The UK is in the center of focus again today. Now the time has come for a leadership challenge on UK Prime Minister Theresa May. Sterling gains a lot of round as it looks like May could survive this big test for her Brexit deal. The Pound is so far trading as the strongest one for today., followed by Euro, and then Canadian. On the other hand, New Zealand Dollar is the weakest one, walking its own path. Yen and Swiss Franc are also soft on improving risk sentiments. US and China are making progresses on trade war. Dollar also turns slightly weaker after consumer inflation data.

Technically, GBP/USD and GBP/JPY should have formed temporary bottoms and EUR/GBP formed temporary top. There is some upside potential in Sterling, for the nearest term. But then, there is no indication of bullish reversal yet, and it could come back under pressure quickly. While Dollar trades lower, EUR/USD, USD/CHF, AUD/USD and USD/CAD are trading familiar range. Some more is needed to indicate Dollar’s near term weakness.

In other markets, FTSE is currently up 1.29%, DAX up 1.29%, CAC up 2.07%. German 10 year yield is up 0.0327 at 0.268. Italian 10 year yield is down -0.121 at 2.996. German-Italian spread is now at 272, a very positive sign. Earlier in Asia, Nikkei closed up 2.15%, Hong Kong HSI up 1.61%, Shanghai SSE up 0.31% and Singapore Strait Times up 1.33%. 10 year JGB yield also closed up 0.0104 at 0.056.

No-confidence vote triggered, UK PM May pledged to fight with everything she got

Sterling receive strong support today, the same as May who is now facing no-confidence vote within hours. In particular BC editor Laura Kuenssberg tweeted that 158 Tory MPs have now said they will back May tonight. And that should be enough for her to win. Reuters also reported that at least 150 Conservative MPs have indicated support for May. 158 of 315 lawmakers are needed to secure May’s seat, theoretically. But the actual number will be slightly lower than that. And should May really wins, there’s a bigger chance for her to secure the needed tweaks, or “clarifications” from the EU, to come back and get the Brexit deal through the Commons.

Earlier today, Graham Brady, chair of the 1922 Committee, has received at least 48 letters from Conservative PMs for a confidence vote on May. The’s over 15% threshold for triggering the request. A ballot will now be held today between 1800 to 2000 GMT today. Brady didn’t put a firm number of the votes needed to oust May. Instead, he said he needed to see the full electoral lists to determine. Meanwhile, he expected to results to come out at around 2100GMT.

In a rather quick response, May pledged to contest the no-confidence vote with “everything I have got”. She believed the deal with EU is “attainable”. And she warned that a change of leadership in the Conservative now will “put the future of our country at risk and create uncertainty we can least afford it”. And she also warned that a change of leadership now would “hand the control of the Brexit negotiation to opposition MPs”. And the new leader will have to extend or rescind article 50, “delaying or even stopping ” Brexit.

Separately, European Council President Donald Tusk said in a letter to EU27 leaders that May would brief the other leaders before dinner on the EU summit on Thursday. And then, May would leave the leaders to “adopt Brexit conclusions. The EU27 leaders will discuss their preparations for no-deal Brexit.

US CPI slowed to 2.2%, Fed still on track for hike next week

Dollar dips mildly after US inflation data. Headline CPI slowed notably to 2.2% yoy in November, down from 2.2%. On the other hand, core CPI rose to 2.2%, up from 2.1% yoy. Both matched market expectations. Headline CPI peaked at 2.9% earlier in June while core CPI peaked at 2.4% in July. For now, Fed is still widely expected to raise interest rate again next week, and most likely another one in March. But diminishing upside pressure in inflation could start to tie Fed’s hand beyond March 2019.

In a Reuters interview, Trump toned down his rhetorics against Fed chair Jerome Powell and said he’s a “great guy”. Though, Trump still disagree to Fed’s “foolish” rate hike next week. Trump said, “Well, I think that would be foolish but what can I say? What can I say? You know, I put a man there. What can I say? If they do that, I’d be disappointed and I think a lot of people would be disappointed.” On Powell, Trump said, “I think he’s trying to do what he thinks is best. I disagree with him – I think he’s a great guy. But, I think he’s trying to get it right but I think he’s being too aggressive, far too aggressive, actually far too aggressive.”

On trade negotiation with China, Trump said the Chines are “back in the market” buying “tremendous amounts of soybeans”. He added there maybe another meeting of “top people on both sides”. And, if necessary, Trump is open to another meeting with Xi “who I like a lot and get along with very well”. Trump went further and said that he could intervene in the Huawei case if it’s good for the trade deal. He said “If I think it’s good for the country, if I think it’s good for what will be certainly the largest trade deal ever made – which is a very important thing – what’s good for national security – I would certainly intervene if I thought it was necessary.” Separately, Huawei’s top executive Meng Wanzhou, arrested by Canada on December 1 on US request, was granted bail by a Canadian court yesterday.

Australia Westpac consumer sentiment rose 0.1%, RBA to hold through 2020

Australia Westpac consumer sentiment rose 0.1% to 104.4 in December, up from 104.3. Westpac Chief Economist Bill Evans noted in the release that the disappointment of just 0.3% Q3 GDP growth is “likely to prompt the RBA to lower its growth forecasts for 2018 and 2019.” Also, “the atmospherics of a central bank forecasting strongly above trend growth is likely to change to one talking more about near trend growth.” And markets pricing have largely moved towards Westpac’s rate forecast. That is RBA will keep OCR unchanged at 1.50% “over the course of both 2019 and 2020”.

