Dollar weakens broadly today as markets are turning their focuses to manufacturing from the US. Final reading of Markit PMI shouldn’t deviate much from the first print 50.6. Meanwhile, ISM manufacturing could probably how confidence turned after last round of trade war escalation with China. Even if the greenback might survive ISM manufacturing, more challenges lie ahead with ISM services and non-farm payrolls.

Trump sounded calm and affirmative with is morning tweet today. He noted “no visible increase in costs or inflation” from the tariffs as “China is subsidizing its product”. Meanwhile, “US is taking Billions!” It’s doesn’t really matter much how true Trump’s claims are, much like China’s denial of its own faults. The point is, Trump also preparing his base for a prolonged trade war with China.

In the currency markets, New Zealand and Australian Dollars are currently the strongest ones for today. After initial selloff, major European stock indices quickly reversed and are all trading mildly up currently. Though German 10-year yield remains weak after hitting new record low at -0.217 earlier today. And that keeps Swiss Franc as third strongest, after EUR/CHF dives to new 2-year low. Meanwhile, Yen is the weakest one so far, mainly because it turned into consolidations on overbought conditions. Sterling is second weakest after manufacturing data showed reversal of pre-Brexit stockpiling effects.

Technically, EUR/CHF’s strong break of 1.1162 key support carries some long term bearish implications. And it’s probably setting up for an extended down trend. While Dollar is weak, it should be noted that EUR/USD and AUD/USD are seen as staying in near term consolidations only. There is no bearish reversal in the greenback yet.

In Europe, currently, FTSE is up 0.11%. DAX is up 0.01%. CAC is up 0.12%. German 10-year yield is down -0.007 at -0.207. Earlier in Asia, Nikkei dropped -0.92%. Hong Kong HSI dropped -0.03%. China Shanghai SSE dropped -0.30%. Singapore Strait Times rose 0.18%. Japan 10-year JGB yield rose 0.0053 to -0.091.

UK PMI manufacturing dropped to 49.4, first contraction July 2016

UK PMI manufacturing dropped to 49.4 in May, down from 53.1 and missed expectation of 52.2. That’s also the lowest level in 34 months. Markit noted that manufacturers reported increased difficulties in convincing clients to commit to new contracts during May, due to high level of inventories from pre-Brexit stockpiling. New order inflows also deteriorated from both domestic and overseas sources.

Rob Dobson, Director at IHS Markit, said: “The trend in output weakened and, based on its relationship with official ONS data, is pointing to a renewed downturn of production… New order inflows declined from both domestic and overseas markets, as already high stock levels at manufacturers and their clients led to difficulties in sustaining output levels and getting agreement on new contracts. Demand was also impacted by ongoing global trade tensions, as well as by companies starting to unwind inventories built up in advance of the original Brexit date. Some EU-based clients were also reported to have shifted supply chains away from the UK.”

Both Johnson and Hunt prepared for no-deal Brexit

As the race for UK Prime Minister position continues, former Foreign Minister Boris Johnson pledged to leave EU on time on October 31, with or without a deal. He said “If I get in we’ll come out, deal or no deal, on October the 31st.” On other policies he said “Now is the time to unite our society, and unite our country. To build the infrastructure, to invest in education, to improve our environment, and to support our fantastic NHS (National Health Service) … To lift everyone in our country, and of course, also to make sure that we support our wealth creators and the businesses that make that investment possible.”

Current Foreign Minister Jeremy Hunt also said he’s prepared for no-deal Brexit in there was no alternative. He told BBC Radio “In the end, if the only way to leave the European Union, to deliver on the result of the referendum, was to leave without a deal, then I would do that… But I would do so very much as a last resort, with a heavy heart because of the risks to businesses and the risks to the union.”

Eurozone PMI manufacturing finalized at 47.7, toughest spell since 2013 continued

Eurozone PMI Manufacturing was finalized at 47.7 in May, unrevised, down from April’s 47.9. That’s also very close to six year low at 47.5 made in March. Looking at the member states, German PMI manufacturing was worst at 44.3. Austria reading dropped to 50-month low at 49.5. Italy reading improved to 8-month high at 49.5 but stayed below 50. Spain reading dropped to 3-month low at 50.2. France reading improved to 3-month high at 50.6, barely expanding.

