Sterling is trading lower in Asian session today as UK Prime Minister Theresa May’s uninspiring statement did nothing to break the stalemate. But, commodity currencies are equally weak, if not weaker, following decline in the stock markets. There is no clear theme but investors appear to be turning cautious after yesterday’s set of Chinese data. Slowdown is inevitably lying ahead but the depth would very much depends on the trade negotiation with the US. For now, Yen and Dollar are the strongest ones so far.

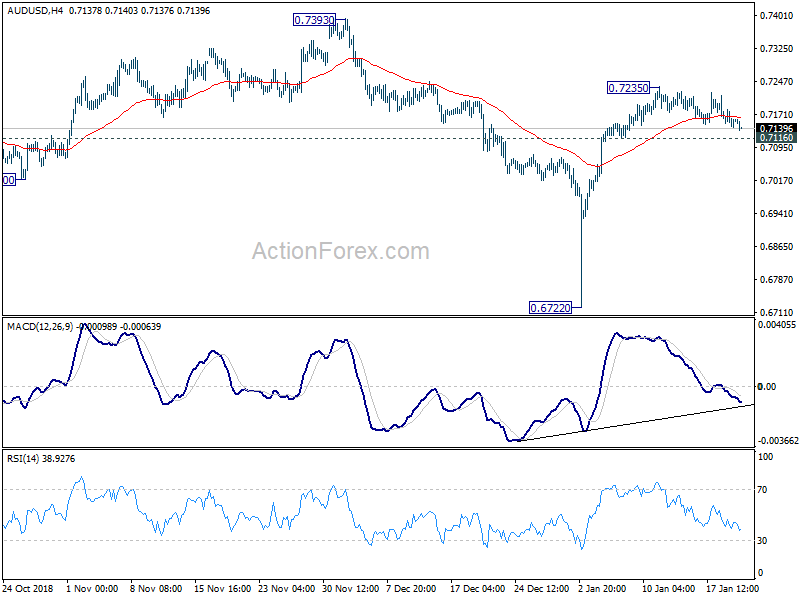

Technically, 1.3323 minor resistance in USD/CAD is a level to watch today. Break will add to the case of near term bottoming at 1.3180. And stronger rebound would be seen back towards 1.3664 high. 0.7116 in AUD/USD is another level to watch too. Break will suggest completion of rebound from 0.6722 and deeper fall would be seen back to this level.

In other markets, Nikkei is currently down -0.69% and is set to close with a loss. Hong Kong HSI is down -1.23%. China Shanghai SSE is down -1.17%. Singapore Strait Times is down -0.41%. Japan 10-year JGB yield is down -0.0037 at 0.001. WTI crude oil is currently at 53.5. It’s apparently losing momentum after hitting 54.44 yesterday, ahead of 54.61 resistance.

UK May pledged change in Brexit approaches, oppose to second referendum

UK Prime Minister Theresa May’s statement on Brexit plan B was rather uninspiring. In short, she finally acknowledged the need to have in change in her approach and laid out three areas. Those include, being “more flexible, open and inclusive” in engaging the parliament, embedding the “the strongest possible protections on workers’ rights and the environment”. And finally, ensuring the “commitment to no hard border in Northern Ireland and Ireland”. They’re hardly anything new.

Meanwhile, she continued to oppose to a second referendum as that would “damage social cohesion by undermining faith in our democracy.” And she doesn’t believe there is a majority for a second referendum. On Article 50 extension, she claimed that EU would not approve it unless UK had a plan for approving a deal. And the only way to avoid a no-deal Brexit would be to revoke Article 50.

May will continue cross-party talks and provide further update next Tuesday.

Businesses respond: Fundamentals have not changed and the stasis continues

In response to May’s statement on Brexit yesterday, CBI director general Carolyn Fairbairn said ” the government’s move to consult more widely is welcome, as is the commitment to scrap the settled status charge for EU citizens”. But she criticized that “the fundamentals have not changed” as “Parliament remains in deadlock while the slope to a cliff edge steepens.” She urged that “government should accept that no-deal in March 2019 must be off the table”.

Allie Renison, head of Europe and trade policy at the Institute of Directors also complained “the stasis continues”. She also noted that “two-thirds of our members say that leaving without a deal would be negative for their businesses and nearly 80% made clear they don’t want to see it happen.” And, “we desperately need politicians to get serious about finding a way forward.”

SNB Zurbruegg: Expansive monetary policy still warranted

SNB Vice Chairman Fritz Zurbruegg spoke at an economic forum in Landquart, Switzerland, yesterday. He noted that expansive monetary policy is still warranted for the central bank, due to heightened uncertainties, highly valued franc exchange rate, low inflationary pressure and global low interest rates.

