European majors are generally weaker today. Stronger than expected UK PMIs add to the case for BoE to stand pat next week. But the Pound shrugs off the data. Euro also receive no particular support from PMIs, which signals that the economy failed to pick up momentum for recovery. Dollar and Canadian are currently the strongest ones for today. Over the week, Euro and Canadian are the weakest as both suffered selloffs after respective central bank meetings Sterling is the strongest, followed by Yen.

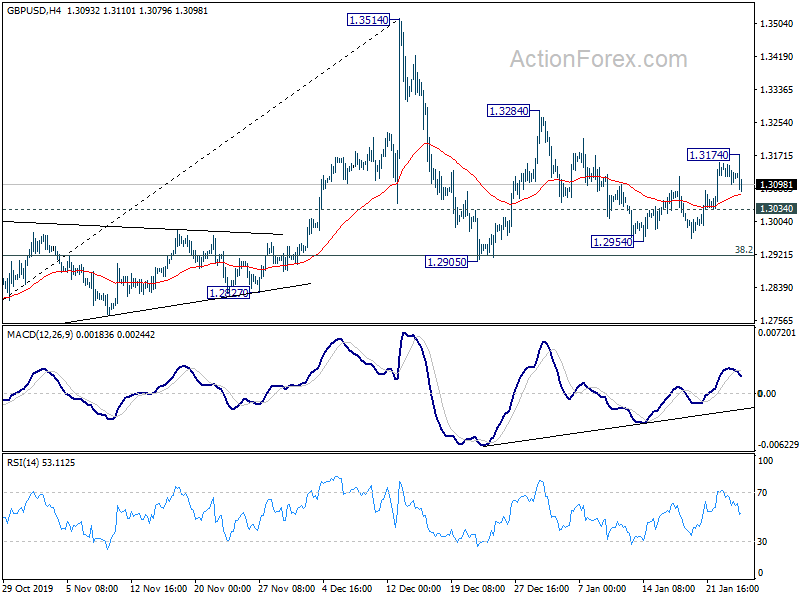

Technically, GBP/USD lost momentum after spiking higher to 1.3174. Intraday bias is turned neutral but another rise is in favor 1.3034 minor support holds. However, break of 1.3034 will turn focus back to 1.2905/54 support zone. GBP/JPY might also have a take on 142.80 minor support. Break will bring deeper fall to 140.83 support.

In Europe, FTSE is up 1.65%. DAX is up 1.50%. CAC is up 1.17%. German 10-year yield is down -0.0004 at -0.305. Earlier in Asia, Nikkei rose 0.13%. Hong Kong HSI rose 0.15%. Singapore Strait Times rose 0.17%. China was on holiday already. Japan 10-year JGB yield rose 0.0053 to -0.019.

Canada retail sales rose 0.9%, but largely from motor sales

Canada retail sales rose 0.9% mom to USD 51.5B in November, well above expectation of 0.6% mom. That also largely offset the -1.1% mom decline in October. However, the growth was primarily attributable to highest sales at motor vehicle and parts dealers. Ex-auto sales grew merely 0.2% mom, below expectation of 0.5% mom. Overall, sales were up in six provinces and all census metropolitan areas.

UK PMI composite rose to 16-month high, kills off prospect of an imminent BoE rate cut

UK PMI Manufacturing rose to 49.8 in January, up from 47.5, beat expectation of 48.8. It’s also just slightly below 50 break-even mark, and was the highest level in nine months. PMI Services rose to 52.9, up from 50.0, beat expectation of 51.1, a 16-month high. PMI Composite rose to 52.4, up from 49.3, turned expansionary, a 16-month high.

Chris Williamson, Chief Business Economist at IHS Markit, said: “The survey data indicate an encouraging start to 2020 for the UK economy… The survey is indicative of GDP rising at a quarterly rate of approximately 0.2% in January, representing a welcome revival of growth after the malaise seen in the closing months of 2019…”It seems likely that the rise in the PMI kills off the prospect of an imminent rate cut by the Bank of England, with policymakers taking a wait and see approach as they assess the performance of the economy in the post-Brexit environment.”

Eurozone PMI composite unchanged at 50.9, failed again to pick-up momentum

Eurozone PMI Manufacturing rose to 47.8 in January, up from 46.3, beat expectation of 46.9. PMI Services, however, dropped to 52.2, down from 52.8, missed expectation of 53.0. PMI Composite was unchanged at 50.9.

