Sterling tries to recover some ground in Asia, after yesterday’s heavy selloff. But there is no sign of a turn a round in the Pound. The Brexit parliamentary vote is now called off and UK Prime Minister Theresa May is going back to the EU to seek changes on the deal, including the backstop. However, responses from EU are so far rather blunt. European Council President Donald Tusk insisted there is no renegotiation, including the backstop. We’ll see how the developments unfold, but Sterling will likely stay pressured for a while.

Staying in the currency markets, Canadian Dollar is the weakest one for today, followed by Dollar, and then Euro. Australian Dollar is the strongest, followed by Yen. Directions maybe a bit unclear from today’s picture. But overall, risk sentiments remain fragile despite the strong reversal in US stocks overnight. Yen and Swiss Franc, and to a lesser extent Dollar, could have a slight upper hand against Europeans and commodity currencies.

Technically, it’s clear that Sterling is bearish. EUR/GBP could have another take on 0.9098 resistance today. And any upside acceleration could pave the way to 0.9305 key resistance. GBP/JPY will also likely extend current fall to 139.88 support. EUR/CHF broke 1.1260 support yesterday to resume recent decline from 1.1501. It should be heading towards 1.1173 low. Rejection of EUR/GBP by 0.9098, and persistent weakness in EUR/CHF, could help push EUR/USD and EUR/JPY for downside range breakout.

In other markets, Nikkei is currently down -0.25%. Hong Kong HSI is up 0.02%, Shanghai SSE is up 0.18%, Singapore Strait Times is down -0.48%. 10 year JGB yield is up 0.0084 at 0.050. Asian Markets are pretty calm.

Overnight, DOW initially dropped to as low as 23881.47 but closed up 0.14% t0 24423.26. The daily range was as large as 619 pts. S&P 500 dropped to 2583.23 but closed up 0.18% at 2637.72. NASDAQ was indeed the star performer, dipping to 6878.98 but closed up 0.74% at 7020.52. Tech stocks are seen as saving markets with Apple gained 0.66%, Qualcomm gained 2.23%, Facebook gained 3.22%.

Treasury yield curve continued to flatten with 5-year yield up 0.13 to 2.709. 10-year yield closed up 0.006 at 2.856. 30-year yield dropped -0.014 to 3.129. Yield curve remains inverted between 3-year (2.738) and 5-year (2.709).

UK PM May called off Brexit vote, will seek change in backstop with EU

Yesterday, UK Prime Minister Theresa May formally confirmed in the Commons that the Brexit vote will be delayed. She said, if Tuesday’s vote went ahead, it would be lost by a wide margin. May said she’ll hold emergency talks with EU to discuss possible changes to the backstop. And, she pledged that changes to the backstop would ensure it’s not permanent.

On second Brexit referendum, May warned that “this risks dividing the country again when as a House we should be striving to bring it back together”. And she added that ” if you want to stay part of the customs union, be honest that this this involves accepting free movement.” Or, “if you want to leave with no deal, be honest that this will cause significant damage in those parts of the county that can least afford it.”

EU Tusk: No Brexit deal renegotiation, including the backstop

UK Prime Minister Theresa May called off Tuesday’s Brexit parliamentary vote as her deal would be defeated by a wide margin. Instead, May is going back to the EU for adjustments in the deal, in particular on Irish border backstop. Response from EU is so far rather cold.

European Council president Donald Tusk tweeted that they will discuss Brexit at the Dec 13/14 scheduled EU meeting. But he emphasized that “we will not renegotiate the deal, including the backstop”. Though, he said “we are ready to discuss how to facilitate UK ratifications:. Also, “as time is running out, we will also discuss our preparedness for a no-deal scenario.”

Suggested readings:

- Brexit Monitor: Brexit Clash Postponed To January, At The Earliest

- Brexit Update: EUR/GBP Surges As May Pulls Vote

Chinese VP Liu talked with Lighthizer and Mnuchin on timetable and roadmap of trade negotiations

The Chinese Ministry of Commerce said in a very brief statement about the phone call between Vice Premier Liu He, US Trade Representative Robert Lighthizer and Treasury Secretary Mnuchin earlier today.

It noted that “both sides exchanged views on putting into effect the consensus reached by the two countries’ leaders at their meeting, and pushing forward the timetable and roadmap for the next stage of economic and trade consultations work.”

