Sterling’s pull back extends deeper today on renewed Brexit concern. Setting a hard deadline of December 2020 for trade negotiations UK and EU could create another Brexit cliff-edge. Meanwhile, Australian and New Zealand Dollars follow the Pound as next weakest, partly weighed down by risk aversion. On the other hand, Swiss Franc and Euro are currently the strongest, helped by rebound in respective Sterling crosses. Dollar is mixed for the moment, together with Yen.

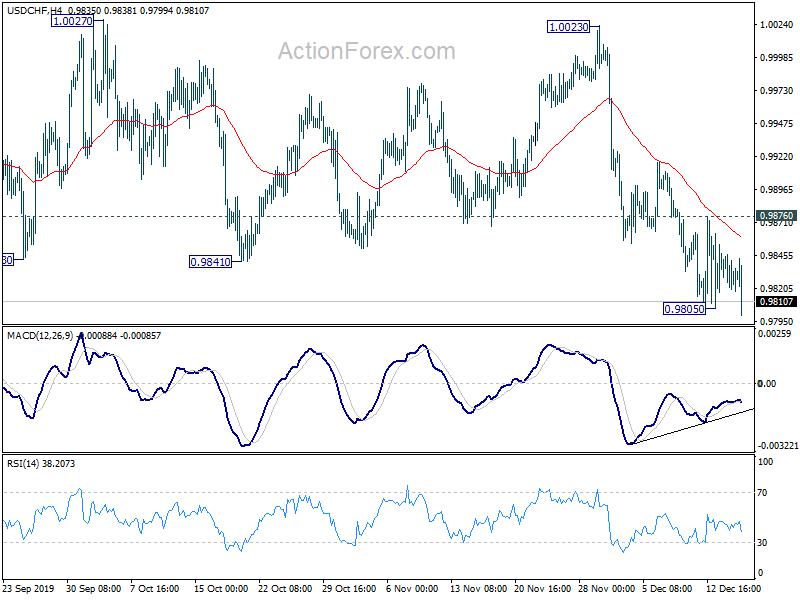

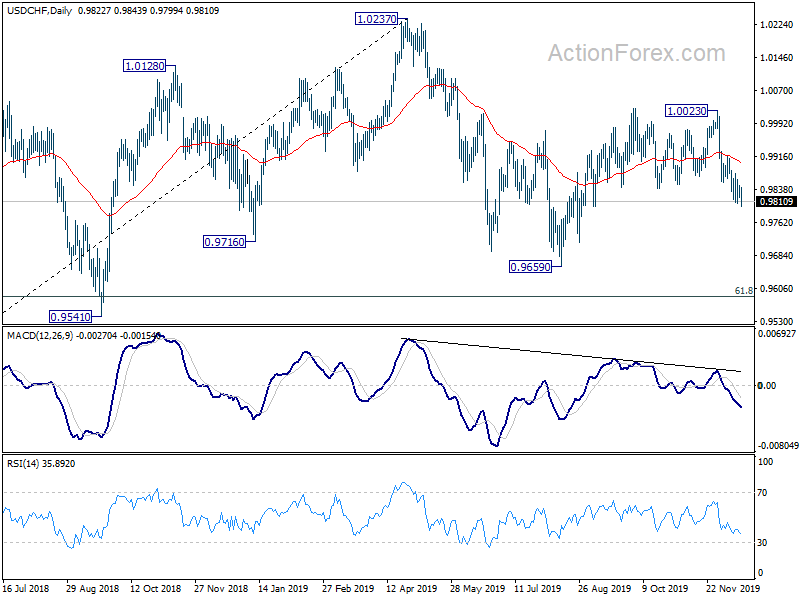

Technically, while the pull back in Pound is deep, key near term levels are intact for now. Those are, 1.3050 support in GBP/USD, 142.47 support in GBP/JPY and 0.8508 resistance in EUR/GBP. We’d still expect these levels to hold to bring another rise in Sterling sooner or later. Though, EUR/GBP is looking most vulnerable for now. USD/CHF breaches 0.9805 temporary low and could be resuming fall from 1.0023.

In Europe, currently, FTSE is down -0.06%. DAX is down -0.67%. CAC is down -0.25%. German 10-year yield is down -0.012 at -0.283. Earlier in Asia, Nikkei rose 0.47%. Hong Kong HSI rose 1.22%. China Shanghai SSE rose 1.27%. Singapore Strait Times dropped -0.16%. Japan 10-year JGB yield rose 0.0142 to -0.013.

US building permits rose to 1.482m, housing starts to 1.365m

US building permits rose 1.4% mom to adjusted annual rate of 1.482 m in November, above expectation of 1.410m. Housing starts rose 3.2% to 1.365m, above expectation of 1.340m. Canada manufacturing sales dropped -0.7% mom in October, below expectation of 0.0% mom.

EU Weyand: Failing to reach a trade agreement with UK by 2020 would lead to another cliff-edge situation

EU trade director-general Sabine Weyand acknowledged that “UK does not intend to go for an extension of the transition” and EU needs to be prepared for that. She added, “that means in the negotiations we have to look at those issues where failing to reach an agreement by 2020 would lead to another cliff-edge situation.”

Weyand also said EU is ready to start negotiations very quickly after UK leaves EU at the end of January. European Commission is due today afternoon to brief EU27 countries on its work program for the negotiations.

