Dollar is trying to recover some of the steep losses triggered by much more dovish than expected FOMC economic projections. The greenback is now trading mixed for the day, and it’s indeed up against Sterling and Canadian for the week. Free fall in Germany yield is another factor lifting Dollar, with 10-year bund yield below 0.05 handle. Putting in to context, 10-year bund yield hit as high as 1.2 just two days ago. US stocks open flat in very tight range while 10-year yield stays pressured. We’d pointed out that yield curve between 3-month and 10-year is now on the brink of indicating recession. It may take some more time for investors to decide whether Fed’s dovish turn is positive or negative to the markets.

Back with the currency markets, Sterling suffering another round of selloff as UK Prime Minister Theresa May arrives in Brussels for the EU summit. For now, it’s uncertainty how she could get pass Commons Speaker Bercow to hold another meaningful vote for her Brexit deal, get the deal approved, and the secure short Article 50 extension within a week before March 29. Stronger than expected UK retail sales look irrelevant for traders for now. BoE and SNB rate decisions were also largely ignored. Canadian is the second weakest one, followed by Euro. New Zealand Dollar and Australian Dollar are the strongest ones.

In Europe, currently, FTSE is up 0.46%. DAX is down -0.76%. CAC is down -0.20%. German 10-year yield is down -0.039 at 0.047. Earlier in Asia, Japan was on holiday. Hong Kong HSI dropped -0.85%. China Shanghai SSE rose 0.35%. Singapore Strait Times rose 0.19%.

US initial jobless claims dropped -9k to 221k, Philly Fed manufacturing outlook rose to 13.7

US initial jobless claims dropped -9k to 221k in the week ending March 16, better than expectation of 226k. Four-week moving average of initial claims rose 1k to 225k. Continuing claims dropped -17k to 1.75M in the week ending March 9. Fours week moving average of continuing claims rose 6k to 1.773M.

Philadelphia Manufacturing Business Outlook jumped to 13.7 in March, up from -4.1 and beat expectation of 5. Prior month’s figure was the first negative reading in almost three news. For this month, new orders rose modestly from -2.4 to 1.9. Shipments index jumped 25 pts to 20.0.

BoE kept interest rate at 0.75%, economic projections appear on track

BoE kept Bank Rate at 0.75% and asset purchase target at GBP 435B as widely expected. Both decisions were made by unanimous 9-0 vote. The central bank noted that economic data has been mixed since last meeting, but February Inflation Report projections “appear on track”.

BoE also noted that shifting expectations about the potential nature and timing Brexit have continued to generate volatility in UK asset prices, particularly the sterling exchange rate. Uncertainties also continue to weigh on confidence and short-term economic activity, notably business investment. Employment growth has been strong and indicators of consumer spending point to ongoing modest growth.

Again, BoE noted that the outlook depend significantly on Brexit. And, the policy response to Brexit “will not be automatic and could be in either direction.

Also from UK, retail sales including auto and fuel rose 0.4% mom, 4.0% yoy in February, much better than expectation of -0.4% mom, 3.3% yoy. Retail sales excluding auto and fuel rose 0.2% mom, 4.0% yoy, also much better than expectation of -0.4% mom, 3.5% yoy.

UK May in Brussels, emphasized Brexit is decision of the people

Arriving at the EU summit in Brussels, UK Prime Minister Theresa May repeated that Brexit delay is a “matter of personal regret”. However, “a short extension would give parliament the time to make a final choice that delivers on the result of the referendum.” Also, she emphasized again: “What matters is that we recognise that Brexit is the decision of the British people. We need to deliver on that. We are nearly three years on from the original vote. It is now the time for parliament to decide.”

Earlier today, German Chancellor Angela Merkel echoed the unified message from EU official regarding Article 50 extensions. She said: “There was a request from Theresa May] to delay the exit date to June 30. The leaders of the EU27 will intensively discuss this request. In principle, we can meet this request if we have a positive vote in the British parliament next week about the exit document.

May sent a letter European Council President Donald Tusk yesterday, requesting Article 50 extension until June 30. Tusk offered to give short Article 50 extension. But that would be “conditional on a positive vote on the withdrawal agreement in the House of Commons.” If his proposal is approved by all other 27 EU members, and there is a positive vote in the House of Commons next week, the EU can “finalize and formalize the decision on extension in the written procedure”. Tusk is ready to call for another EU summit next week if needed.

SNB kept interest rate at -0.75%, downgrades inflation forecast

SNB left “expansionary” monetary policy unchanged as widely expected. Sight deposit rate is held at -0.75%. Three-month Libor target range is also kept at -1.25% to -0.25%. The central bank maintained the pledge to “remain active in the foreign exchange market as necessary, while taking the overall currency situation into consideration.”

While Swiss Franc has depreciated slightly since December meeting, SNB said “it is still highly valued” and the currency markets situation remain “fragile”. Thus, negative interest rate and the SNB’s willingness to intervene in the foreign exchange market as necessary therefore remain essential. These measures keep the attractiveness of Swiss franc investments low and reduce upward pressure on the currency.

