Global treasury yields are boosted by solid data from China today. German 10-year yield hit at high as 0.104 and is now back at around 0.08. US 10-year yield breaches hit 2.614 and it’s now trying to own 2.6 handle. These are both signs of improvements in market sentiments as stabilization in China’s slowdown is a key factor for rebound in global economy in the second half. Though, such optimism is not much reflected in the overbought stocks, especially in the US. DOW just open the day flat, slightly in red.

In the currency markets, Australian Dollar is a clear winner for most of the day. However, Canadian takes over as the strongest one after core CPI unexpectedly accelerated in March. Euro is the third strongest for now, shrugging off German government’s growth outlook downgrade. New Zealand Dollar is the weakest one for today as poor CPI data raises the chance of an imminent RBNZ rate cut at next meeting. Swiss Franc is the second weakest, followed by Sterling, while UK CPI failed to accelerate.

In the US, DOW is currently down -0.16%. S&P 500 is up 0.07%. NASDAQ is up 0.36%. 10-year yield is up 0.0030 at 2.599. In Europe, FTSE is up 0.04%. DAX is up 0.72%. CAC is up 0.66%. German 10-year yield is up 0.009 at 0.080. Earlier in Asia, Nikkei rose 0.25%. Hong Kong HSI dropped -0.02%. China Shanghai SSE rose 0.29%. Singapore Strait Times rose 0.50%. Japan 10-year JGB yield rose 0.01 to -0.01.

Canadian dollar jumps as core CPI accelerated in March

Canadian Dollar rises in early US session as core inflation came in higher than expected. Headline CPI rose 1.9% yoy in March, accelerated from 1.5% yoy but matched expectation. CPI core common was unchanged at 1.8% yoy, matched expectations. However, CPI core median accelerated to 2.0% yoy, up from 1.8% yoy and beat expectation os 1.8% yoy. CPI core trim rose to 2.1% yoy, up from 1.9% yoy and beat expectation of 1.8% yoy.

Also from released, Canada trade surplus was smaller than expected at CAD 2.9B in February. US trade deficit narrowed to USD -49.4B in February.

UK CPI unchanged at 1.9%, core at 1.8%, Sterling steady

In March, UK CPI was unchanged at 1.9% yoy, below expectation of 2.0% yoy. Core CPI was also unchanged at 1.8% yoy, below expectation of 1.9% yoy. RPI slowed to 2.4% yoy, down from 2.5% yoy and miss expectation of 2.6% yoy.

PPI input dropped -0.2% mom, rose 3.7% yoy, below expectation of 0.3% mom, 3.9% yoy. PPI output rose 0.3% mom, 2.4% yoy, versus expectation of 0.2% mom, 2.1% yoy. PPI output core rose 0.02% mom, 2.2% yoy versus expectation of 0.1% mom, 2.2% yoy.

House price index rose 0.6% yoy in February, well below expectation of 1.3% yoy.

Eurozone CPI confirmed at 1.4%, core at 0.8%

Eurozone CPI was finalized at 1.4% yoy in March, unrevised, down from 1.5% yoy in February. Core CPI was finalized at 0.8% yoy, unchanged from February’s reading. EU28 inflation was confirmed at 1.6% yoy.

The highest contribution to the annual euro area inflation rate came from energy (+0.52 percentage points, pp), followed by services (+0.51 pp), food, alcohol & tobacco (+0.34 pp) and non-energy industrial goods (+0.04 pp).

Germany halves 2019 growth forecast to 0.5%

Germany’s Economy Ministry lowered 2019 growth forecast to a mere 0.5%, just half of January’s projection of 1.0% (downgraded from 1.8%). If realized, that would be slowest growth in six years. For 2020m, growth is projected to pick up to 1.5%.

Economy Minister Peter Altmaier said externally, slowing global growth, trade tensions and Brexit uncertainty are weighing on the economy. Internally, introduction of the new car emission regulations and unusually low Rhine water levels are negative factors.

The ministry also noted that global economy should regain some momentum ahead. Strong import would mean a negative contribution to growth in 2019, “purely mathematically”.

China Q1 GDP grew 6.4%. Production, sales, investment rebounded

Another batch of data from China released today surprised on the upside. GDP growth came in at 6.4% yoy in Q1, unchanged from prior quarter and beat expectation of 6.3% yoy.

In March, industrial production rose strongly by 8.5% ytd yoy, accelerated from 5.3% and beat expectation of 5.6%. Retail sales rose 8.7% ytd yoy, up fro 8.2% and beat expectation of 8.3%. Fixed asset investment rose 6.3% ytd yoy, up from 6.1% yoy and matched expectation of 6.3%. Jobless rate also improved from 5.3% to 5.2%.

Recent data from China continued to paint the picture of stabilization in slowdown, and raised hope that recovery is on the way. That’s an important condition for improvement in global outlook.