The was no further elaboration on the details of the call. But the presence of Mnuchin is a gesture of willingness on both sides for constructive discussions. Mnuchin is seen by many as the most China-dovish member of Trump’s cabinet. And he should have likely taken a moderator role between Liu and Lighthizer.

US automakers called Japan currency manipulator, Japan FM Aso said your government hasn’t brought the topic up

Japan was fiercely attacked by an US automaker group in a US trade negotiating objectives hearing yesterday. The United Auto Workers representative criticized that the Japanese auto market is largely closed because of non-tariff barriers. Those barriers include Japan-specific regulatory, safety and emissions standards. Also, he said Japan manipulated its currency to push down the value of the Yen.

The UAW representative Desiree Hoffman went further and said “these barriers have created an uneven playing field, so much so that for every car that the U.S. exported to Japan in 2017, Japan sent 100 back”. And, “any loosening of the 2.5 percent automotive or 25 percent light truck tariff would further direct Japan’s overcapacity to our shores, exacerbating the problem.” Hoffman demanded Trump’s administration to impost strict import quotas on Japanese vehicles.

Japan Finance Minister Taro Aso responded calmly regarding currency manipulations. He said that “we have agreed with the U.S. side that any questions on currencies will be discussed with the U.S. Treasury Department, and so far it hasn’t been brought up.”

Released from Japan, BSI large manufacturing index dropped to 5.5 in Q4, M2 rose 2.3% yoy in November.

Australia NAB business confidence dropped to 3, house prices dropped -1.5% qoq

Australia NAB business confidence dropped to 3 in November, down from 5. Business conditions dropped to 11, down from 13.

Alan Oster, NAB Group Chief Economist noted that “the downtrend in conditions has continued in November” and, “this trend suggests that the business sector has lost some momentum since late 2017 and early 2018.” He added “confidence is now below average, suggesting that businesses themselves think momentum will slow further”.

On falling house prices, though, Oster noted “businesses do not yet suggest they are having a material impact.” And, “falling house prices in themselves may have a ‘wealth effect’ on households but given the prior large run up the impact of the declines to date is unclear”.

Also from Australia, house price index dropped for the third quarter by -1.5% qoq in Q3, matched expectation. Over the year, house priced dropped -1.9% yoy.

Among the capital cities, Sydney’s house prices dropped -1.9% qoq, -4.4% yoy. Melbourne’s dropped -2.6% qoq, -1.5% yoy. However, gains was recorded in Hobart (1.3% qoq, 13.0% yoy), Adelaide (0.6% qoq, 2.0% yoy) and Brisbane (0.6% qoq, 1.7% yoy).

Looking ahead

Now that there will be no Brexit parliamentary vote in UK today, focus will turn to job data. Germany will release ZEW economic sentiment. US will release PPI later today too.

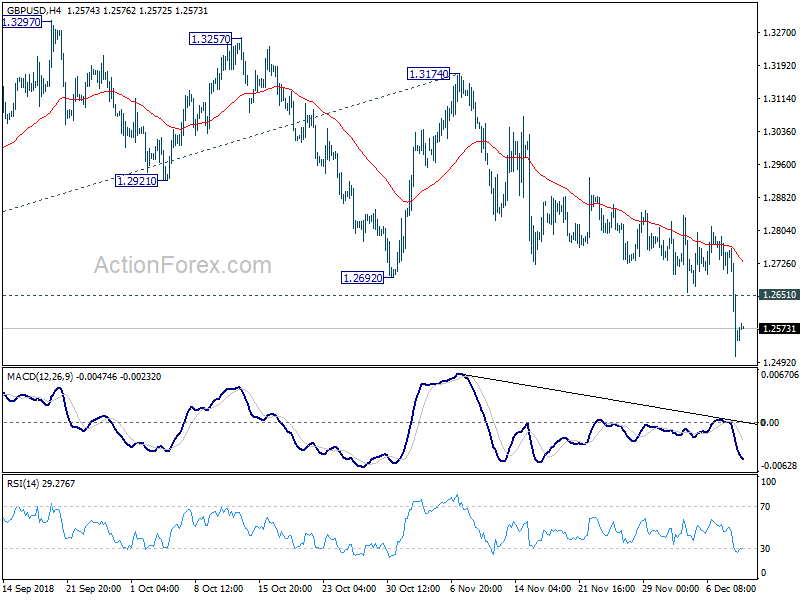

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2458; (P) 1.2609; (R1) 1.2710; More…

GBP/USD’s decline extended to as low as 1.2506 so far. Intraday bias stays on the downside for the moment. Prior break of 1.2661 support confirmed resumption of down trend from 1.4376. Further fall should be seen to 61.8% projection of 1.4376 to 1.2661 from 1.3174 at 1.2114. On the upside, above 1.2651 minor resistance will turn intraday bias neutral and bring consolidation first, before staging another decline.