Andrew Harker, Associate Director at IHS Markit said: “While the year may have changed, the performance of the eurozone economy was a familiar one in January. Output growth was unchanged from the modest pace seen in December, signalling that the economy failed again to record a pick-up in growth momentum.

“Overall, a stable picture for both growth and inflation will likely reassure the European Central Bank that they are safe to keep monetary policy fixed for now while carrying out a strategy review.”

German PMI manufacturing rose to 45.2, storm clouds starting to clear

Germany PMI Manufacturing rose to 45.2 in January, up from 43.7, beat expectation of 44.6. That’s also a 11-month high even though it’s deep in contraction region. PMI Services rose to 54.2, up from 52.9, beat expectation of 54.0. PMI Composite rose to 51.1, up from 50.2, a 5-month high.

Phil Smith, Principal Economist at IHS Markit said: “A number of positive takeaways from January’s flash PMI survey suggest the storm clouds over the German economy may be starting to clear. The drag from the downturn in manufacturing continues to ease as the sector moves closer to stabilisation, while the services economy is back growing at a robust pace.

France PMI composite dropped to 51.5, but private sector stays in expansion in the near term

France PMI Manufacturing rose to 51.0 in January, up from 50.4, beat expectation of 50.5. PMI Services dropped to 51.7, down from 52.4, missed expectation of 52.1. PMI Composite dropped to 51.5, down from 52.0, hitting a 4-month low.

Pollyanna De Lima, Principal Economist at IHS Markit said: “The flash PMI data continued to show a slowdown in economic growth across France.” but “Encouragingly companies across both sectors are in buoyant mood regarding the year-ahead outlook for business activity, with optimism at a nine-month high. This upbeat growth projections continued to drive job creation and should ensure the private sector stays in expansion territory in the near-term.”

Japan CPI core accelerated to 0.7%, BoJ minutes show concerns on overseas

Japan national CPI (all-item) accelerated from 0.8% yoy in December, up from 0.5% yoy, beat expectation of 0.7% yoy. CPI core (ex-fresh food), rose to 0.7% yoy, up from 0.5% yoy, beat expectations. CPI core-core (ex-fresh food, energy) also rose to 0.9% yoy, up from 0.8% yoy and matched expectations. While core CPI remains well below BoJ’s 2% target, the pickup should be welcomed by the central bank.

In the minutes of December BoJ meeting, some members expressed concerns that gloomy global outlook could underscores market expectations. A few members noted “considering the risk that overseas economies could recover only to a small extent or slow further, the outlook for exports could not be viewed optimistically.”

Falling global demand might also hurt household income. Some noted that “Close attention should be paid to how developments in corporate profits … would affect winter bonuses.” Capital spending has shown signs of weakness, which is a “matter of concern” too.

Japan PMI composite rose to 51.1, domestic-led economic recovery

Japan PMI Manufacturing rose to 49.3 in January, up from 48.4, beat expectation of 48.7. PMI Services rose notably to 52.1, up from 49.4, back in expansion. PMI Composite also rose to 51.1, up from 48.6, turned into expansion.

Joe Hayes, Economist at IHS Market, said: “Positive signs have emerged for Japan’s economy at the start of 2020, with flash PMI data pointing to a domestic-led economic recovery”. While Q4 would likely post an “ugly decline in GDP”, January PMI will “certainly allay fears” of an “impending technical recession”.

Australia PMI composite dropped to record low 48.6, softness spilled over to 2020

Australia PMI Manufacturing dropped to 49.1 in January, down from 49.2. PMI Services dropped to 48.9, down from 49.8. PMI Composite dropped to 48.6, down from 49.6. That’s the record worst contraction reading since the survey started in May 2016.

CBA Chief Economist, Michael Blythe said: “The January ‘flash’ results show the softness in the Australian economy at the end of 2019 has spilled over into the early part of 2020.” But, “the gloom should not be overdone. Key leading indicators like new orders and employment are showing a notably stronger result than the ‘headline’ PMI readings. And expectations about future business remain at encouraging levels”.