Chris Williamson, Chief Business Economist at IHS Markit said: “A fourth successive monthly drop in output and further steep decline in new orders underscored how the sector remains in its toughest spell since 2013… trade wars, slumping demand in the auto sector, Brexit and wider geopolitical uncertainty all remained commonly cited risks to the outlook, and all have the potential to derail any stabilisation of the manufacturing sector.”

Also released, Swiss CPI slowed to 0.6% yoy in May, down from 0.7% yoy and matched expectation. Swiss PMI manufacturing rose 0.2 to 48.6 in May, below expectation of 48.8.

China Caixin PMI manufacturing unchanged at 50.2, some resilience with weakened confidence

China Caixin manufacturing PMI was unchanged at 50.2 in May, above expectation of 50.0. Production was broadly stable in May. Total new work and export sales both increase slightly. And, there was renewed rise in purchasing activity.

Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group said:”Overall, China’s economy showed steady growth and resilience in May. The manufacturing sector saw demand rise from both overseas and domestic markets, and prices were stable. However, business confidence weakened, and manufacturers’ inventory levels remained low. The trade tensions between the U.S. and China are having an impact on confidence and the best way to respond to this is to boost the confidence of enterprises, residents and capital markets by carrying out favorable reforms and to undertake timely adjustments to regulations and controls.”

Japan PMI manufacturing finalized at 49.8, potential banana skins lie ahead

Japan PMI manufacturing was finalized at 49.8 in May, revised up from 49.6, down from 50.2 in April. Markit noted that domestic and external demand conditions deteriorate. Firms slow the rate of hiring amid production cutbacks. And, output expectations turn negative for first time since November 2012.

Joe Hayes, Economist at IHS Markit: “There were no signs a let-up in the recent manufacturing downturn during May, as output and new orders both slipped for fifth successive months. Weak demand from Japan’s key trade partner, China, as well as signs of an increasingly sluggish domestic economy, have impacted sales volumes…. Given the importance of capital goods to Japan’s foreign trade, it would suggest further difficulties lie ahead for Japanese exporters.

“With the upcoming sales tax hike and upper house elections in July, there lies ahead potential banana skins for Japanese firms to avoid. Re-escalated trade tensions between China and the US merely add to existing concerns for manufacturers. Subsequently, businesses cast a downbeat assessment for the year ahead for the first time in six-and-a-half years.”

Also from Japan, capital spending rose 6.1% in Q1, beat expectation of 2.6%.

Australia AiG PMI dropped to -2.1, wage index at lowest since Mar 2017

Australia AiG Performance of Manufacturing Index dropped -2.1 pts to 52.7 in May, suggesting a slower rate of growth. Looking at the details, production dropped sharply by -6.9 to 51.2. New orders dropped -3.3 to 52.3. exports dropped -3.6 to just 40.3. Employment index staged a strong rebound and rose 4.1 to 55.6. But average wages dropped -2.2 to 55.5. Input prices rose 3.6 to 68.3 but selling prices dropped -2.8 to 52.1.

In particular, on wages, 55.5 is the lowest monthly results since March 2017 and is well below historical average of 59.2. This index has been trending lower since its recent peak in September 2018. It indicates that fewer manufacturing businesses are now implementing wage rises, compared to the recent peak in Q3 of 2018.

Also from Australia, TD Securities inflation rose 0.0% mom in May. Company operating profit rose 1.7% qoq in Q1.

