Yen and Swiss Franc are finally showing some strength today. There was no special escalation in US-China relationship as the former refrained from naming the latter as currency manipulator. But recovery attempts in stocks were rather short lived. Selloff in stocks is in tandem with free fall in treasury yields, which is started in Germany yesterday, passed to the US, then back to Germany again today. Commodity currencies are generally back under pressure today. Euro and Dollar are mixed.

Technically, EUR/JPY finally broke 122.08 support to resume recent fall from 127.05. We’d maintain the bearish view that 118.62 low is the next target, and will pay attention to sign of downside acceleration. EUR/CHF’s recovery also faltered ahead of 1.1292 minor resistance. Thus, there is no confirmation on near term bullish reversal. Focus could be quickly back to 1.1162 key support level. USD/CAD is showing some strength today and could have a take on 1.3521 resistance. Though, whether USD/CAD could firmly breakout from recent range will eventually depend much on BoC rate statement.

In other markets, currently, all major European indices, FTSE, DAX and CAC open mildly lower. German 10-year yield is down -0.0024 at -0.16. In Asia, Nikkei dropped -1.21%. Hong Kong HSI is down -0.42%. China Shanghai SSE bucked the trend is gained 0.21%. Singapore Strait Times is down -0.33%. Japan 10-year JGB yield is down -0.0239 at -0.095. Overnight, DOW dropped -0.93%. S&P 500 dropped -0.84%. NASDAQ dropped -0.39%. 10-year yield extended recent steel fall to 2.268, down -0.056.

US Treasury said limited Yuan intervention seen, but urges China to avoid a persistently weak currency

US Treasury announced that nine countries are put in the “monitoring list” on currency manipulation, but no major trading partner is named as manipulator. The nine countries include China, Germany, Ireland, Italy, Japan, Korea, Malaysia, Singapore, and Vietnam. That conclusion was made even after the Treasury revised and updated the thresholds it uses to assess where unfair currency practices or imbalanced macroeconomic policies may be emerging.

In the statement, US Treasury Secretary Steven Mnuchin singled out China and said “Treasury will continue its enhanced bilateral engagement with China regarding exchange rate issues, given that the RMB has fallen against the dollar by eight percent over the last year in the context of an extremely large and widening bilateral trade surplus.”

US Treasury also estimated that “direct intervention by the People’s Bank of China in the last year has been limited.” But it surged China to “take the necessary steps to avoid a persistently weak currency”. Also, it urged China to aggressively address market-distorting forces, including subsidies and state-owned enterprises, enhance social safety nets to support greater household consumption growth, and rebalance the economy away from investment.

EU to decide next Commission and ECB Presidents in June

EU28 leaders agreed to have swift process on choosing the next European Commission and ECB Presidents in a meeting overnight. The decision would be made at a June 20-21 summit. But for now, Germany and France seem to be at odds over the choices. German Chancellor Angela Merkel is standing by the center-right German lawmaker Manfred Weber to succeed Jean-Claude Juncker and Commission President. But Weber is seen as is failing to gain traction. French President Emmanuel Macron appeared to be pushing for Brexit negotiator Michel Barnier as a compromise.

Macron told reporters after the summit that “the key for me is for the people at the most sensitive positions to share our project and be the most charismatic, creative and competent possible.” On the other hand, Merkel bluntly said “I am warning against telling the EU Parliament that somebody who has only made experiences in parliament is not experienced… And that somebody who has made experiences in the Commission, is experienced. We shouldn’t deal with each other in this currency.”

Meanwhile, at least five candidates are believed to be running to succeed Mario Draghi as ECB Presidents. Contenders include Bank of France Governor Francois Villeroy de Galhau, Finland’s Olli Rehn and Erkki Liikanen, and Bundesbank President Jens Weidmann. Chances of Weidmann and de Galhau will depend on who takes the Juncker’s job.

BoJ Kuroda: Best to manage inflation expectations with flexible targeting framework

In academic conference organized by BoJ, Governor Haruhiko Kuroda expressed his openness to flexible inflation targeting. Former ECB President Jean-Claude Trichet also emphasized that medium- to long-term inflation expectations are what really matter.

Kuroda said “If missing inflation comes from structural factors such as globalization and digitalization, central banks should continue examining how best to manage inflation expectations .. within the flexible inflation targeting framework.” He also noted the need to expand the policy tools to fight the next downturn. “While policy makers have developed a wide range of unconventional policy tools, their effectiveness and transmission mechanisms may differ depending on financial conditions and economic structure,” Kuroda said.

Trichet also said it’s not necessary for central banks to target exactly the same level of inflation in a set period of time. Instead, “there is a consensus among central banks that real success is to solidly anchor inflation expectations in the medium- to long-term in line with their definition of price stability.”

New Zealand ANZ business confidence improved to -32.0

New Zealand ANZ Business Confidence rose to -32.0 in May, up from -37.5. But all sectors remained deeply negative, with agriculture confidence worst at -63.9. Activity Outlook also improved to 8.5, up from 7.1. Manufacturing scored best in activity at 21.5.