New Zealand CPI rose 0.5% qoq on transport costs, NZD recovers mildly

New Zealand CPI slowed to 0.5% qoq in Q4, down from 0.7% qoq, but beat expectation of 0.4% qoq. Annually, CPI accelerated to 1.9% yoy, up from 1.5% yoy, but missed expectation of 2.2% yoy. Transport cost was a main driver of quarterly inflation pickup, rose 2.1%. Recreation and culture rose 1.6%. Housing and household utilities rose 0.5%. On the other hand, food prices dropped -0.6%.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3100; (P) 1.3125; (R1) 1.3154; More…

Intraday bias in GBP/USD is turned neutral with a temporary top formed at 1.3174. Further rise is mildly in favor as long as 1.3034 minor support hods. Above 1.3174 will target 1.3284 resistance. Break will pave the way to retest 1.3514 high. On the downside, below 1.3034 minor support will turn bias to the downside for retesting 38.2% retracement of 1.1958 to 1.3514 at 1.2920.

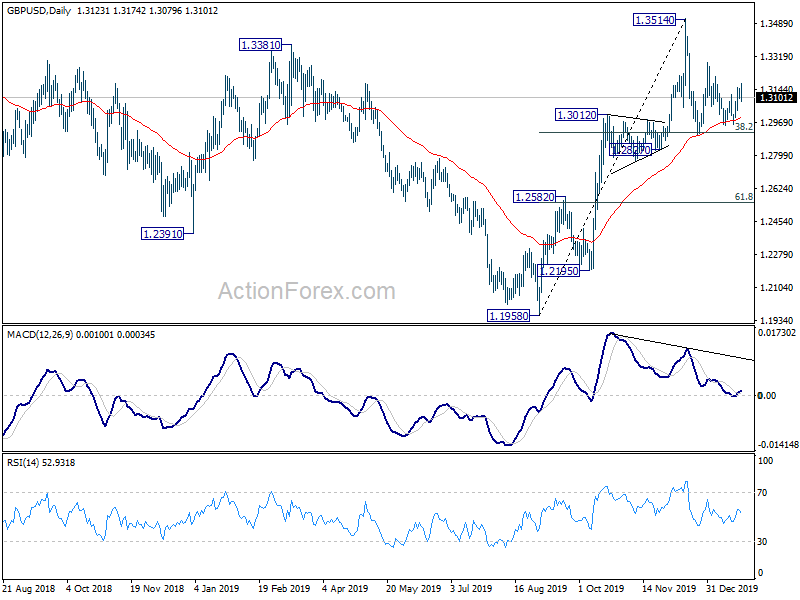

In the bigger picture, rise from 1.1958 medium term bottom is expected to extend higher to retest 1.4376 key resistance. Reactions from there would decide whether it’s in consolidation from 1.1946 (2016 low). Or, firm break of 1.4376 will indicate long term bullish reversal. In any case, for now, outlook will stay bullish as long as 1.2582 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | CPI Q/Q Q4 | 0.50% | 0.40% | 0.70% | |

| 21:45 | NZD | CPI Y/Y Q4 | 1.90% | 2.20% | 1.50% | |

| 22:00 | AUD | CBA Manufacturing PMI Jan P | 49.1 | 49.2 | ||

| 22:00 | AUD | CBA Services PMI Jan P | 48.9 | 49.8 | ||

| 23:30 | JPY | National CPI Core Y/Y Dec | 0.70% | 0.70% | 0.50% | |

| 00:30 | JPY | Manufacturing PMI Jan P | 49.3 | 48.7 | 48.4 | |

| 08:15 | EUR | France Manufacturing PMI Jan P | 51 | 50.5 | 50.4 | |

| 08:15 | EUR | France Services PMI Jan P | 51.7 | 52.1 | 52.4 | |

| 08:30 | EUR | Germany Manufacturing PMI Jan P | 45.2 | 44.6 | 43.7 | |

| 08:30 | EUR | Germany Services PMI Jan P | 54.2 | 54 | 52.9 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Jan P | 47.8 | 46.9 | 46.3 | |

| 09:00 | EUR | Eurozone Services PMI Jan P | 52.2 | 53 | 52.8 | |

| 09:30 | GBP | Manufacturing PMI Jan P | 49.8 | 48.8 | 47.5 | |

| 09:30 | GBP | Services PMI Jan P | 52.9 | 51.1 | 50 | |

| 13:30 | CAD | Retail Sales M/M Nov | 0.90% | 0.60% | -1.20% | -1.10% |

| 13:30 | CAD | Retail Sales ex Autos M/M Nov | 0.20% | 0.50% | -0.50% | -0.40% |

| 14:45 | USD | Manufacturing PMI Jan P | 52.3 | 52.4 | ||

| 14:45 | USD | Services PMI Jan P | 53.1 | 52.8 |

{kind=link}