Australian and New Zealand Dollars have very different fortunes today. Aussie was boosted higher by stronger than expected Chinese data. On the other hand, Kiwi dived as weaker than expected CPI raises the chance of RBNZ rate cut at next meeting. In between, Euro is the second strongest so far, followed by Sterling. Dollar is the second weakest, followed by Yen. Focus will turn to more inflation data from UK and Canada today.

Technically, AUD/USD’s choppy rise resumed and edged higher to 0.7205. Further rise is mildly in favor towards 0.7295 resistance. EUR/AUD’s break of 1.5721 support now suggests resumption of fall form 1.6765. USD/JPY edged higher and breached 112.13 key resistance. But there is no follow through buying to push it through this key resistance yet.

In Asia, Nikkei is currently up 0.30%. Hong Kong HSI is down -0.13%. China Shanghai SSE is up 0.15%. Singapore Strait Times is up 0.44%. Japan 10-year JGB yield is up 0.012 at -0.008. Overnight, DOW rose 0.26%. S&P 500 rose 0.05%. NASDAQ rose 0.30%. 10-year yield rose 0.039 to 2.592. 10-year yield could have a take on 2.6 handle today and firm break could give Dollar a lift.

China Q1 GDP grew 6.4%. Production, sales, investment rebounded

Another batch of data from China released today surprised on the upside. GDP growth came in at 6.4% yoy in Q1, unchanged from prior quarter and beat expectation of 6.3% yoy.

In March, industrial production rose strongly by 8.5% ytd yoy, accelerated from 5.3% and beat expectation of 5.6%. Retail sales rose 8.7% ytd yoy, up fro 8.2% and beat expectation of 8.3%. Fixed asset investment rose 6.3% ytd yoy, up from 6.1% yoy and matched expectation of 6.3%. Jobless rate also improved from 5.3% to 5.2%.

Recent data from China continued to paint the picture of stabilization in slowdown, and raised hope that recovery is on the way. That’s an important condition for improvement in global outlook.

New Zealand CPI slowed to 1.5%, solidifies need for imminent RBNZ easing

New Zealand Dollar drops sharply after worse than expected consumer inflation data. CPI rose 0.1% qoq in Q1, below expectation of 0.3% qoq. Annually, CPI slowed to 1.5% yoy, down from 1.9% yoy and missed expectation of 1.7% yoy. Tradeable CPI dropped -0.4% yoy while non-tradeable CPI rose 2.8% yoy.

CPI has been persistently weak and remained below mid-point of RBNZ’s 1-3% target range for the eight consecutive quarter. Indeed, CPI has only breached 2% level once in Q1 2017 (2.2%) since 2011. Yesterday, RBNZ Governor Adrian Orr noted that “possibilities of first quarter inflation numbers being undershot have already being factored in the RBNZ’s dovish bias”. The downside surprise is giving Orr an even worse picture and solidifies the imminent need for policy easing.

From Australia, Westpac leading index rose 0.2% mom in March.

Japan exports slumped in March, raised concerns of Q1 GDP contraction

In March, in trend terms, Japan’s exports dropped -2.4% yoy to JPY 7.20T. Imports rose 1.1% yoy to JPY 6.67T. Trade surplus came in at JPY 0.53T, up from prior month’s JPY 0.33T. In seasonally adjusted terms, exports dropped -1.0% yoy to JPY 6.61T. Imports rose 2.1% yoy to JPY 6.78T. Trade deficit was at JPY -0.18T.

Exports to China, Japan’s largest trading partner, dropped -9.4% yoy, reversing from 5.6% growth in February. Exports to Asia as a whole dropped -5.5% yoy, a fifth straight month of decline. The slump in exports could drag down capital expenditure and private consumption growth . And it raised concerns that the economy contracted again in Q1.

Also from Japan, industrial production was finalized at 0.7% mom in February.

US raised very large trade deficit with Japan during trade talks

The US Trade Representative issued a statement regarding the meeting of USTR Robert Lighthizer and Japan’s Economic Revitalization Minister Toshimitsu Motegi on April 15-16 in Washington.

