The stimulus deal in US Congress gave markets just a very brief lift. European indices turned mixed after initial rally while US futures are essentially flat. Trading in the currency markets is subdued too with Australian Dollar leading commodity currencies higher. Yen, Swiss Franc and Dollar remain soft. Gold appears to be losing some upside momentum after hitting 1639.28. WTI crude oil is staying in tight range around 24/25 handle. Economic data continues to be ignored as focus remains on coronavirus pandemic, which death toll is set to break 20k handle soon.

Technically, we’d maintain that Dollar’s pull back this week is merely a correction. There is no development that threatens near term up trend. Indeed, there is prospect of ending the correction soon, as both GBP/USD and AUD/USD touched 4 hour 55 EMAs already. There’s no change in Dollar’s bullish outlook as long as 1.0981 resistance in EUR/USD, 1.2129 resistance in GBP/USD, 0.9901 support in USD/CHF hold.

In Europe, currently, FTSE is up 0.20%. DAX is down -1.62%. CAC is down -0.04%. German 10-year yield is up 0.027 at -0.297. Earlier in Asia, Nikkei rose 8.04%. Hong Kong HSI rose 3.81%. China Shanghai SSE rose 2.17%. Singapore Strait Times rose 6.07%. Japan 10-year JGB yield dropped -0.0015 to 0.038.

US durable goods orders rose 1.2%, but ex-transport orders dropped -0.6%

US durable goods orders rose 1.2% mom to US D249.4B in February, much better than expectation of -0.9% decline. However, ex-transport orders dropped -0.6%, below expectation of -0.2%. Ex-defense orders rose 0.1%.

House price index rose 0.3% mom in January, matched expectations.

German Ifo collapsed to 86.1, steepest decline since reunification

Germany Ifo Business Climate collapsed from 96.0 to 86.1 in March. That’s the steepest decline ever recorded since German reunification. It’s also the lowest value since July 2009. Current Situation index dropped from 99.0 to 93.0. Expectations Index dropped from 93.1 to 79.7.

By sector, manufacturing index dropped from -1.6 to -18.2. It’s the lowest since August 2009. Service index dropped from 17.4 to -7.6, biggest decline on record since 2005. Trade index dropped form 1.0 to -21.4. Construction index dropped from 12.9 to 5.0.

Ifo economist Klaus Wohlrabe said the economy could contract by between -5% and -20% this year depending on the length of the shutdown caused by the pandemic. He expected there to be a severe recession that would last for at least two quarters.

UK CPI slowed to 1.7%, core CPI rose to 1.7%

UK headline CPI slowed to 1.7% yoy in February, down form 1.8% yoy, matched expectation. However, core CPI accelerated to 1.7% yoy, up from 1.6% yoy, beat expectation of 1.5% yoy. RPI slowed to 2.5% yoy, down form 2.7% yoy, beat expectation of 2.4% yoy.

PPI input was at -1.2% mom, -0.5% yoy in February, versus expectation of 0.2% mom, 3.6% yoy. PPI Output was at -0.3% mom, 0.4% yoy, versus expectation of 0.0% mom, 1.4% yoy. PPI output core was at -0.1% mom, 0.4% yoy, versus expectation of 0.2% mom, 0.6% yoy.

AmCham China: 22% US companies resumed normal operations in China

The American Chamber of Commerce in China (“AmCham China”) released a coronavirus impact survey, taken between March 14 and 18 on 199 US businesses in China. 57% of respondents expect 2020 revenues to decrease if business cannot return to normal before April 30. 60% expect revenue to drop anyway between 10% and 50% or more if business cannot return to normal before August 30.

Chairman Greg Gilligan: “Close to half of the companies said the global spread of the virus would have a moderate-to-strong impact on their China operations. But the views aren’t all grim: nearly a quarter of our companies expect a return to normal business operations by the end of April, while 22% have already resumed normal operations, and 40% report they will maintain previously planned investment levels, up significantly from last month’s survey.”

BoJ opinions: Impact of coronavirus could be significant and not just temporary

In the summary of opinions of BoJ’s March 16 meeting, it’s noted that “global financial and capital markets have been unstable” and “Japan’s economic activity has been week” due to growing uncertainties over coronavirus pandemic. “Downward pressure on Japan’s economy has been increasing due to a constrain on economic activity”. Firms are facing a “sudden deterioration in business conditions” and “the situation has been very serious”.

It’s also warned that the impact of the pandemic can be “significant and not just temporary”. And there is concern that the economy could “remain weak even after overseas economies recover”. There are “doubts regarding the scenario that the economy will strongly recover after the crisis caused by COVID-19 recedes.”

Regarding policy responses, “it is essential to maintain a strong cooperative framework between the Bank and the government as well as among major central banks, while closely sharing information.”

