While Dollar remains the worst performing one for the week, Euro is overtaking as the weakest one for today. Selloff in crosses, in particular in EUR/CHF, is dragging down the common currency. Much stronger than expected industrial production data was ignored. Instead, it’s clear that ECB is on track for more monetary stimulus, and could probably deliver even ahead of Fed.

Staying in the currency markets, Dollar is so far the weakest one for today, followed by New Zealand Dollar. Swiss Franc and Yen are the strongest ones, also ignoring resilience in stock markets and rebound in treasury yields. Canadian Dollar is the third strongest for now.

In Europe, currently, FTSE is up 0.10%. DAX is up 0.07%. CAC is up 0.44%. German 10-year yield is up 0.061 at -0.203, it hit record low at -0.407 just earlier this month. Earlier in Asia, Nikkei rose 0.20%. Hong Kong HSI rose 0.14%. China Shanghai SSE rose 0.44%. Singapore Strait Times rose 0.21%. Japan 10-year JGB yield rose 0.0259 to -0.114.

WH Navarro: Trade negotiation with China in a quiet period, be patient and don’t listen to garbage

White House trade advisor Peter Navarro said trade negotiation with China is “in a quiet period” and urged people to be “patient with the process”. He also trashed media in US and China as they reported “garbage” regarding trade negotiation. Instead he urged people to only listen to comments from either Trump or Trade Representative Robert Lighthizer.

Navarro said on CNBC Squawk Box that “my advice for investors is to be patient with the process and don’t believe anything you read in either the Chinese or the US press about these negotiations unless it comes from the mouth of either the president or advisor Lighthizer”.

And, “there’s just going to be a lot of garbage coming out of the Wall Street Journal and the People’s Daily and everything in between,” he added, “there were all sorts of stories written and they were designed to shape the negotiations and they didn’t have any insight into them.”

US PPI rose 0.1%, 1.7% yoy in June, versus expectation of 0.1% mom, 1.6% yoy. PPI core rose 0.3% mom, 2.3% yoy, versus expectation of 0.2% mom, 2.1% yoy.

ECB Visco: Will asset hot to adjust policy instruments in the coming weeks

ECB Governing Council member Ignazio Visco said the central bank “will need to adopt further expansionary measures if the euro zone economy does not pick up.” And, “in the coming weeks the ECB will continue to assess how to adjust the instruments at its disposal”. This is in-line with market expectations that ECB is ready ramp up monetary stimulus either on July 25 or later in September.

Being Governor of Bank of Italy too, Visco expected the Italian economy to grow just 0.1% this year, marginally below the government’s 0.2% official forecast. Though, he also expected growth to pickup to just slightly below 1% in 2020 and 2021. He urged the government to adopt “prudent” budget deficit targets for the coming years. But he also welcomed recent fall in Italian yields, after EU averted the Excessive Deficit Procedure on the country.

Eurozone industrial production rose 0.9% mom in May, above expectation

Eurozone industrial production rose 0.9% mom in May, well above expectation of 0.2% mom. Comparing by industrial grouping, production of non-durable consumer goods rose by 2.7%, durable consumer goods by 2.3%, capital goods by 1.3% and energy by 0.7%, while production of intermediate goods fell by 0.2%.

EU 28 industrial production rose 0.8% mom. Among member states for which data are available, the highest increases in industrial production were registered in Denmark (+4.4%), Ireland (+2.3%) and France (+2.1%). The largest decreases were observed in Finland (-2.9%), Romania (-1.9%) and Croatia (-1.7%).

China trade surplus widened to USD 51B, both imports and exports declined

In June, in USD terms, US imports dropped -7.3% yoy to USD 16.19B. Exports dropped -1.3% yoy to 21.28B. Both import and exports were worse than expectation of -4.6% yoy and -0.6% yoy respectively. Trade surplus came in at USD 51.0B above expectation of USD 45.2B.

The results clearly showed some impacts in trade after US imposition on higher tariffs on USD 200B of Chinese goods came into effect. But so far, there was no notably improvement in US-China trade balance. US trade deficit with China came in at USD -140.5B in the first half, worse than USD -133.8B in first half of 2018.

From Jan to Jun, with US: Total trade dropped -14.2% yoy to USD 258.3B. Exports dropped -8.1% yoy to USD 199.4B. Imports dropped -29.9% yoy to USD 58.9B. Trade surplus was at USD 140.5B.

From Jan to Jun, with EU: Total trade rose 4.9% yoy to USD 338.0B. Exports rose 6.0% yoy to USD 202.8B. Imports rose 3.3% yoy to 135.2B. Trade surplus was at USD 67.6B

From Jan to Jun, with AU: Total trade rose 6.3% yoy to 78.7B. Exports rose 2.0% to USD 22.1B. Imports rose 8.1% to USD 56.7B. Trade deficit was at USD -34.6B.

New Zealand BusinessNZ PMI rose to 51.3, but employment worsened

New Zealand BusinessNZ Performance of Manufacturing Index rose to 51.3 in June, up from 50.4. BusinessNZ’s executive director for manufacturing Catherine Beard said that while the sector avoided further deterioration in activity from May, there were still a number of concerns about manufacturing’s current state of play.

She said: “The key sub-indexes of production (51.0) and new orders (52.8) recovered from May, which ensured the sector didn’t fall into contraction for June. However, employment (48.0) worsened to its lowest level since August 2016, while deliveries of raw materials (48.9) also fell into negative territory for the first time since December 2017, and its lowest result since September 2012.