NAB becomes another bank to delay RBA rate hike expectations. It now expects the first hike to happen in second half of 2020. It noted that “ages pressure remains weak and hence inflationary pressure has remained low.” And, core inflation would continue to “track below RBA’s target band” through all of 2019. And, there would be a “moderation in growth back to potential of around 2.3 to 2.5%”. And, “falling house prices suggest a bigger impact on housing construction than previously incorporated and additional concerns about the consumer, though low rates and unemployment are important offsets.”

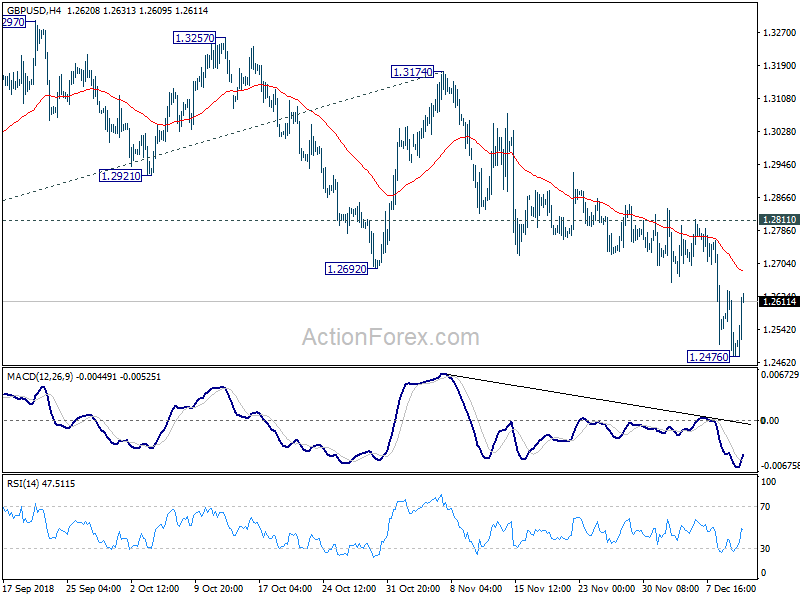

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2458; (P) 1.2609; (R1) 1.2710; More…

A temporary low should be in place at 1.2476 in GBP/USD with today’s recovery. Intraday bias is turned neutral for some consolidations first. But upside should be limited by 1.2811 resistance to bring fall resumption. On the downside, break of 1.2476 will extend larger down trend from 1.4376 to 61.8% projection of 1.4376 to 1.2661 from 1.3174 at 1.2114. However, firm break of 1.2811 will be an early signal of trend reversal and turn focus back to 1.3174 resistance.

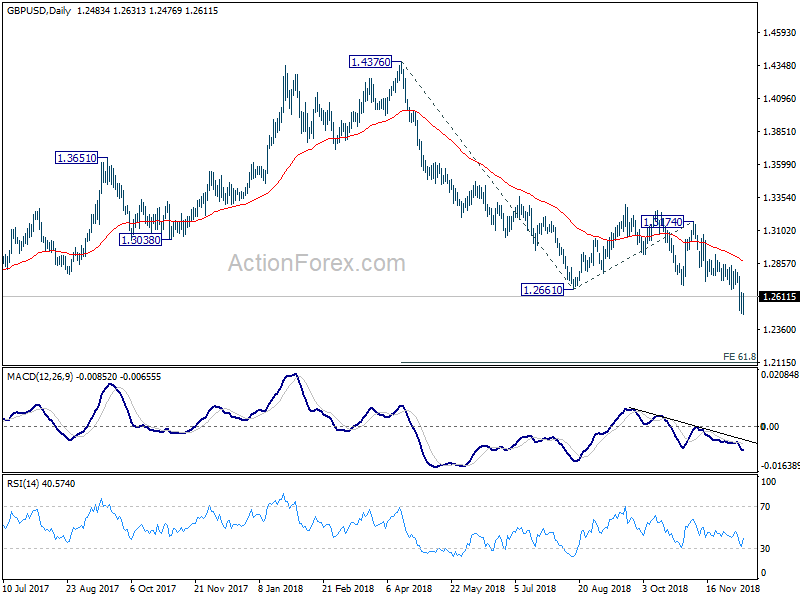

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA. The structure and momentum of the fall from 1.4376 argues that it’s resuming long term down trend from 2.1161 (2007 high). And this will now remain the preferred case as long as 1.3174 structural resistance holds. GBP/USD should now target a test on 1.1946 first. Decisive break there will confirm our bearish view.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Consumer Confidence Dec | 0.10% | 2.80% | ||

| 23:50 | JPY | Domestic CGPI Y/Y Nov | 2.30% | 2.40% | 2.90% | 3.00% |

| 23:50 | JPY | Machine Orders M/M Oct | 7.60% | 10.20% | -18.30% | |

| 04:30 | JPY | Tertiary Industry Index M/M Oct | 1.90% | 0.90% | -1.10% | -1.20% |

| 10:00 | EUR | Eurozone Industrial Production M/M Oct | 0.20% | 0.20% | -0.30% | |

| 13:30 | USD | CPI M/M Nov | 0.00% | 0.10% | 0.30% | |

| 13:30 | USD | CPI Y/Y Nov | 2.20% | 2.20% | 2.50% | |

| 13:30 | USD | CPI Core M/M Nov | 0.20% | 0.20% | 0.20% | |

| 13:30 | USD | CPI Core Y/Y Nov | 2.20% | 2.20% | 2.10% | |

| 15:30 | USD | Crude Oil Inventories | -3.0M | -7.3M | ||

| 19:00 | USD | Monthly Budget Statement Nov | -193.5b | -100.5B |

{kind=link}