Inflation forecast in 2019 is downgraded to 0.3%, down from December projection of 0.5%. For 2020, inflation is projected to be at 0.6%, down from 1.0%. For 2020, inflation is projected to pick up to 1.2%. The forecasts are based on keeping three-month Libor rate at -0.75% over the entire horizon. On growth, SNB expects GDP to grow by around 1.5% in 2019 as a whole.

Suggested reading: SNB Downgraded Inflation Forecast for Switzerland, Pledged to Curb Franc’s Strength

Australia unemployment rate dropped to 4.9% as participation rate dropped -0.2%

In seasonally adjusted term, Australian employment market grew 4.6k in February, well below expectation of 15.2k. Full-time employment dropped -7.3k while part-time jobs grew 11.9k. Unemployment rate dropped to 4.9%, down from 5.0%. That’s also the lowest level since June 2011. However, participation rate dropped by -0.2% to 65.6%.

The seasonally adjusted unemployment rate increased in New South Wales (up 0.3 pts to 4.3%) and Victoria (up 0.2 pts to 4.8%). Decreases were observed in Western Australia (down 0.9 pts to 5.9%), Queensland (down 0.6 pts to 5.4%), South Australia (down 0.6 pts to 5.7%) and Tasmania (down 0.5 pts to 6.5%).

ABS Chief Economist Bruce Hockman said: “The trend unemployment rate declined 0.5 percentage points over the year, from 5.5 per cent to 5.0 per cent. The pace of decline slowed in recent months, which was consistent with the slowdown seen in recent Job Vacancies and GDP numbers.”

New Zealand GDP grew 0.6% qoq, led by services

New Zealand GDP grew 0.6% qoq in Q4, up from Q3’s 0.3% qoq and matched expectations. GDP grew 2.8% over the year ended December 2018. While the 0.6% growth missed RBNZ’s forecast of 0.8%, it may not be weak enough to prompt an RBNZ rate cut in this month’s meeting yet.

Looking at the details, growth was driven by services industries which rose 0.9%, with 9 of 11 services industries recording increases. Agriculture, forestry, and fishing industry contracted -0.6%. construction rose 1.8%. Household spending rose 1.3%. Investment spending rose 1.4%.

China MOFCOM confirms USTR Lighthizer’s visit on Mar 28-29

China Commerce Ministry spokesman Gao Feng confirmed in a regular press briefing that US delegation is traveling to Beijing next week to continue trade negotiation. Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin will visit China on March 28-29. After that Vice Premier Liu He will travel to the Washington in early April for more talks.

Gao also noted that the decline is import and expect during the first two months of the year was mainly due to Chinese New Year. He noted the typical pattern of “concentrated export pre CNG, concentrated import post CNY”. Though, he also said trade rebounded strongly during the first half of March. And, Q1 trade will remain stability.

Trump said yesterday that administration is talking about leaving tariffs on China for a long period of time. That is, even if a trade agreement is reached, the tariffs won’t be limited until China complies with the terms of the deal. He criticized that China “had a lot of problems living by certain deals.”

His comments were generally seen as counter-productive to the negotiation, as well as the world economy. Without US stopping the punitive tariffs, China will certainly not agree to correcting its unfair trade practice while lifting its own retaliatory tariffs at the same time. The US won’t have it all. That is, even if there is an eventual agreement and China will speed up it’s reforms, tariffs from both sides will stay there for much longer. The damage to the world economy would continue.

