Swiss Franc is overwhelmingly the weakest one today with fresh selling in early US session. While Japanese Yen is also weak, it’s a relatively distant second. Both are pressured by extended rebound in global stocks. Meanwhile, additional pressure is seen on Franc from strong rebound in oil prices and emerging market currencies. Currently, both USD/TRY and USD/ZAR are down nearly -0.3%.

Return of risk appetite is benefiting Australian Dollar most. Investors are cheering the deal in US Congress to avert another government shut down, with funding for 90km of bordering fencing. Also, there seems to be some quiet optimism on US-China trade talks. Though, US Treasurer Steven Mnuchin and USTR Robert Lighthizer arrived in Beijing today for trade talks, without any notable comments so far.

Dollar and Euro are mixed for the moment. Sterling also stays mixed as UK Prime Minister delivered her Brexit update in the parliament. The most important thing to note is that if she cannot get an approvable new deal by February 26, the Commons will be given a chance to vote on a plan B on the following day.

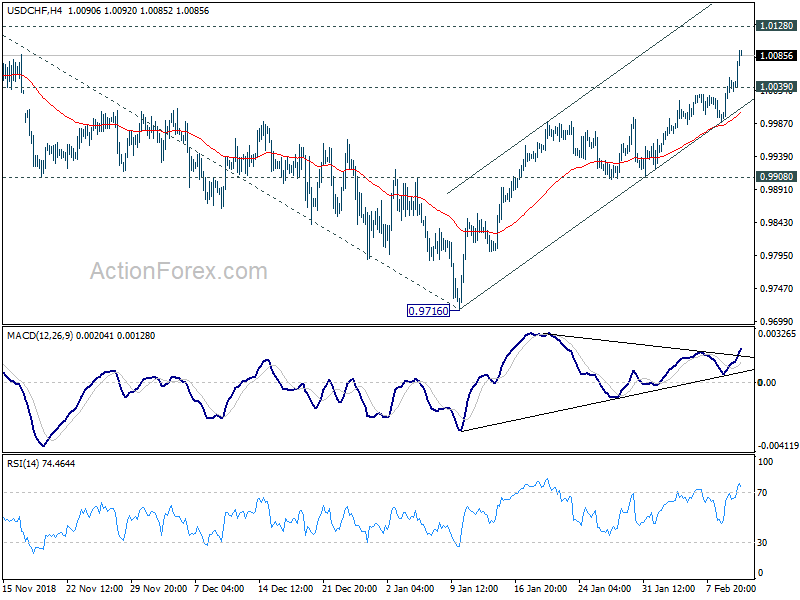

Technically, USD/CHF’s rally is accelerating towards 1.0128 key resistance. Break will confirm medium term up trend resumption. EUR/CHF’s break of 1.1376 minor resistance also suggests that pull back from 1.1444 has completed. Further rise is now likely through this level to 1.1501 key resistance. While AUD/USD is strong, upside is so far still capped by dovish RBA expectation. Further decline will remain in favor for the near term as long as 0.7107 minor resistance holds.

In Europe, currently, FTSE is down -0.07%. DAX is up 1.03%. CAC is up 0.86%. German 10-year yield is up 0.0204 at 0.143. Earlier in Asia, Nikkei rose 2.61%. Hong Kong HSI rose 0.10%. China Shanghai SSE rose 0.68%. Singapore Strait Times dropped -0.16%. Japan 10-year JGB yield rose 0.0184 to -0.009, staying negative.

US Treasurer Mnuchin and USTR Lighthizer arrive in Beijing for trade talks

US Treasury Secretary Steven Mnuchin and Trade Representative Robert Lighthizer arrived in Beijing today, ahead of the high-level meeting on Thursday. Mnuchin told reporters that “it’s great to be here back in Beijing,” and “we’re looking forward to several important days of talks.” Lighthizer arrived earlier but didn’t any any questions from reporters.

UK PM May: Parliament can vote on Brexit plan B is no new deal is agreed by Feb 26

UK Prime Minister Theresa May said in the parliament that she told European Commission President Jean-Claude Juncker last week that UK wanted “legal binding” changes to the withdrawal agreement that it would not be kept in the backstop. But Juncker insisted EU would not reopen negotiation on the withdrawal agreement.

May told lawmakers such request for renegotiation was “reasonable”. But she also admitted that “some time” is needed to complete the process of negotiating a better deal on Irish backstop. Though, May is still aiming to leave the EU on March 29. She also promised that if she cannot get a deal by February 26, the Commons will have a chance to vote on a plan B the following day.

For this week, it’s confirmed that there will be no meaningful vote in the Commons, but amendable motion for debate on Thursday.

BoE Carney: Brexit is the first test of a new global order

BoE Governor Mark Carney noted in a speech “The global outlook” today that global growth momentum is now “weakening in all major regions” and “downside risks have intensified”. Also, the proportion of the global economy growing above trend has fallen from four-fifths to one-third.

Tighter financial conditions could be part of the reasons for the deceleration. But he warned, “potentially more seriously, the slowing in global momentum may also be the product of rising trade tensions and growing policy uncertainty.” And, “risks from China and from de-globalisation are significant and growing.” Carney also emphasized “contrary to what you might have heard, it isn’t easy to win a trade war.”

He added that Brexit is the “first test of a new global order”. It could be the “acid test” of “whether a way can be found to broaden the benefits of openness while enhancing democratic accountability.” And, Brexit can also lead to “new form of international cooperation and cross-border commerce built on a better balance of local and supranational authorities.”

