While the US continues to post scary job numbers, the markets couldn’t care less. Investors know the numbers would be bad and it doesn’t matter how bad they are. The point is, there has to be an end to the coronavirus pandemic, which originated from China. Otherwise, the economy will just continue to turn from worse to… even worse.

Dollar picked up some buying earlier today and remains firm. It’s set to close as the strongest one for the week. On the other hand, Euro is currently the weakest one. However, Sterling’s selloff is starting to pick up. There are still a few hours to go before we know who’s the worst performing.

In other markets, Gold is staying in tight range around 1615. WTI crude oil’s break of 28.39 resistance finally indicates short term bottoming at 20.40. Further rise would be seen to 55 day EMA (now at 39.25). DOW futures is slightly lower by less than 100 pts. In Europe, FTSE is down -1.16%. DAX is down -0.23%. CAC is down -1.12%. German 10-year yield is down -0.0065 at -0.442. Earlier in Asia, Nikkei rose 0.01%. Hong Kong HSI dropped -0.19%. China Shanghai SSE dropped -0.60%. Singapore Strait Times dropped -2.60%. Japan 10-year JGB yield rose 0.0032 to -0.0008.

US NFP dropped -701k, unemployment surged to 4.4%

US non-farm payroll employment dropped -701k in March. Two-thirds of the drop occurred in leisure and hospitality. Notable declines also occurred in health case and social assistance, professional and business services, retail trade, and construction.

Unemployment rate jumped from 3.5% to 4.4%. That’s the largest over-the-month increase since January 1975. Labor force participation rate dropped -0.7% to 62.7%. Average hourly earnings rose 0.4% mom.

Eurozone retail sales rose 0.9%, EU sales rose 0.8%

Eurozone retail sales grew 0.9% mom in February, versus expectation of 0.1% mom. The volume of retail trade increased by 2.4% for food, drinks and tobacco and 0.2% for non-food products, while automotive fuels fell by 0.1%.

EU retail sales grew 0.8% mom. Among Member States for which data are available, the highest increases in the total retail trade volume were registered in Estonia (+4.4%), Latvia (+3.5%) and Portugal (+3.0%). Decreases were observed in Ireland (-2.7%), Slovenia (-1.8%), Croatia and Poland (both -0.2%).

Eurozone PMI composite finalized at 29.7, GDP contracting near to -10% annualized

Eurozone PMI Services was finalized at 26.4 in March, down from February’s 52.6. PMI Composite was finalized at 29.7, own from February’s 51.6. that’s the biggest single monthly fall, as well as a survey record low. Looking at some member states, Germany PMI Composite dropped to 35.0, France to 28.9, Spain to 26.7, Italy to 20.2, all record lows.

Chris Williamson, Chief Business Economist at IHS Markit said: ” The data indicate that the eurozone economy is already contracting at an annualised rate approaching 10%, with worse inevitably to come in the near future… No countries are escaping the severe downturn in business activity, but the especially steep decline in of Italy’s service sector PMI to just 17.4 likely gives a taste of things to come for other countries as closures and lockdowns become more prevalent and more strictly enforced in coming months… The ultimate economic cost of the COVID-19 outbreak cannot be accurately estimated until we get more clarity on the duration and scale of the pandemic.”

UK PMI composite finalized at 36.0, almost certain to experience a deep contraction in Q2

UK PMI Services was finalized at 34.5 in March, down from February’s 53.2. It’s the worst reading since survey began in 1996. PMI Composite was finalized at 36.0, lowest since series began in 1998.

Tim Moore, Economics Director at IHS Markit: “With the UK economy now almost certain to experience a deep contraction in the second quarter of the year, perhaps the most important aspect of the Services PMI to watch for hopeful signs will be any recovery in the business expectations sub-index from the record low seen in March.”

Japan PMI services dropped to 33.8, GDP contracting at 8% annualized rate

Japan PMI Services dropped to 33.8 in March, down from 46.8. The index was close to record low seen in February 2009 (33.7). PMI Composite dropped to 36.2, down from 47.0. Markit said that output fell at near record pace as coronavirus pandemic hits demand. Employment declined as operating requirements slumped. Also, business activity was expected to fall sharply over the coming 12 months.

Joe Hayes, Economist at IHS Markit, said, latest data showed that the economic impact from coronavirus pandemic “has become widespread”. The sharp fall signals “how aggressive and sudden the drop in activity has been”. The combined manufacturing and services PMI already point to “GDP contracting at an annual of around 8%”. If the outbreak were to escalate in Japan, Q2 GDP could be “poised for an annual decline in excess of 10%”.

ADB slashes China’s growth forecast to 2.3% in 2020, but rebound expected next year

The Asian Development Bank slashed China’s growth forecast to just 2.3% in 2020 on coronavirus pandemic. Though, it expects a strong bounce back of 7.3% in 2021. ADP noted warned that a new round of domestic infection of further global spread could “increasingly dampen investor sentiment, consumer spending, credit sustainability, and overall economic activity”. Revival of trade conflict with the US is another risk.

For Asia, growth in 2020 will slow to 2.2%, down from 2019’s 5.2%, then bounces back to 6.2% in 2021. Excluding Taiwan, Hong Kong, South Korea and Singapore, developing Asia is forecasts to grow 2.4% in 2020, then rebounds to 6.7% in 2021.