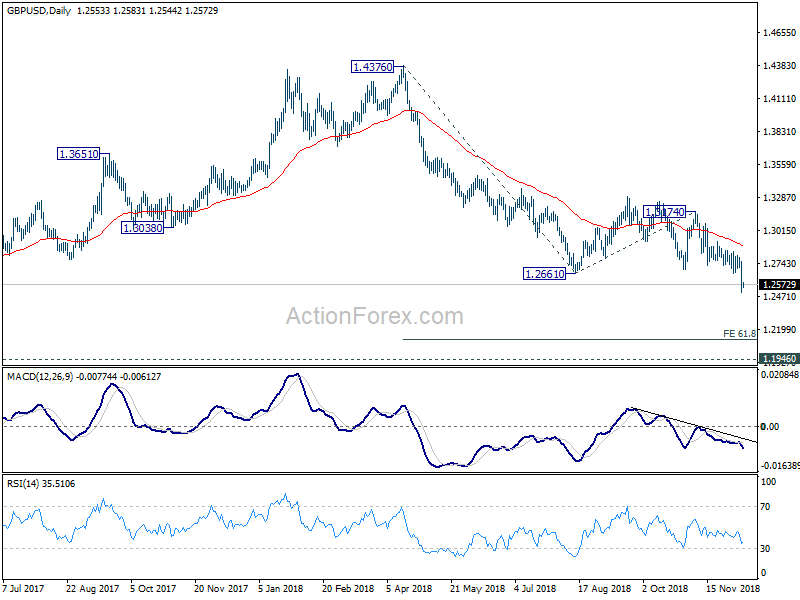

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA. The structure and momentum of the fall from 1.4376 argues that it’s resuming long term down trend from 2.1161 (2007 high). And this will now remain the preferred case as long as 1.3174 structural resistance holds. GBP/USD should now target a test on 1.1946 first. Decisive break there will confirm our bearish view.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Nov | 2.30% | 2.60% | 2.70% | |

| 23:50 | JPY | BSI Large Manufacturing Q/Q Q4 | 5.5 | 6.5 | ||

| 0:30 | AUD | NAB Business Confidence Nov | 3 | 4 | 5 | |

| 0:30 | AUD | NAB Business Conditions Nov | 11 | 12 | 13 | |

| 0:30 | AUD | House Price Index Q/Q Q3 | -1.50% | -1.50% | -0.70% | |

| 0:30 | AUD | House Price Index Y/Y Q3 | -1.90% | -0.60% | ||

| 6:00 | JPY | Machine Tool Orders Y/Y Nov P | -0.70% | |||

| 9:30 | GBP | Jobless Claims Change Nov | 13.2K | 20.2K | ||

| 9:30 | GBP | Claimant Count Rate Nov | 2.70% | |||

| 9:30 | GBP | Average Weekly Earnings 3M/Y Oct | 3.00% | 3.00% | ||

| 9:30 | GBP | Weekly Earnings ex Bonus 3M/Y Oct | 3.20% | 3.20% | ||

| 9:30 | GBP | ILO Unemployment Rate 3Mths Oct | 4.10% | 4.10% | ||

| 10:00 | EUR | German ZEW Economic Sentiment Dec | -25 | -24.1 | ||

| 10:00 | EUR | German ZEW Current Situation Dec | 55.6 | 58.2 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Dec | -23.2 | -22 | ||

| 13:30 | USD | PPIM/M Nov | 0.10% | 0.60% | ||

| 13:30 | USD | PPIY/Y Nov | 2.60% | 2.90% | ||

| 13:30 | USD | PPI Core M/M Nov | 0.20% | 0.50% | ||

| 13:30 | USD | PPI Core Y/Y Nov | 2.50% | 2.60% |

{kind=link}