Euro drops broadly today as pressured by renewed selling following weaker than expected German inflation data. That’s more than enough o offset improved unemployment rate. For now, though, Swiss Franc is the weakest one, followed by New Zealand Dollar. On the other hand, Dollar surges broadly, with the help from the decline in EUR/USD. Sterling is steadily firmer as it’s staying in consolidations.

Technically, EUR/USD’s medium term down trend resumes through 1.09 and it’s heading towards 1.0813 fibonacci level next. EUR/JPY is pressing 117.55 again. Break will bring retest of 115.86 low. USD/CHF is heading back to 0.9983 resistance. Break will be a solid sign of near term bullishness and should pave the way to 1.0237 resistance.

In Europe, currently, FTSE is down -0.05%. DAX is up 0.10%. CAC is up 0.21%. German 10-year yield is up 0.006 at -0.564. Earlier in Asia, Nikkei dropped -0.56%. Hong Kong HSI rose 0.53%. China Shanghai SSE dropped -0.92%. Singapore Strait Times dropped -0.18%. Japan 10-year JGB yield rose 0.0126 to -0.221.

German retail sales rose 0.5%, CPI dropped to 1.2%

German retail sales rose 0.5% mom in August, below expectation of 0.6% mom. Over the year, retail sales rose 3.2% yoy. Unemployment dropped -10k in September versus expectation of 5k. Unemployment rate was unchanged at 5.0% in September, matched expectations. CPI slowed to 1.2% yoy in September, down from 1.4% yoy, missed expectation of 1.4% yoy.

Eurozone unemployment rate dropped to 7.4%, lowest since 2008

Eurozone unemployment rate dropped to 7.4% in August, down from 7.5% and beat expectation of 7.5%. That’s also the lowest level since May 2008, and an extension of the sustained down trend from 11.5% since August 2014. EU28 unemployment rate also dropped to 6.2%, down from 6.3%. Among the Member States, the lowest unemployment rates in August 2019 were recorded in Czechia (2.0%) and Germany (3.1%). The highest unemployment rates were observed in Greece (17.0% in June 2019) and Spain (13.8%).

UK Q2 GDP finalized as -0.2% qoq, services the only positive contribution

UK GDP contraction was finalized -0.2% qoq in Q2, matched expectations, revised. Over the year, GDP grew 1.3% yoy, down from 2.1% yoy in Q1. In the quarter, services rose 0.12%, the only positive contribution to growth, but that was the weakest quarterly figure in three years. production contracted -0.24%. Construction dropped -0.07%. Agriculture was flat.

Also from UK, mortgage approvals dropped to 66k in August, below expectation of 67k. M4 rose 0.4% mom in August, matched expectations. Current account deficit narrowed to GBP -25.2B in Q2, larger than expectation of GBP -19.2B.

Swiss KOF dropped to 93.2, outlook remains gloomy towards end of the year

Swiss KOF Economic Barometer dropped to 93.2 in September, down from 95.5, missed expectation of 94.5. KOF said “downward tendency that has been evident since the beginning of the year is now continuing”. Swiss economic outlook “remains gloomy towards the end of 2019.”

It added that the decline is primarily due to declining developments in the manufacturing industry. The indicator bundle for the service industry and the accommodation and food service industry slightly reinforce this decline. By contrast, private consumption, foreign demand and the construction industry remain stable relative to the previous month.

China manufacturing PMIs improved, but trade uncertainties still weigh

China Caixin Manufacturing PMI improved to 51.4 in September, up from 50.4 and beat expectation of 50.2. That’s also the highest reading since February 2018, signalling a recovery in the sector. Markit noted there were stronger increases in output and total new orders. However, new export business continued to decline. Staffing levels remained broadly unchanged.

Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group said: “The recovery in China’s manufacturing industry in September benefited mainly from the potential growth of domestic demand. The trade conflicts between China and the U.S. had a notable impact on exports, production costs and confidence of enterprises. Compared with growth in new orders, the employment situation recovered only a bit, indicating that structural issues may exist in the labor market. Central policymakers have recently been emphasizing the strong growth in the domestic market. Faster construction of infrastructure projects, better implementation of upgrading the industrial sector, and tax and fee cuts are likely to offset the influence of the subdued overseas demand and soften the downward pressure on China’s economic growth.”