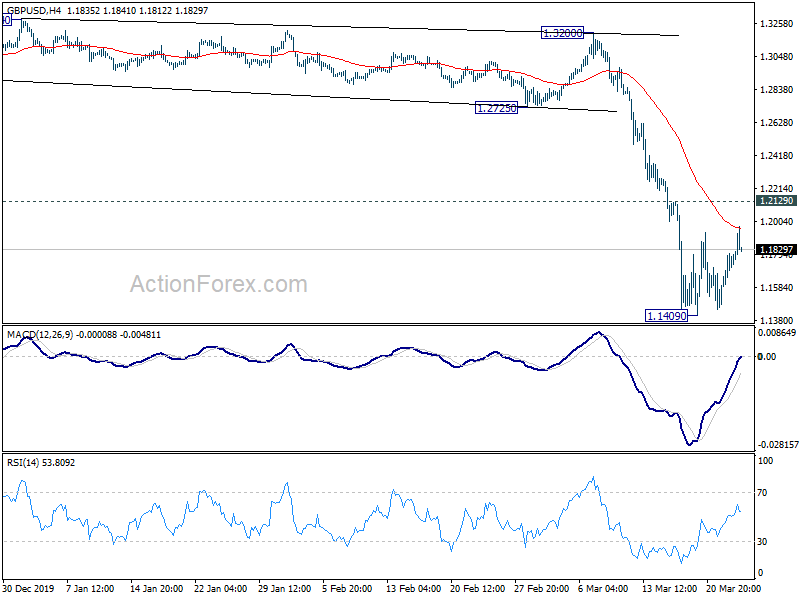

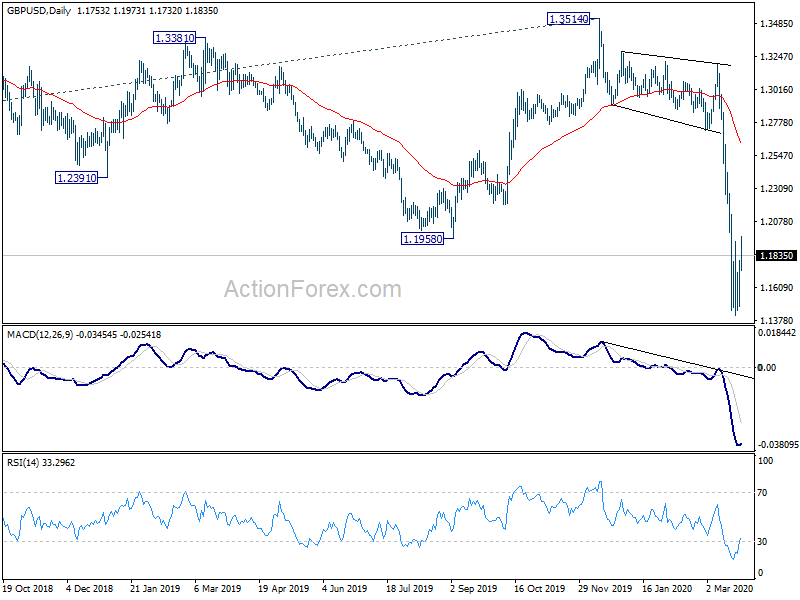

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1583; (P) 1.1692; (R1) 1.1877; More…

No change in GBP/USD’s outlook as consolidation form 1.1409 is still extending. Stronger recovery cannot be ruled out. But upside should be limited by 1.2129 minor resistance to bring fall resumption. On the downside, break of 1.1409 will resume larger down trend. However, firm break of 1.2129 will dampen immediate bearish case and bring stronger rebound.

In the bigger picture, down trend from 2.1161 (2007 high) has just resumed. Next medium term target will be 61.8% projection of 1.7190 to 1.1946 from 1.3514 at 1.0273. In any case, outlook will remain bearish as long as 1.3514 resistance holds, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Feb | 594M | 550M | -340M | -414M |

| 07:00 | GBP | CPI M/M Feb | 0.40% | 0.30% | -0.30% | |

| 07:00 | GBP | CPI Y/Y Feb | 1.70% | 1.70% | 1.80% | |

| 07:00 | GBP | Core CPI Y/Y Feb | 1.70% | 1.50% | 1.60% | |

| 07:00 | GBP | RPI M/M Feb | 0.50% | 0.60% | -0.40% | |

| 07:00 | GBP | RPI Y/Y Feb | 2.50% | 2.40% | 2.70% | |

| 07:00 | GBP | PPI Input M/M Feb | -1.20% | 0.20% | 0.90% | |

| 07:00 | GBP | PPI Input Y/Y Feb | -0.50% | 3.60% | 2.10% | 1.60% |

| 07:00 | GBP | PPI Output M/M Feb | -0.30% | 0.00% | 0.30% | |

| 07:00 | GBP | PPI Output Y/Y Feb | 0.40% | 1.40% | 1.10% | 1.00% |

| 07:00 | GBP | PPI Core Output M/M Feb | -0.10% | 0.20% | 0.10% | |

| 07:00 | GBP | PPI Core Output Y/Y Feb | 0.40% | 0.60% | 0.70% | 0.20% |

| 09:00 | EUR | Germany IFO Business Climate Mar | 86.1 | 87.7 | 87.7 | |

| 09:00 | EUR | Germany IFO Current Assessment Mar | 93 | 93.7 | 93.8 | |

| 09:00 | EUR | Germany IFO Expectations Mar | 79.7 | 82 | 82 | |

| 09:30 | GBP | DCLG House Price Index Y/Y Jan | 1.30% | 2.40% | 2.20% | |

| 11:00 | GBP | CBI Realized Sales Mar | -3 | -15 | 1 | |

| 12:30 | USD | Durable Goods Orders Feb | 1.20% | -0.90% | -0.20% | |

| 12:30 | USD | Durable Goods Orders ex Trans Feb | -0.60% | -0.20% | 0.80% | |

| 13:00 | USD | Housing Price Index M/M Jan | 0.30% | 0.30% | 0.60% | |

| 14:00 | CHF | SNB Quarterly Bulletin Q1 | ||||

| 14:30 | USD | Crude Oil Inventories | 2.9M | 2.0M |

{kind=link}