In particular, he noted that uncertainties have risen recently, due to protectionism, Brexit, Italy. The Swiss Fran remains highly valued and that remains a risk. But overall, outlook for the Swiss economy remains favorable.

The comments echoed those by Chairman Thomas Jordan, who noted the need to block a surge Franc on safe-haven flow.

China NDRC: Downward pressure on economy will be passed onto jobs

China National Development and Reform Commission spokeswoman Meng Wei warned that the job market faces “new changes” ahead and slowdown in the economy will pressure the job markets. She also noted that some factories in the export hub of Guangdong province have shut earlier than usual ahead of Lunar new year holiday.

Meng said “from the viewpoint of ‘changes’, the external environment is complex and austere.” And, “Within the changes, there is something to worry about, and there is downward pressure on the economy. To a certain extent, the pressure will be passed onto jobs.”

Her comments came after survey-based data showed unemployment rate rose 0.1% to 4.9% in December, release yesterday.

On the data front

UK job data and German ZEW economic sentiment will be the major focus in European session. Later in the day, Canada will release wholesale sales and manufacturing sales. US will release existing home sales.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7139; (P) 0.7158; (R1) 0.7178; More…

AUD/USD weakens mildly today but it’s staying in range of 0.7116/7235. Intraday bias remains neutral first. As long as 0.7116 minor support holds, further rally is mildly in favor. On the upside, break of 0.7235 will target 0.7393 resistance. We’d expect strong resistance from there to limit upside. On the downside, break of 0.7116 minor support will suggest completion of rebound from 0.6722. Intraday bias will then be turned back to the downside for retesting this low.

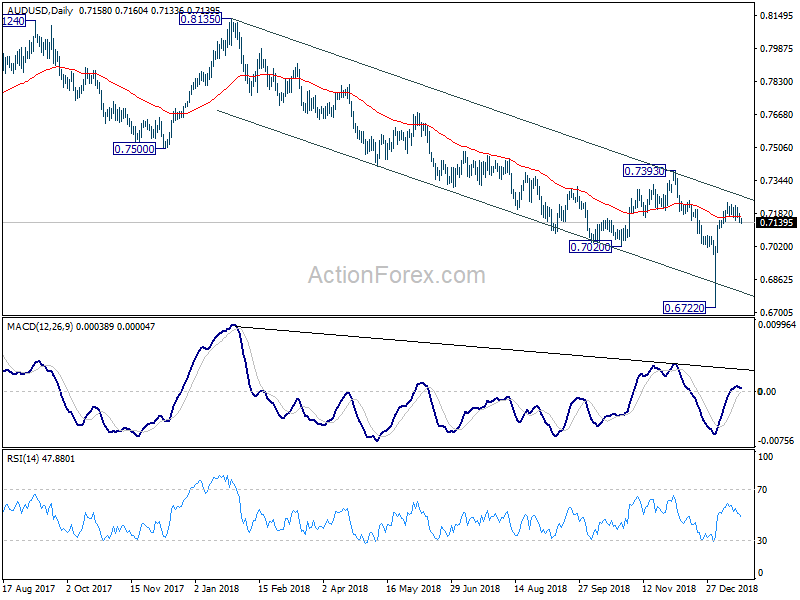

In the bigger picture, the failure to sustain below 0.6826 (2016 low) suggests that the long term down trend is not ready to resume yet. But prior rejection by 55 week EMA indicates underlying medium term bearishness in the pair. Outlook will also stay bearish as long as 0.7393 resistance holds. On the downside, sustained break of 0.6826 will target 0.6008 (2008 low).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 09:30 | GBP | Jobless Claims Change Dec | 20.1K | 21.9K | ||

| 09:30 | GBP | Claimant Count Rate Dec | 2.80% | |||

| 09:30 | GBP | Average Weekly Earnings 3M Y/Y Nov | 3.30% | 3.30% | ||

| 09:30 | GBP | Weekly Earnings ex Bonus 3M Y/Y Nov | 3.30% | 3.30% | ||

| 09:30 | GBP | ILO Unemployment Rate 3Mths Nov | 4.10% | 4.10% | ||

| 09:30 | GBP | Public Sector Net Borrowing (GBP) Dec | 1.1B | 6.3B | ||

| 10:00 | EUR | German ZEW Economic Sentiment Jan | -18.5 | -17.5 | ||

| 10:00 | EUR | German ZEW Current Situation Jan | 43.3 | 45.3 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Jan | -20.1 | -21 | ||

| 13:30 | CAD | Wholesale Trade Sales M/M Nov | 0.20% | 1.00% | ||

| 13:30 | CAD | Manufacturing Sales M/M Nov | -0.50% | -0.10% | ||

| 15:00 | USD | Existing Home Sales Dec | 5.27M | 5.32M |

{kind=link}