China Caixin PMI services recovered to 43, situation requires policymakers to cut GDP growth target

China Caixin PMI Services recovered to 43.0 in March, up from 26.5. PMI Composite rose from 27.5 to 46.7, second lowest reading in 11 years. Caixin said that business activity and new work both declined at slower rates, but employment fell at quickest pace on record. Output charges also cut at fastest rate since April 2009.

Zhengsheng Zhong, Chairman and Chief Economist at CEBM Group said: “The recovery of economic activity remained limited in March, although the domestic epidemic was contained. In the first two months this year, China’s value-added industrial output and services output dropped 13.5% and 13% year-on-year, respectively.

“Estimates suggest their declines haven’t been as steep in March and the country’s first-quarter GDP is likely to have dropped significantly. Such a situation requires policymakers to cut this year’s GDP growth target and step up countercyclical efforts to support areas like consumption and infrastructure, particularly given the accelerated contraction in the service sector job market.”

Australia AiG construction dropped to 37.9, retail sales rose 0.5%

Australia AiG Construction Index dropped to 37.9 in March, down from 42.7. That’s the lowest level since May 2013. Across the four construction sectors, the house building sector indicated modest growth for a fourth consecutive month (trend). Contractions in the apartment and commercial construction sectors were steeper (a lower index result), while the contraction in engineering construction activity eased slightly in March.

Retail sales rose 0.5% mom in February. “Retailers reported a range of impacts from COVID-19 in February” said Ben James, Director of Quarterly Economy Wide Surveys, “with increases in food retailing slightly offset by falls in more discretionary spending.”

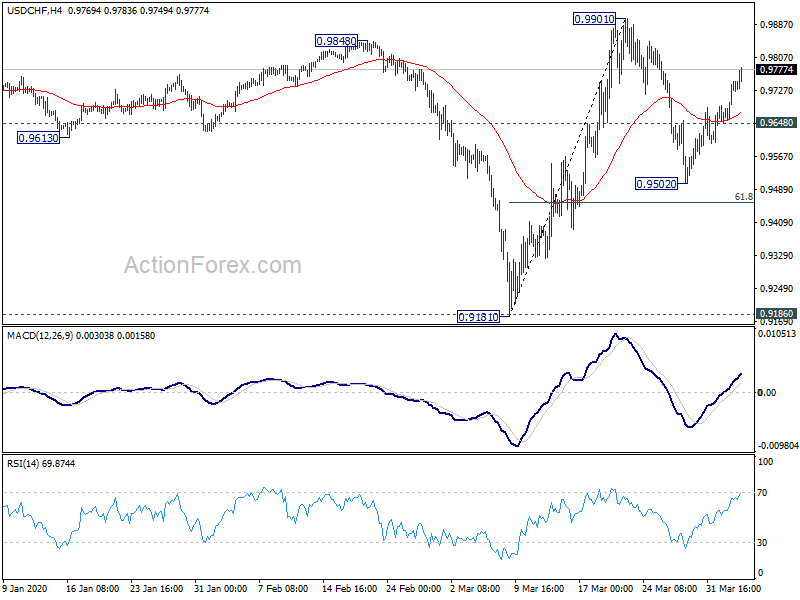

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9675; (P) 0.9713; (R1) 0.9774; More…

USD/CHF’s rebound form 0.9502 extends to as high as 0.9783 so far. Intraday bias remains on the upside for retesting 0.9901. Break will resume whole rise from 0.9181. On the downside, break of 0.9648 minor support will extend the correction from 0.9901 with another fall. Intraday bias will be turned back to the downside for 61.8% retracement of 0.9181 to 0.9901 at 0.9456.

In the bigger picture, decline from 1.0237 is seen as the third leg of the pattern from 1.0342 (2016 low). It could have completed at 0.9181 after hitting 0.9186 key support (2018 low). Further rise could be seen to retest 1.0237 high. After all, medium term range trading will likely continue between 0.9181/1.0237 for some time.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Construction Index Mar | 37.9 | 42.7 | ||

| 00:30 | AUD | Retail Sales M/M Feb F | 0.50% | 0.40% | -0.30% | |

| 01:45 | CNY | Caixin Services PMI Mar | 43 | 39.6 | 26.5 | |

| 07:15 | EUR | Spain Services PMI Mar | 23 | 25 | 52.1 | |

| 07:45 | EUR | Italy Services PMI Mar F | 17.4 | 21 | 52.1 | |

| 07:50 | EUR | France Services PMI Mar F | 27.4 | 29 | 29 | |

| 07:55 | EUR | Germany Services PMI Mar F | 31.7 | 34.3 | 34.5 | |

| 08:00 | EUR | Eurozone Services PMI Mar F | 26.4 | 28.4 | 28.4 | |

| 08:30 | GBP | Services PMI Mar F | 34.5 | 35.4 | 35.7 | |

| 09:00 | EUR | Retail Sales M/M Feb | 0.90% | 0.10% | 0.60% | 0.70% |

| 12:30 | USD | Nonfarm Payrolls Mar | -701K | -123K | 273K | 275 K |

| 12:30 | USD | Average Hourly Earnings M/M Mar | 0.40% | 0.20% | 0.30% | |

| 12:30 | USD | Unemployment Rate Mar | 4.40% | 4.00% | 3.50% | |

| 13:45 | USD | Services PMI Mar F | 39.1 | 39.1 | ||

| 14:00 | USD | ISM Non-Manufacturing PMI Mar | 48 | 57.3 |

{kind=link}