38.2% retracement of 1.4376 to 1.2661 at 1.3316 holds. However, firm break of 1.3316 would bring stronger rebound to 61.8% retracement at 1.3721. And, the eventual depth of the fall from 1.4376, and the chance of hitting 1.1946 low, will depend on the strength of the interim corrective rebound from 1.2661.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Trade Balance Aug | 1.60B | 1.45B | 1.55B | |

| 11:30 | USD | Challenger Job Cuts Y/Y Sep | 70.90% | 13.70% | ||

| 12:30 | USD | Initial Jobless Claims (SEP 29) | 207K | 206K | 214K | 215K |

| 14:00 | CAD | Ivey PMI Sep | 61.4 | 61.9 | ||

| 14:00 | USD | Factory Orders Aug | 0.90% | -0.80% | ||

| 14:30 | USD | Natural Gas Storage | 47B | 46B |

{kind=link}