Sterling is sold off broadly today as poor GDP data added to the case of BoE rate cut. Recent comments from BoE officials already suggested that they’re open to easing if data don’t show improvement. The Pound will face more tests from CPI and retail sales later in the week. Yen is following as the second weakest as pressured by surging Germany and US yields. Meanwhile, Swiss Franc and Canadian Dollar the stronger ones so far. Dollar is mixed, awaiting US-China trade deal phase one, to be signed on Wednesday.

Technically, GBP/USD extends fall from 1.3284 and should have a test on 1.2905 support. EUR/GBP will also have a take on 0.8591 resistance and break will resume rebound from 0.8276. USD/JPY’s break of 109.72 resistance finally suggests resumption of rise from 104.45. Further rally should be seen to channel resistance (now at 111.53).

In Europe, currently, FTSE is up 0.29%. DAX is down -0.12%. CAC is up 0.07%. German 10-year yield is up 0.060 at -0.176. Earlier in Asia, Japan was on holiday. Hong Kong HSI rose 1.11%. China Shanghai SSE rose 0.75%. Singapore Strait Times dropped -0.15%.

UK GDP dropped -0.3% mom in Nov, weakening services and lackluster manufacturing

UK GDP dropped -0.3% mom in November, well below expectation of 0.0% mom. Services dropped -0.3% mom. Production dropped -1.2% mom, manufacturing dropped -1.7% mom. Construction and agriculture rose 1.9% mom and 0.1% mom respectively.

In the three months to November, GDP grew only 0.1% 3mo3m. Services grew 0.1% 3mo3m, contributing 0.08% to the rolling three months GDP growth. Production contracted -0.6% 3mo3m, contributing -0.08% fall in GDP growth. Construction rose 1.1% 3mo3m, contributing 0.07% to GDP growth.

Head of GDP Rob Kent-Smith said: “Overall, the economy grew slightly in the latest three months, with growth in construction pulled back by weakening services and another lacklustre performance from manufacturing. The UK economy grew slightly more strongly in September and October than was previously estimated, with later data painting a healthier picture. Long term, the economy continues to slow, with growth in the economy compared with the same time last year at its lowest since the spring of 2012. The underlying trade deficit narrowed as exports grew faster than imports.”

Also released from UK, industrial production dropped -1.2% mom, -1.6% yoy in November, below expectation of -0.2% mom, -1.4% yoy. Manufacturing production dropped -1.2% mom, -2.0% yoy, below expectation of -0.2% mom, -1.6% yoy. Goods trade deficit narrowed to GBP -5.3B in November versus expectation of -11.8b.

US Chamber: A sigh of relief with China trade deal

US Chamber of Commerce Executive Vice President Myron Brilliant welcomed the phase one US-China trade deal. He said there is “clearly a sigh of relief from both sides” with the agreement. Also, “implementation of Phase 1 will be important to building trust and certainty, building off the success of the negotiation”.

Nevertheless, he emphasized it’s important that the two sides demonstrate a commitment to moving forward on the Phase 2 negotiations”. “Significant challenges” remain regarding the core structural issues.

China auto sales forecast to contract -2% this year

China Association of Automobile Manufacturers (CAAM) said auto sales dropped -0.1% yoy in December. That’s the 18th straight month of decline. For the whole of 2019, auto sales dropped -8.2%. The association also said sales will drop further by -2% in 2020.

Shi Jianhua, a senior official at CAAM, said: “We have moved away from the high-speed development stage. We have to accept the reality of low-speed development… We had high-speed growth for a consecutive 28 years, which was really not bad, so I hope everyone can calmly look at the market.”

S&P affirms Australia’s AAA rating despite bushfires

S&P Global Ratings said Australia’s AAA sovereign rating is not at immediate risk from the devastating bushfires. Credit analyst Anthony Walker said, “we do not believe that these bushfires will affect credit metrics enough to trigger rating changes in the next one to two years”.

“We believe there is capacity within our current ratings on the sovereign and state governments to absorb the fiscal costs, which are relatively small compared with their budgets,” he noted.