ANZ noted that “how quickly the economy will bounce back is a key question. If the forward indicators start to suggest that the Reserve Bank’s relatively sharp V-shaped recovery is overly optimistic, it will be game on for further OCR cuts this year.”

Looking ahead, BoC expected to stand pat

Canadian Dollar is trading mixed as markets await BoC rate decision. BoC is widely expected to keep policy rate unchanged at 1.75%. At last meeting in April, BoC removed chance of rate hike in the near- to medium- term. The central bank also downgraded GDP growth forecast, and lowered the range of neutral rate.

Economic data released since then showed not special deterioration. Headline CPI accelerated to 2.0% yoy but BoC’s preferred gauges of inflation – trimmed CPI, median CPI and common CPI – either eased or stayed unchanged, giving an average reading of +1.9%, down slightly from March’s +1.97%. Job market grew strongly by 106.5k. GDP contracted -0.1% mom in February but 0.3% mom rebound is expected in March. This would probably translate to an annualized growth of 0.7% qoq in 1Q19.

BoC Governor Stephen Poloz said recently that , “the natural tendency is for interest rates to still go up a bit”. Though, that depends on whether the slowdown is temporary. Though, Poloz is uncertain about the size and timing of the rate hike. Overall, we’re not expecting any drastic change with today’s announcement.

Here are some suggested readings on BoC:

- BOC to Avoid Hinting Rate Hike Despite Improvement in Economic Data

- Will the BoC Strike a More Confident Tone at its May Meeting?

- Forward Guidance: International Trade Tensions Unlikely to Sway the Bank of Canada Rate Decision

On the data front, Swiss will release KOF economic barometer. Germany will release unemployment.

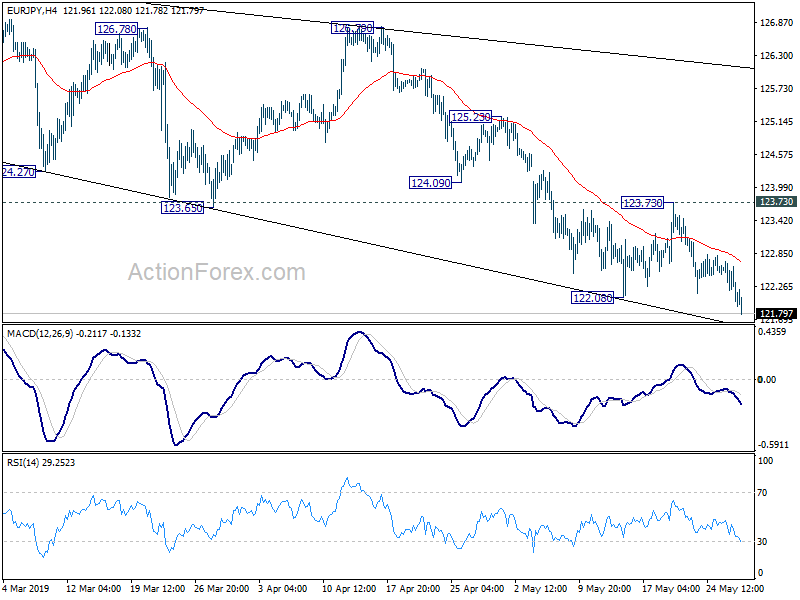

EUR/JPY Daily Outlook

Daily Pivots: (S1) 121.80; (P) 122.26; (R1) 122.51; More….

EUR/JPY drops to as low as 121.79 today. Break of 122.08 support indicates resumption of whole fall from 127.50. Intraday bias is back on the downside. Current fall should target a test on 118.62 low next. On the upside, break of 123.73 resistance is needed to signal short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, current development argues that rebound from 118.62 is merely a correction and has completed at 127.50. EUR/JPY is staying in long term falling channel from 137.49 (2018 high). Decisive break of 118.62 will confirm resumption of this medium term fall and target 109.20 low. For now, this will be the favored case as long as 125.23 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:00 | NZD | RBNZ Financial Stability Report | ||||

| 23:01 | GBP | BRC Shop Price Index Y/Y May | 0.80% | 0.40% | ||

| 1:00 | NZD | ANZ Business Confidence May | -32.0 | -37.5 | ||

| 6:45 | EUR | French GDP Q/Q Q1 F | 0.30% | 0.30% | 0.30% | |

| 7:00 | CHF | KOF Economic Barometer May | 96.2 | 96.2 | ||

| 7:55 | EUR | German Unemployment Change (000’s) May | -8K | -12K | ||

| 7:55 | EUR | German Unemployment Claims Rate May | 4.90% | 4.90% | ||

| 8:00 | EUR | ECB Financial Stability Review | ||||

| 14:00 | CAD | BoC Rate Decision | 1.75% | 1.75% |

{kind=link}