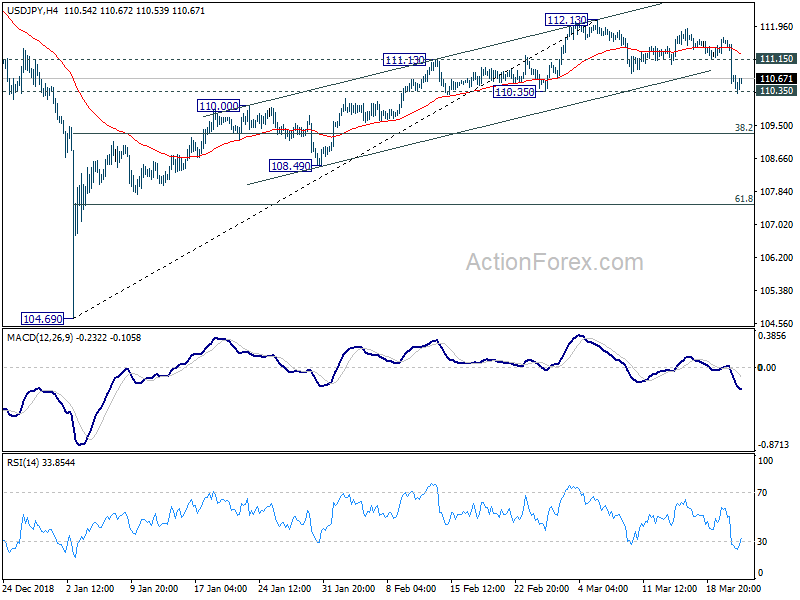

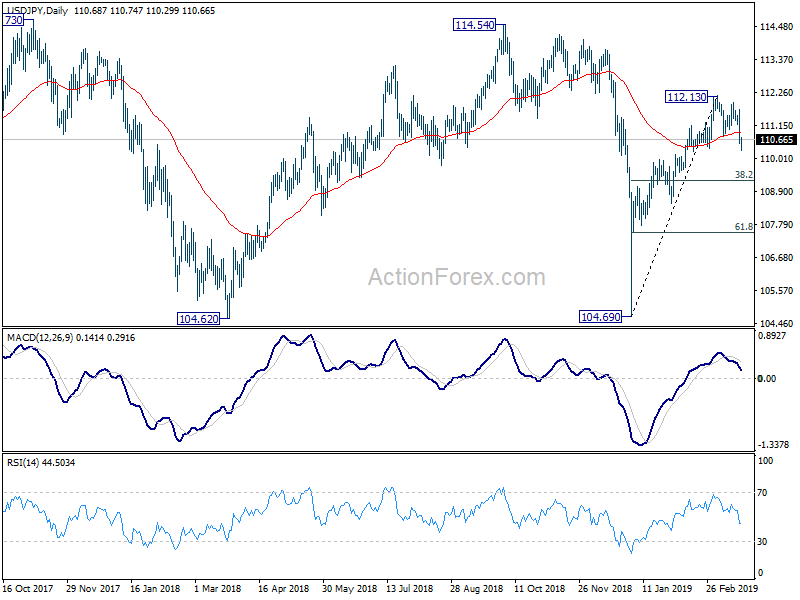

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.25; (P) 110.98; (R1) 111.42; More…

USD/JPY breaches 110.35 to 110.30 but quickly recovered. It’s still holding on to 110.35 support and intraday bias remains neutral first. On the downside, decisive break there will confirm that whole rebound from 104.69 has completed at 112.13. In that case, deeper fall should be seen back to 38.2% retracement of 104.69 to 112.13 at 109.28 next. On the upside, break of 111.15 minor resistance will turn bias back to the upside for retesting 112.13 high instead.

In the bigger picture, strong rebound from 104.69 argues that decline from 118.65 (2016 high) has completed with three waves down to 104.69, after failing 104.62. More importantly, the rise from 98.97 (2016 low) could be resuming. Decisive break of 114.54 resistance will add more credence to this bullish case and target 118.65. This will now be the favored case as long as 110.35 support holds. However, firm break of 110.35 will mix up the medium term outlook again and turn focus back to 104.69 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | GDP Q/Q Q4 | 0.60% | 0.60% | 0.30% | |

| 00:30 | AUD | Employment Change Feb | 4.6K | 15.2K | 39.1K | 38.3K |

| 00:30 | AUD | Unemployment Rate Feb | 4.90% | 5.00% | 5.00% | |

| 08:30 | CHF | SNB Sight Deposit Interest Rate | -0.75% | -0.75% | -0.75% | |

| 08:30 | CHF | SNB 3-Month Libor Upper Target Range | -0.25% | -0.25% | -0.25% | |

| 08:30 | CHF | SNB 3-Month Libor Lower Target Range | -1.25% | -1.25% | -1.25% | |

| 09:00 | EUR | ECB Monthly Bulletin | ||||

| 09:30 | GBP | Public Sector Net Borrowing (GBP) Feb | -0.7B | -0.3B | -15.8B | |

| 09:30 | GBP | Retail Sales Inc Auto Fuel M/M Feb | 0.40% | -0.40% | 1.00% | 0.90% |

| 09:30 | GBP | Retail Sales Inc Auto Fuel Y/Y Feb | 4.00% | 3.30% | 4.20% | 4.10% |

| 09:30 | GBP | Retail Sales Ex Auto Fuel M/M Feb | 0.20% | -0.40% | 1.20% | 1.10% |

| 09:30 | GBP | Retail Sales Ex Auto Fuel Y/Y Feb | 4.00% | 3.50% | 4.10% | |

| 12:00 | GBP | BoE Rate Decsion | 0.75% | 0.75% | 0.75% | |

| 12:00 | GBP | BoE Asset Purchase Target Mar | 435B | 435B | 435B | |

| 12:00 | GBP | MPC Official Bank Rate Votes | 0–0–9 | 0–0–9 | 0–0–9 | |

| 12:00 | GBP | MPC Asset Purchase Facility Votes | 0–0–9 | 0–0–9 | 0–0–9 | |

| 12:30 | CAD | Wholesale Trade Sales M/M Jan | 0.60% | 0.50% | 0.30% | |

| 12:30 | USD | Philadelphia Fed Business Outlook Mar | 13.7 | 5 | -4.1 | |

| 12:30 | USD | Initial Jobless Claims (MAR 16) | 221K | 226K | 229K | 230K |

| 14:00 | USD | Leading Index Feb | 0.2% | 0.10% | -0.10% | |

| 14:30 | USD | Natural Gas Storage | -49B | -204B |

{kind=link}