In the statement, it’s noted that US and Japan “discussed trade issues involving goods, including agriculture, as well as the need to establish high standards in the area of digital trade”. Also, US raised its “very large trade deficit with Japan – $67.6 billion in goods in 2018.” Both sides agreed to meet again in the “near future to continue these talks”.

Motegi said yesterday that no agreement has been made. But he hoped to reach a “good result” on the talks “at an early stage.” There will be further discussions next week before the US-Japan summit. Meanwhile, discussions regarding exchange rate would be left to finance ministers.

Amamiya: BoJ mindful of risks including financial imbalances

BoJ Deputy Governor Masayoshi Amamiya said the central bank is “ready to respond” financial crisis threatens the stability of the banking system.

He pointed to experience in the late 1980s, and noted “one of the factors that led to Japan’s asset-inflated bubble was the fact we kept monetary policy easy even as the economy continued to expand”. Hence, “the BOJ must be mindful of the potential risks to the economy and prices, including financial imbalances,”

Regarding monetary policy, Amamiya said “we’re ready to respond if financial problems have a big impact on the economy.”

Looking ahead

UK inflation data will be a major focus in European session with CPI, RPI, PPI and house price featured. Eurozone will release current account, trade balance and CPI final. Later in the day, Canada will release CPI. US will release trade balance, wholesale inventories and Fed’s Beige Book economic report.

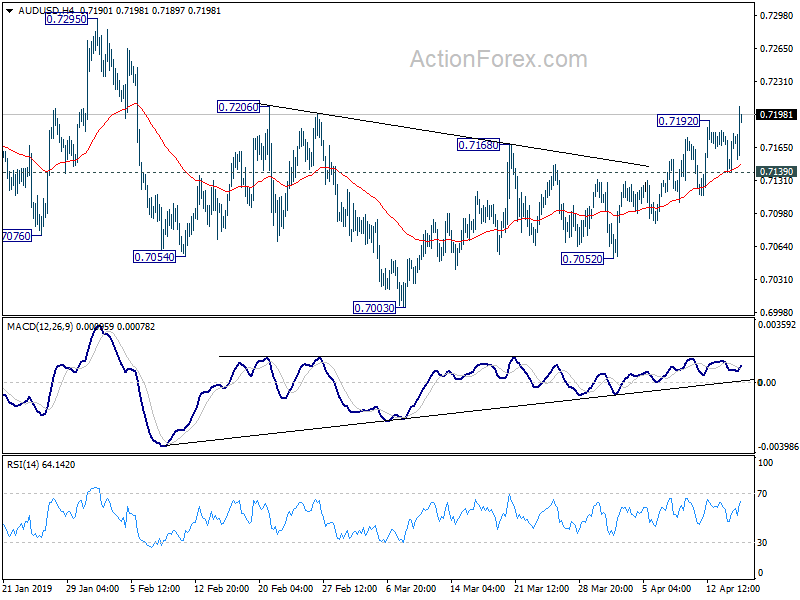

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7149; (P) 0.7165; (R1) 0.7190; More…

AUD/USD’s choppy rise from 0.7003 resumed by taking out 0.7192 and reaches as high as 0.7205 so far. Intraday bias is back on the upside for 0.7295 resistance. Upside momentum is relatively weak and structure of the recovery is corrective looking. Thus, upside could be limited by 0.7295 to bring near term reversal. On the downside, break of 0.7139 minor support will turn intraday bias back to the downside for 0.7003/7052 support zone instead.