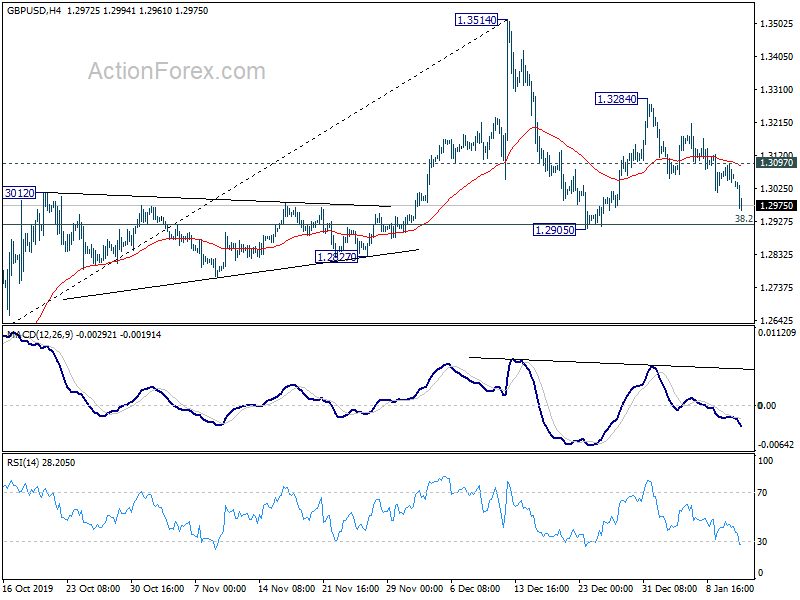

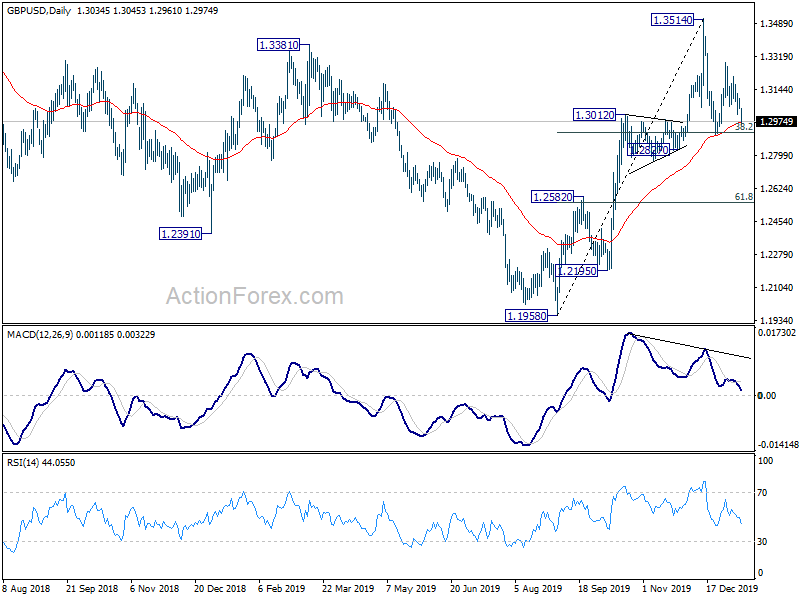

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3011; (P) 1.3068; (R1) 1.3122; More….

GBP/USD’s fall form 1.3284 extends to as low as 1.2961 so far. Intraday bias remains on the downside. Sustained break of 38.2% retracement of 1.1958 to 1.3514 at 1.2920 will target 61.8% retracement at 1.2552. On the upside, above 1.3097 minor resistance will turn bias back to the upside for 1.3284 resistance instead.

In the bigger picture, rise from 1.1958 medium term bottom is expected to extend higher to retest 1.4376 key resistance. Reactions from there would decide whether it’s in consolidation from 1.1946 (2016 low). Or, firm break of 1.4376 will indicate long term bullish reversal. In any case, for now, outlook will stay bullish as long as 1.2582 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:00 | AUD | TD Securities Inflation M/M Dec | 0.30% | 0.00% | ||

| 7:00 | EUR | Germany Wholesale Price Index M/M Dec | 0.00% | 0.20% | -0.10% | |

| 9:00 | EUR | Italy Retail Sales M/M Nov | -0.20% | 0.30% | -0.20% | -0.30% |

| 9:30 | GBP | GDP M/M Nov | -0.30% | 0.00% | 0.00% | |

| 9:30 | GBP | Index of Services 3M/3M Nov | 0.10% | 0.20% | 0.20% | |

| 9:30 | GBP | Industrial Production M/M Nov | -1.20% | -0.20% | 0.10% | |

| 9:30 | GBP | Industrial Production Y/Y Nov | -1.60% | -1.40% | -1.30% | -0.60% |

| 9:30 | GBP | Manufacturing Production M/M Nov | -1.20% | -0.20% | 0.20% | |

| 9:30 | GBP | Manufacturing Production Y/Y Nov | -2.00% | -1.60% | -1.20% | -0.30% |

| 9:30 | GBP | Goods Trade Balance (GBP) Nov | -5.3B | -11.8B | -14.5B | |

| GBP | NIESR GDP Estimate (3M) Dec | 0.00% |

{kind=link}