Bundesbank Weidmann: Acting beyond mandate will undermine trust in ECB

Bundesbank President Jens Weidmann warned today that the Eurozone is still not crisis proof. He pointed out that “certain issues like the lack of credibility of fiscal rules or the harmful sovereign-bank nexus still have to be adequately addressed.”

At the same time, fighting crises could force unelected ECB bankers to take political positions that’s beyond its own mandate. And, “acting beyond the mandate would also undermine people’s trust in the central bank.”

He added, “at the end of the day, it could become more and more difficult for the European Central Bank to focus on its promise of a stable currency.”

ECB Knot: Wait-and-see attitude is probably the optimal attitude

ECB Governing Council member Klaas Knot said there is no need to raise interest rates before more sign of inflation pickup to target. He said “we will have to be patient and also, in my view, modest with respect to the precise moment at which we can expect inflation to converge toward our medium-term objective.” And, at this moment, a “wait-and-see attitude is probably the optimal attitude.”

Knot also tried to play down recession risk despite economic slow down. He said “the current situation might last a few quarters, but I’m still positive . . . that afterwards growth will return to levels slightly above potential again.”

NAB on RBA: Next rate move could be down rather than up

Australia NAB Business Condition staged a moderate rebound in January up from 2 to 7 and beat expectation of 4. That came after the sharp decline from 11 to 3 in December. Business Confidence also rose slightly from 3 to 4. NAB noted that even after the recovery, “conditions and forward orders continue to trend lower and still show a sizeable decline over the past 6 months.”

Alan Oster, NAB Group Chief Economist noted that “Based on the confirmation that conditions have deteriorated further and our current set of forecasts we now see the RBA staying in neutral for the foreseeable future, though think the next move could be down rather than up based on the current trajectory of growth and growing downside risks”.

Also from Australia, home loans dropped -6.1% mom in December versus expectation of -2.0% mom.

RBNZ survey: Inflation, house price and GDP expectations dropped

RBNZ quarterly survey showed inflation expectation for a year ahead dropped from 2.09% to 1.82%. One-year house price expectations dropped sharply from 2.86% to 1.91%. One-year rolling annual GDP expectation dropped slightly from 2.44% to 2.38%. Regarding RBNZ monetary policy, a net 75.6% of respondents believe monetary conditions in one year’s time will be easier than neutral.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.0000; (P) 1.0027; (R1) 1.0068; More….

USD/CHF’s rally accelerates to as high as 1.0092 so far today. Intraday bias stays on the upside for 1.0128 resistance. Decisive break there will confirm resumption of up trend from 0.9186. Next target will be 100% projection of 0.9541 to 1.0128 from 0.9716 at 1.0303. On the downside, below 1.0039 minor support will turn intraday bias neutral first and bring consolidations. But retreat should be contained well above 0.9908 support to bring another rally.

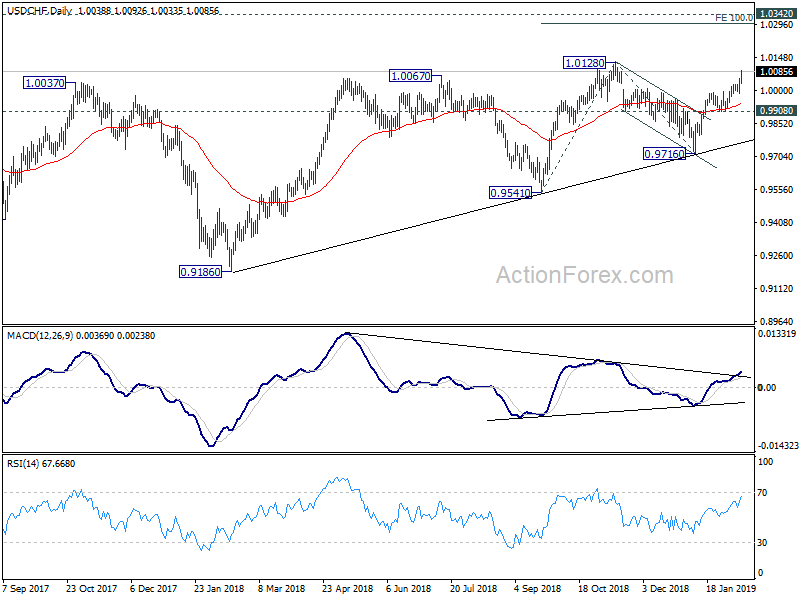

In the bigger picture, USD/CHF drew strong support from medium term trend line and rebounded. That suggests rise from 0.9186 is still in progress. Further break of 1.0128 will confirm up trend resumption and target 1.0342 key resistance. Nevertheless, break of 0.9716 will dampen this bullish view and at least bring deeper fall to 0.9541 key support.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Jan | 2.40% | 2.40% | 2.40% | |

| 0:30 | AUD | Home Loans M/M Dec | -6.10% | -2.00% | -0.90% | |

| 0:30 | AUD | NAB Business Confidence Jan | 4 | 3 | 3 | |

| 0:30 | AUD | NAB Business Conditions Jan | 7 | 4 | 2 | |

| 4:30 | JPY | Tertiary Industry Index M/M Dec | -0.30% | -0.10% | -0.30% | |

| 6:00 | JPY | Machine Tool Orders Y/Y Jan P | -18.80% | -18.30% | ||

| 11:00 | USD | NFIB Small Business Optimism Jan | 101.2 | 103 | 104.4 |