In the bigger picture, break of medium term channel resistance is the first sign of bullish reversal. But there is no confirmation yet. As long as 0.7393 resistance holds, larger fall from 0.8135 is still expected to resume later. Such decline is seen as resuming long term down trend from 1.1079 (2011 high). Decisive break of 0.6826 (2016 low) will confirm this bearish view and resume the down trend to 0.6008 (2008 low). However, firm break of 0.7393 will argue that fall from 0.8135 has completed. And corrective pattern from 0.6826 has started the third leg, targeting 0.8135 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | CPI Q/Q Q1 | 0.10% | 0.30% | 0.10% | |

| 22:45 | NZD | CPI Y/Y Q1 | 1.50% | 1.70% | 1.90% | |

| 23:50 | JPY | Trade Balance (JPY) Mar | -0.18T | -0.30T | 0.12T | 0.03T |

| 0:30 | AUD | Westpac Leading Index M/M Mar | 0.20% | 0.00% | ||

| 2:00 | CNY | GDP Y/Y Q1 | 6.40% | 6.30% | 6.40% | |

| 2:00 | CNY | Industrial Production YTD Y/Y Mar | 8.50% | 5.60% | 5.30% | |

| 2:00 | CNY | Retail Sales YTD Y/Y Mar | 8.70% | 8.30% | 8.20% | |

| 2:00 | CNY | Fixed Assets Ex Rural YTD Y/Y Mar | 6.30% | 6.30% | 6.10% | |

| 2:00 | CNY | Surveyed Jobless Rate Mar | 5.20% | 5.30% | ||

| 4:30 | JPY | Industrial Production M/M Feb F | 0.70% | 1.40% | 1.40% | |

| 8:00 | EUR | Eurozone Current Account (EUR) Feb | 33.2B | 36.8B | ||

| 8:30 | GBP | CPI M/M Mar | 0.20% | 0.50% | ||

| 8:30 | GBP | CPI Y/Y Mar | 2.00% | 1.90% | ||

| 8:30 | GBP | Core CPI Y/Y Mar | 1.90% | 1.80% | ||

| 8:30 | GBP | RPI M/M Mar | 0.20% | 0.70% | ||

| 8:30 | GBP | RPI Y/Y Mar | 2.60% | 2.50% | ||

| 8:30 | GBP | PPI Input M/M Mar | 0.50% | 0.60% | ||

| 8:30 | GBP | PPI Input Y/Y Mar | 4.10% | 3.70% | ||

| 8:30 | GBP | PPI Output M/M Mar | 0.30% | 0.10% | ||

| 8:30 | GBP | PPI Output Y/Y Mar | 2.20% | 2.20% | ||

| 8:30 | GBP | PPI Output Core M/M Mar | 0.10% | 0.10% | ||

| 8:30 | GBP | PPI Output Core Y/Y Mar | 2.20% | 2.20% | ||

| 8:30 | GBP | House Price Index Y/Y Feb | 1.30% | 1.70% | ||

| 9:00 | EUR | Eurozone Trade Balance (EUR) Feb | 16.8B | 17.0B | ||

| 9:00 | EUR | Eurozone CPI M/M Mar | 0.30% | 0.30% | ||

| 9:00 | EUR | Eurozone CPI Y/Y Mar F | 1.40% | 1.50% | ||

| 9:00 | EUR | Eurozone CPI Core Y/Y Mar F | 0.80% | 0.80% | ||

| 12:30 | CAD | International Merchandise Trade (CAD) Feb | 3.50B | -4.25B | ||

| 12:30 | CAD | CPI M/M Mar | 0.60% | 0.70% | ||

| 12:30 | CAD | CPI Y/Y Mar | 1.30% | 1.50% | ||

| 12:30 | CAD | CPI Core – Common Y/Y Mar | 1.80% | |||

| 12:30 | CAD | CPI Core – Median Y/Y Mar | 1.80% | |||

| 12:30 | CAD | CPI Core – Trim Y/Y Mar | 1.90% | |||

| 12:30 | USD | Trade Balance (USD) Feb | -53.5B | -51.1B | ||

| 14:00 | USD | Wholesale Inventories M/M Feb | 0.40% | 1.20% | ||

| 14:30 | USD | Crude Oil Inventories | 7.0M | |||

| 18:00 | USD | Federal Reserve Beige Book |

{kind=link}