New Zealand CPI slowed to 1.5%, solidifies need for imminent RBNZ easing

New Zealand Dollar drops sharply after worse than expected consumer inflation data. CPI rose 0.1% qoq in Q1, below expectation of 0.3% qoq. Annually, CPI slowed to 1.5% yoy, down from 1.9% yoy and missed expectation of 1.7% yoy. Tradeable CPI dropped -0.4% yoy while non-tradeable CPI rose 2.8% yoy.

CPI has been persistently weak and remained below mid-point of RBNZ’s 1-3% target range for the eight consecutive quarter. Indeed, CPI has only breached 2% level once in Q1 2017 (2.2%) since 2011. Yesterday, RBNZ Governor Adrian Orr noted that “possibilities of first quarter inflation numbers being undershot have already being factored in the RBNZ’s dovish bias”. The downside surprise is giving Orr an even worse picture and solidifies the imminent need for policy easing.

From Australia, Westpac leading index rose 0.2% mom in March.

Japan exports slumped in March, raised concerns of Q1 GDP contraction

In March, in trend terms, Japan’s exports dropped -2.4% yoy to JPY 7.20T. Imports rose 1.1% yoy to JPY 6.67T. Trade surplus came in at JPY 0.53T, up from prior month’s JPY 0.33T. In seasonally adjusted terms, exports dropped -1.0% yoy to JPY 6.61T. Imports rose 2.1% yoy to JPY 6.78T. Trade deficit was at JPY -0.18T.

Exports to China, Japan’s largest trading partner, dropped -9.4% yoy, reversing from 5.6% growth in February. Exports to Asia as a whole dropped -5.5% yoy, a fifth straight month of decline. The slump in exports could drag down capital expenditure and private consumption growth . And it raised concerns that the economy contracted again in Q1.

Also from Japan, industrial production was finalized at 0.7% mom in February.

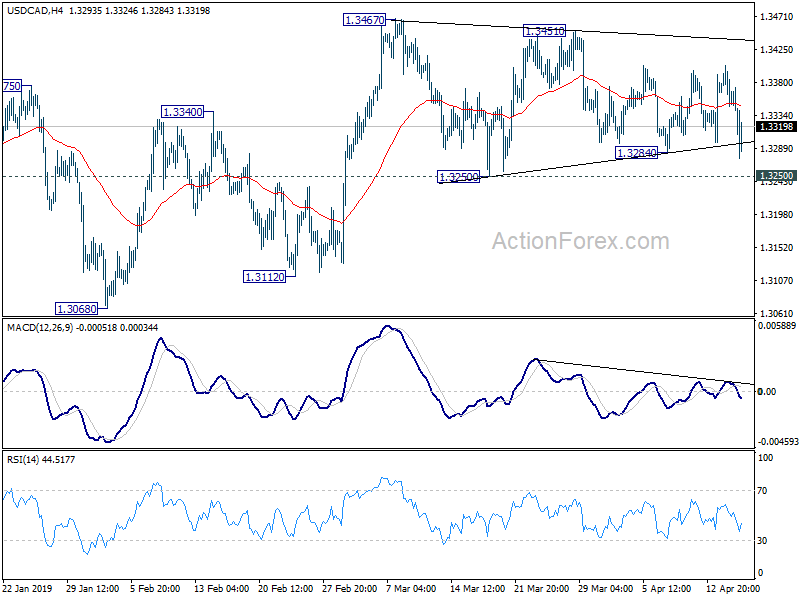

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3329; (P) 1.3366; (R1) 1.3387; More…

USD/CAD drops sharply to as low as 1.3274 but stays above 1.3250 support. Outlook is unchanged and intraday bias remains neutral. Consolidation from 1.3467 is in progress and could extend, but upside breakout is expected sooner or later. On the upside, firm break of 1.3467 will confirm this bullish case and target 1.3664 resistance next. However, decisive break of 1.3250 will turn bias back to the downside for 1.3068/3112 support zone instead.