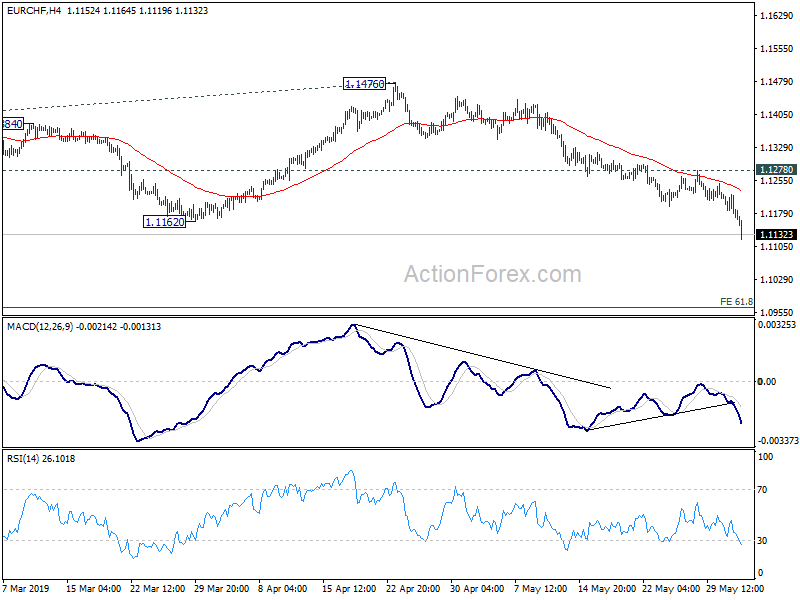

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1159; (P) 1.1192; (R1) 1.1242; More….

EUR/CHF drops sharply to as low as 1.1119 so far today after breaking 1.1162 support firmly. Current development confirms resumption of whole decline from 1.2004. Intraday bias is now on the downside for 61.8% projection of 1.2004 to 1.1173 from 1.1476 at 1.0962 next. On the upside, break of 1.1278 resistance is needed to confirm short term bottoming. Otherwise, outlook will stays bearish in case of recovery.

In the bigger picture, focus will stay on 61.8% retracement of 1.0629 to 1.2004 at 1.1154. Sustained break of 1.1154 will argue that fall from 1.2004 is itself a long term down trend. Next target will be 1.0629 support next. This will now remain the favored case as long as 1.1476 resistance holds even in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Manufacturing Index May | 52.7 | 54.8 | ||

| 23:50 | JPY | Capital Spending Q1 | 6.10% | 2.60% | 5.70% | |

| 0:30 | JPY | PMI Manufacturing May F | 49.8 | 49.7 | 49.6 | |

| 1:00 | AUD | TD Securities Inflation M/M May | 0.00% | 0.20% | ||

| 1:30 | AUD | Company Operating Profit Q/Q Q1 | 1.70% | 2.80% | 0.80% | 2.80% |

| 1:45 | CNY | Caixin PMI Manufacturing May | 50.2 | 50 | 50.2 | |

| 6:30 | CHF | CPI M/M May | 0.30% | 0.30% | 0.20% | |

| 6:30 | CHF | CPI Y/Y May | 0.60% | 0.60% | 0.70% | |

| 7:30 | CHF | PMI Manufacturing May | 48.6 | 48.8 | 48.5 | |

| 7:45 | EUR | Italy Manufacturing PMI May | 49.7 | 48.5 | 49.1 | |

| 7:50 | EUR | France Manufacturing PMI May F | 50.6 | 50.6 | 50.6 | |

| 7:55 | EUR | Germany Manufacturing PMI May F | 44.3 | 44.3 | 44.3 | |

| 8:00 | EUR | Eurozone Manufacturing PMI May F | 47.7 | 47.7 | 47.7 | |

| 8:30 | GBP | PMI Manufacturing May | 49.4 | 52.2 | 53.1 | |

| 13:30 | CAD | Manufacturing PMI May | 49.7 | |||

| 13:45 | USD | Manufacturing PMI May F | 50.6 | 50.6 | ||

| 14:00 | USD | ISM Manufacturing May | 53 | 52.8 | ||

| 14:00 | USD | ISM Prices Paid May | 51 | 50 | ||

| 14:00 | USD | ISM Employment May | 52.4 | |||

| 14:00 | USD | Construction Spending M/M Apr | 0.40% | -0.90% |

{kind=link}