Also released, the NBS PMI Manufacturing rose to 49.8 in September, up from 49.5 and beat expectation of 49.7. While there was and improvement, the sector remained in contraction for the fifth straight months. Total new orders improved and swung back to growth, indicating improving domestic demand. But new export orders dropped for the 16th month. Meanwhile factories continued to cut jobs with employment sub-index largely unchanged at 47.0.

BoJ: Not reached an impasse on monetary policy measures

Summary of opinions at September 18-19 BoJ meeting, BoJ warned that the “contrast between the manufacturing and nonmanufacturing sectors has become more evident” at home and abroad. Downside risks to the global economy “have been increasing further” mainly in Europe due to Brexit.

Also, ” it is becoming necessary to pay closer attention to the possibility that the inflation momentum will be lost”. BoJ needs to “reexamine economic and price developments” at the next monetary policy meeting (MPM).

It is also important for BoJ to “communicate with an emphasis that it has not reached an impasse on monetary policy measures”. Additionally, with regard to a negative interest policy, “its impact on the overall economy should be considered first, rather than on banks’ business conditions.”

Also released, industrial production dropped -1.2% mom in August, below expectation of -0.5% mom. Retail sales rose 2.0% yoy in August, above expectation of 0.9% yoy. Weak production data reconfirm that impact from global slowdown on exports. Strength of retail sales might partly be due to pre sales tax hike effect and could wane ahead.

New Zealand business confidence dropped -53.5, no impact from RBNZ’s rate cut

New Zealand ANZ Business Confidence dropped to -53.5 in September, down from -52.3. That’s also the worst reading since April 2008. Agriculture scored weakest confidence at -75.6 while manufacturing was best at -46.2. Activity outlook also dropped to -1.8, down from -0.5. Activity outlook was worst in construction at -7.1, best at services at -0.6.

ANZ noted that RBNZ will be “disappointed that its unexpectedly large 50bp cut in the Official Cash Rate last month does not appear to have had much impact on business’ sentiment or investment and employment intentions.” And, “prolonged lack of confidence is starting to feed its way through the economy and is threatening the tight labour market.” Also, “this gradual but prolonged economic slowdown is at risk of ceasing to be about the data and starting to become about the people.

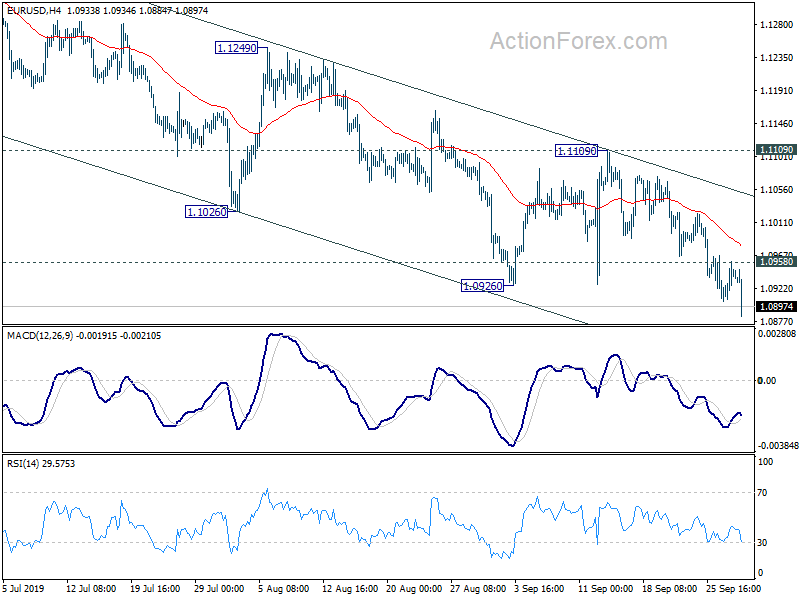

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0912; (P) 1.0935; (R1) 1.0966; More…

EUR/USD’s decline resumes after brief consolidation and reaches as low as 1.0084 so far. Intraday bias is back on the downside. Current down trend should target 1.0813 fibonacci level next. On the upside, break of 1.0958 minor resistance will turn intraday bias neutral again. But outlook will remain bearish as long as 1.1109 resistance holds.