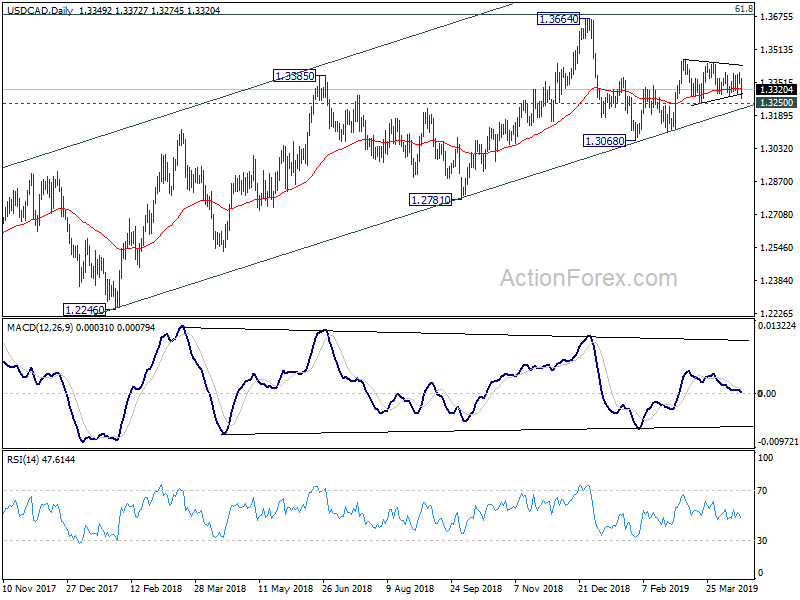

In the bigger picture, USD/CAD is staying well inside medium term rising channel (support at 1.3212). Thus, even though upside momentum and structure are unconvincing, further rise is still in favor. Decisive break of 61.8% retracement of 1.4689 (2016 high) to 1.2061 at 1.3685 and 1.3793 will pave the way to retest 1.4689 (2015 high). However, firm break of the channel support should indicate bearish reversal, after rejection by 1.3793, and bring deeper fall to 1.3068 support for confirmation.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | CPI Q/Q Q1 | 0.10% | 0.30% | 0.10% | |

| 22:45 | NZD | CPI Y/Y Q1 | 1.50% | 1.70% | 1.90% | |

| 23:50 | JPY | Trade Balance (JPY) Mar | -0.18T | -0.30T | 0.12T | 0.03T |

| 00:30 | AUD | Westpac Leading Index M/M Mar | 0.20% | 0.00% | ||

| 02:00 | CNY | GDP Y/Y Q1 | 6.40% | 6.30% | 6.40% | |

| 02:00 | CNY | Industrial Production YTD Y/Y Mar | 8.50% | 5.60% | 5.30% | |

| 02:00 | CNY | Retail Sales YTD Y/Y Mar | 8.70% | 8.30% | 8.20% | |

| 02:00 | CNY | Fixed Assets Ex Rural YTD Y/Y Mar | 6.30% | 6.30% | 6.10% | |

| 02:00 | CNY | Surveyed Jobless Rate Mar | 5.20% | 5.30% | ||

| 04:30 | JPY | Industrial Production M/M Feb F | 0.70% | 1.40% | 1.40% | |

| 08:00 | EUR | Eurozone Current Account (EUR) Feb | 26.8B | 33.2B | 36.8B | |

| 08:30 | GBP | CPI M/M Mar | 0.20% | 0.20% | 0.50% | |

| 08:30 | GBP | CPI Y/Y Mar | 1.90% | 2.00% | 1.90% | |

| 08:30 | GBP | Core CPI Y/Y Mar | 1.80% | 1.90% | 1.80% | |

| 08:30 | GBP | RPI M/M Mar | 0.00% | 0.20% | 0.70% | |

| 08:30 | GBP | RPI Y/Y Mar | 2.40% | 2.60% | 2.50% | |

| 08:30 | GBP | PPI Input M/M Mar | -0.20% | 0.50% | 0.60% | 1.00% |

| 08:30 | GBP | PPI Input Y/Y Mar | 3.70% | 4.10% | 3.70% | 4.00% |

| 08:30 | GBP | PPI Output M/M Mar | 0.30% | 0.30% | 0.10% | 0.30% |

| 08:30 | GBP | PPI Output Y/Y Mar | 2.40% | 2.20% | 2.20% | 2.40% |

| 08:30 | GBP | PPI Output Core M/M Mar | 0.00% | 0.10% | 0.10% | 0.20% |

| 08:30 | GBP | PPI Output Core Y/Y Mar | 2.20% | 2.20% | 2.20% | 2.30% |

| 08:30 | GBP | House Price Index Y/Y Feb | 0.60% | 1.30% | 1.70% | |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Feb | 19.5B | 16.8B | 17.0B | 17.4B |

| 09:00 | EUR | Eurozone CPI M/M Mar | 1.00% | 0.30% | 0.30% | |

| 09:00 | EUR | Eurozone CPI Y/Y Mar F | 1.40% | 1.40% | 1.50% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Mar F | 0.80% | 0.80% | 0.80% | |

| 12:30 | CAD | International Merchandise Trade (CAD) Feb | 2.90B | 3.50B | -4.25B | -3.09B |

| 12:30 | CAD | CPI M/M Mar | 0.70% | 0.60% | 0.70% | |

| 12:30 | CAD | CPI Y/Y Mar | 1.90% | 1.90% | 1.50% | |

| 12:30 | CAD | CPI Core – Common Y/Y Mar | 1.80% | 1.80% | 1.80% | |

| 12:30 | CAD | CPI Core – Median Y/Y Mar | 2.00% | 1.80% | 1.80% | |

| 12:30 | CAD | CPI Core – Trim Y/Y Mar | 2.10% | 1.80% | 1.90% | |

| 12:30 | USD | Trade Balance (USD) Feb | -49.4B | -53.5B | -51.1B | |

| 14:00 | USD | Wholesale Inventories M/M Feb | 0.40% | 1.20% | ||

| 14:30 | USD | Crude Oil Inventories | 1.6M | 7.0M | ||

| 18:00 | USD | Federal Reserve Beige Book |

{kind=link}