UK unemployment rate unchanged at 3.8%, wages growth slowed

UK unemployment rate was unchanged at 3.8% in the three months to October, below expectation of 3.9%. Estimated unemployment rate was 4.0% for men and 3.5% for women, the latter at a record low. An estimated 1.28m people were unemployment, 93k fewer than a year ago.

Wages growth slowed quite notably. Average earnings including bonus dropped to 3.2% 3moy, down from 3.7% and missed expectation of 3.4%. Average earnings excluding bonus dropped to 3.5% 3moy, down from 3.6%, but beat expectation of 3.4%.

ECB Kazimir: No significant growth before completing monetary union

ECB Governing Council member Peter Kazimir urged further structural change in the bloc. He warned, “I am worried that we won’t be able to enjoy significant economic growth before we deal with the fact that EU is lagging behind in technology and before we complete the European Monetary Union.”

Another Governing Council member Madis Müller said the upcoming policy review should consider whether the control over inflation has diminished. And, “maybe in this case we would not need to be as aggressive with our policies. We could be more flexible and not chase that goal at any price.”

RBA minutes suggest more easing on weak wages growth

Minutes of December RBA meeting suggest that the central bank is still on track to further easing next year, probably in February. Employment and wages growth would remain the main reason for doing so. It’s noted that “current rate of wages growth was not consistent with inflation being sustainably within the target range”. Also, “nor was it consistent with consumption growth returning to trend”. Furthermore, private sector wages growth has indeed “levelled out in recent quarters, following its gentle upward trend of the previous couple of years”.”

RBA members also discussed the effect of lower interest rates on confidence, including business and consumer. However, “while members recognised the negative confidence effects for some parts of the community arising from lower interest rates, they judged that the impact of these effects was unlikely to outweigh the stimulus to the economy from lower interest rates.”

Suggested readings on RBA minutes:

- RBA Hinted Further Easing in 1Q20

- RBA Minutes Highlight Importance of February Meeting

- RBA Headed For A Cut In Feb 2020?

New Zealand ANZ business confidence rose to -13.2, commodity prices and low interest rates working their magic

New Zealand ANZ Business Confidence improved to -13.2 in December, up from -26.4. It’s the best reading since October 2017. Nevertheless, confidence remained negative across all sectors, worst in agriculture (-35.1) and beat in retail (-6.5). Activity outlook also improved to 17.2, up from 12.9, best in manufacturing (23.7), worst in construction (9.5). Outlook reading was the best since April 2018.

ANZ said: “New Zealand businesses are rolling into the end of the year in much better heart than was looking likely just a few months ago, particularly manufacturers. Challenges remain, and time will tell how sustainable the lift in sentiment and activity proves to be, with headwinds for the economy still present and global risks not having gone away, for all that some geopolitical risks are now less prominent. But for now, surprisingly strong commodity prices and low interest rates are working their magic, and 2019 is ending on a much better note than it began.”

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9815; (P) 0.9831; (R1) 0.9842; More…

USD/CHF’s breach of 0.9805 temporary low suggests resumption of fall from 1.0023. Intraday bias is turned back to the downside for retesting 0.9659 low. However, considering bullish convergence condition in 4 hour MACD, break of 0.9876 will indicate short term bottoming. In such case, intraday bias will be turned back to the upside for 55 day EMA (now at 0.9900) and above.

In the bigger picture, medium term outlook remains neutral as USD/CHF is staying in range of 0.9659/1.0237. In any case, decisive break of 1.0237 is needed to indicate up trend resumption. Otherwise, more sideway trading would be seen with risk of another fall. Meanwhile, break of 0.9695 support will target 0.9541 support instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 20:00 | NZD | Westpac Consumer Survey Q4 | 109.9 | 103.1 | ||

| 00:00 | NZD | ANZ Business Confidence Dec | -13.2 | -26.4 | ||

| 00:30 | AUD | Home Loans Oct | 0.60% | 1.40% | -3.00% | |

| 00:30 | AUD | RBA Meeting Minutes | ||||

| 09:30 | GBP | Claimant Count Change Nov | 28.8K | 20.2K | 33.0K | 26.4K |

| 09:30 | GBP | Claimant Count Rate Nov | 3.50% | 3.40% | ||

| 09:30 | GBP | ILO Unemployment Rate (3M) Oct | 3.80% | 3.90% | 3.80% | |

| 09:30 | GBP | Average Earnings Including Bonus 3M/Y Oct | 3.20% | 3.40% | 3.60% | 3.70% |

| 09:30 | GBP | Average Earnings Excluding Bonus 3M/Y Oct | 3.50% | 3.40% | 3.60% | |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Oct | 24.5B | 18.7B | 18.3B | 18.7B |

| 11:00 | GBP | CBI Industrial Order Expectations Dec | -28 | -25 | -26 | |

| 13:30 | USD | Housing Starts Nov | 1.365M | 1.340M | 1.314M | 1.323M |

| 13:30 | USD | Building Permits Nov | 1.482M | 1.410M | 1.461M | |

| 13:30 | CAD | Manufacturing Shipments M/M Oct | -0.70% | 0.00% | -0.20% | |

| 14:15 | USD | Industrial Production M/M Nov | 0.80% | -0.80% | ||

| 14:15 | USD | Capacity Utilization Nov | 77.20% | 76.70% |

{kind=link}