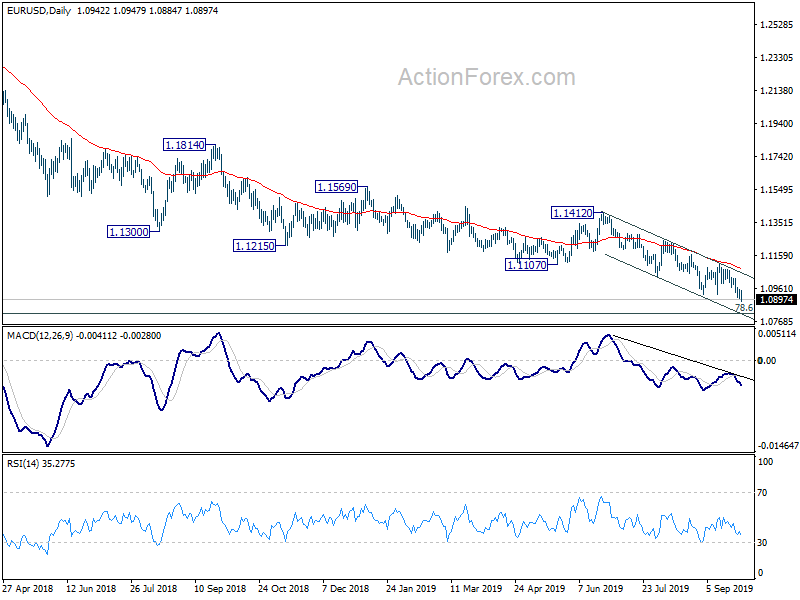

In the bigger picture, down trend from 1.2555 (2018 high) is in progress. Prior rejection of 55 week EMA also maintained bearishness. Further fall should be seen to 78.6% retracement of 1.0339 to 1.2555 at 1.0813. Decisive break there will target 1.0339 (2017 low). On the upside, break of 1.1412 resistance is needed to confirm medium term bottoming. Otherwise, outlook will stay bearish in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Aug | 0.80% | -2.70% | -1.30% | |

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 23:50 | JPY | Industrial Production M/M Aug P | -1.20% | -0.50% | 1.30% | |

| 23:50 | JPY | Retail Trade Y/Y Aug | 2.00% | 0.90% | -2.00% | |

| 00:00 | NZD | ANZ Business Confidence Sep | -53.5 | -58.5 | -52.3 | |

| 01:00 | CNY | Manufacturing PMI Sep | 49.8 | 49.7 | 49.5 | |

| 01:00 | CNY | Non-Manufacturing PMI Sep | 53.7 | 54.2 | 53.8 | |

| 01:30 | AUD | Private Sector Credit M/M Aug | 0.20% | 0.30% | 0.20% | |

| 01:45 | CNY | Caixin Manufacturing PMI Sep | 51.4 | 50.2 | 50.4 | |

| 05:00 | JPY | Housing Starts Y/Y Aug | -7.10% | -6.10% | -4.10% | |

| 06:00 | EUR | Germany Retail Sales M/M Aug | 0.50% | 0.60% | -2.20% | -0.80% |

| 07:00 | CHF | KOF Leading Indicator Sep | 93.2 | 94.5 | 97 | 95.5 |

| 07:55 | EUR | Germany Unemployment Change Sep | -10K | 4K | 4K | 2K |

| 07:55 | EUR | Germany Unemployment Rate Sep | 5% | 5% | 5% | |

| 08:30 | GBP | Net Lending to Individuals (GBP) M/M Aug | 4.8B | 5.1B | 5.5B | |

| 08:30 | GBP | GDP Q/Q Q2 F | -0.20% | -0.20% | -0.20% | |

| 08:30 | GBP | Mortgage Approvals Aug | 66K | 67K | 67K | |

| 08:30 | GBP | M4 Money Supply M/M Aug | 0.40% | 0.40% | 0.70% | |

| 08:30 | GBP | M4 Money Supply Y/Y Aug | 3.20% | 2.70% | ||

| 08:30 | GBP | Current Account (GBP) Q2 | -25.2B | -19.2B | -30.0B | -33.1B |

| 09:00 | EUR | Unemployment Rate Aug | 7.40% | 7.50% | 7.50% | |

| 12:00 | EUR | Germany CPI M/M Sep P | 0.00% | 0.10% | -0.20% | |

| 12:00 | EUR | Germany CPI Y/Y Sep P | 1.20% | 1.40% | 1.40% | |

| 12:30 | CAD | Industrial Product Price M/M Aug | 0.20% | -0.20% | -0.30% | |

| 12:30 | CAD | Raw Material Price Index Aug | -1.80% | 1.30% | 1.20% | 1.30% |

| 13:45 | USD | Chicago PMI Sep | 50.5 | 50.4 |

{kind=link}