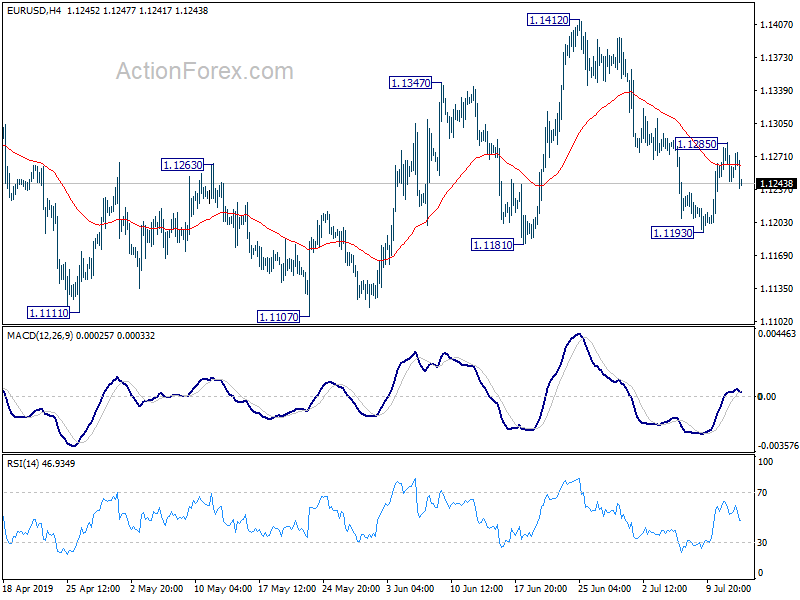

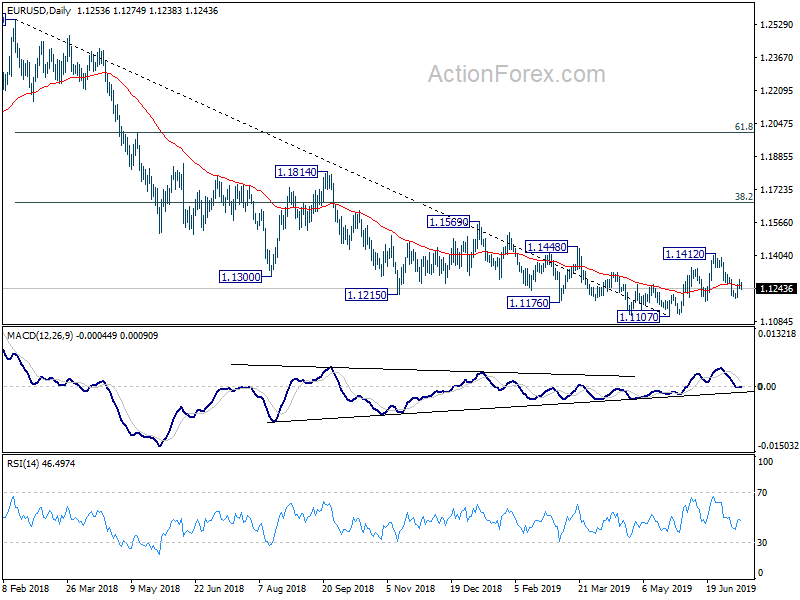

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1238; (P) 1.1262; (R1) 1.1279; More…

Intraday bias in EUR/USD is turned neutral with 4 hour MACD crossed below signal line. A temporary top is formed at 1.1285. On the upside, above 1.1285 will extend the rebound from 1.1193 to 1.1412 resistance. Break will resume the whole choppy rise from 1.1107. On the downside, break of 1.1193 will turn bias back to the downside to retest 1.1107 low instead.

In the bigger picture, bullish convergence condition in daily and weekly MACD suggests that 1.1107 is a medium term bottom. However, rejection by 55 EMA retains medium term bearish. Outlook will be neutral for now. On the downside, break of 1.1107 will resume the down trend from 1.2555 (2018 high) to 78.6% retracement of 1.0339 to 1.2555 at 1.0813. Meanwhile, break of 1.1412 will resume the rebound to 38.2% retracement of 1.2555 to 1.1107 at 1.1660.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | BusinessNZ Manufacturing PMI Jun | 51.3 | 50.2 | 50.4 | |

| 04:30 | JPY | Industrial Production M/M May F | 2.20% | 2.30% | 2.30% | |

| 07:00 | CNY | Trade Balance (CNY) Jun | 345B | 276B | 276B | |

| 07:00 | CNY | Imports Y/Y (CNY) Jun | -0.40% | 4.50% | -2.50% | |

| 07:00 | CNY | Exports Y/Y (CNY) Jun | 6.10% | 7.70% | 7.70% | |

| 07:00 | CNY | Trade Balance (USD) Jun | 51.0B | 45.2B | 41.7B | |

| 07:00 | CNY | Imports Y/Y (USD) Jun | -7.30% | -4.60% | -8.50% | |

| 07:00 | CNY | Exports Y/Y (USD) Jun | -1.30% | -0.60% | 1.10% | |

| 09:00 | EUR | Eurozone Industrial Production M/M May | 0.90% | 0.20% | -0.50% | -0.40% |

| 12:30 | USD | PPI M/M Jun | 0.10% | 0.10% | 0.10% | |

| 12:30 | USD | PPI Y/Y Jun | 1.70% | 1.60% | 1.80% | |

| 12:30 | USD | PPI Core M/M Jun | 0.30% | 0.20% | 0.20% | |

| 12:30 | USD | PPI Core Y/Y Jun | 2.30% | 2.10% | 2.30% |

{kind=link}