Commodity currencies remain the strongest one today as supported by risk appetite. Sentiments are lifted by expectations of lockdown exits as well as optimism on coronavirus treatment. Dollar remains generally weak with Fed providing little inspirations. Euro and Swiss Franc are not much better than the greenback. Euro’s weakness is the main reason keeping Dollar index afloat. Focus is turning to ECB rate decision, as well as Eurozone GDP data today. We’ll see if Euro traders would finally take a direction against the greenback.

Technically, Aussie continues to look unstoppable. EUR/AUD, AUD/JPY, AUD/CAD are all around key levels and a pull back is due. We’d continue to look for sign of topping as AUD/USD approaches 0.6670 key resistance. But break of 0.6505 minor support is needed to signal temporary topping first. USD/CAD is on track to extend the correction from 1.4667 through 1.3855 support. But we’d expect strong support from 1.3762 fibonacci level to bring rebound.

In Asia, Nikkei is up 2.57%. Hong Kong HSI is up 0.28%. China Shanghai SSE is up 1.34%. Singapore Strait Times is up 2.05%. Japan 10-year JGB yield is up 0.0055 at -0.039. Overnight, DOW rose 2.21%. S&P 500 rose 2.66%. NASDAQ rose 3.57%. 10-year yield rose 0.017 to 0.627.

Dollar index shrugs FOMC, DOW jumped on remdesivir news

Fed kept monetary policy unchanged overnight as widely expected and reiterated the pledge to maintain rate target at 0-0.25% ” until it is confident that the economy has weathered recent events and is on track to achieve its maximum employment and price stability goals.” Chairman Jerome Powell said there will be a “large increase” in economic activity when people are coming out to spend again while unemployment goes down. However, “it is unlikely it will bring us quickly back to pre-crisis levels,” he added. “Trying to be really precise about when that might happen and what the numbers might look like – it is very tough to do that.”

Some suggested readings on Fed:

- Fed Markedly Downgraded Economic Assessments on Sharp Decline in Activities and Surge in Unemployment

- No New Measures, But Fed Support Not Going Away Any Time Soon

- No Surprises from FOMC Today, But Ongoing Commitment to “Use Its Full Range of Tools” to Support the Economy

- Northern Exposure: US GDP 5% Annualised Fall in Q1 Evidence of Shock to Come

- April 2020 Fed Meeting Instant Analysis

Dollar softened a little bit further after FOMC’s announcement and press conference. But there was no avalanche selling. Dollar index is back pressing 55 day EMA and outlook is unchanged. Price actions from 102.99 are seen as a corrective pattern. Fall from 100.93 is likely the third leg. Break of 55 day EMA will pave the way to 98.27 support and possibly below. But downside should be contained by 61.8% retracement of 94.65 to 102.99 at 97.83 to bring rebound.

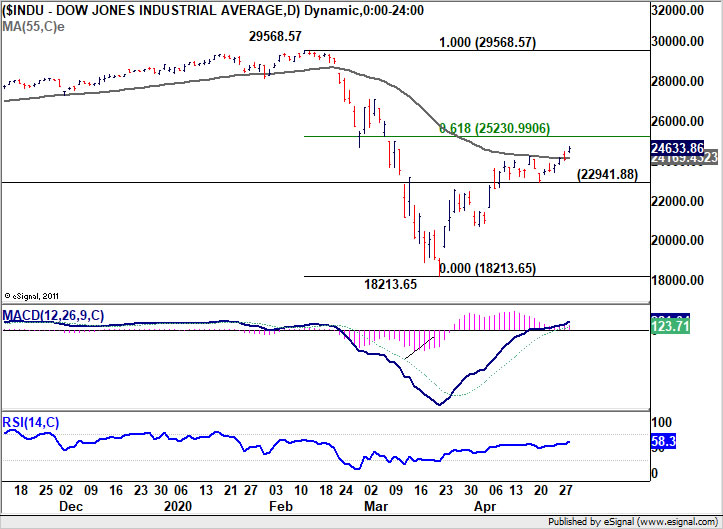

DOW rose 532.31 pts, or 2.21% to close at 24633.86. But that’s mainly due to news that Gilead Sciences found promising results of its experiments on coronavirus treatment drug remdesivir. Technically, DOW’s rebound from 18213.65 could extend higher. But we’d expect strong resistance from 61.8% retracement of 29568.57 to 18213.65 at 25230.99 to limit upside, at least on first attempt. Break of 22941.88 support will mark short term topping and bring near term reversal.

Japan industrial production, retail sales dropped most since Oct

Japan’s industrial production dropped -3.7% mom in March, down from February’s -0.3% mom, but was better than expectation of -5.2% mom. But that still the sharpest fall in production since October last year. Retail sales dropped -4.6% yoy, down from February’s 1.6% yoy, slightly better than expectation of -4.7% yoy. That’s also the sharpest decline since last October’s sales tax hike. Housing starts dropped -7.6% yoy, much better than expectation of -16.0% yoy.

The parliament is set to enact a JPY 25.69 trillion supplementary budget for fiscal 2020 today. The House of Councillors is generally expected to approve the extra budget, which was passed by House of Representative already, to cushion the economy from the impact of the coronavirus pandemic. Meanwhile, Prime Minister Shinzo Abe would announce the extension of nationwide state of emergency that is due to end next Wednesday.

China PMI manufacturing dropped to 50.8 while non-manufacturing improved

China’s official NBS PMI manufacturing dropped to 50.8 in April, down from 52.0, missed expectation of 51.0. In particular, new export orders plunged sharply to 33.5. But PMI non-manufacturing improved to a three-month high of 53.2, up from 52.3, beat expectation of 52.8. The set of data suggests that China’s economy is on a double-track. Hope of a strong come back in manufacturing is dim as coronavirus pandemic is continuing elsewhere. Global recession will continue to heap on downward pressure in the sector in the coming months.

New Zealand ANZ business confidence off low, offers a glimmer of light

New Zealand ANZ Business Confidence improved to -66.6 in April, up from preliminary reading of -73.1, while down from March reading of -63.5. All sectors are deep in negative with retail at -70.7, manufacturing at -65.3, agriculture at -89.7, construction at -71.8 and services at -60.3. Activity Outlook also improved slightly to -55.1, up from preliminary reading of -43.6, but down from March’s -26.7. All sectors are also deep in negative with retail at -67.2, manufacturing at -52.7, agriculture at -44.8, construction at -57.9, and services at -52.4.

ANZ said, “a glimmer of light at the end of the tunnel emerged over the month, with the country making solid progress in its COVID-19 battle”. However, “the levels of most indicators remain at levels that were frankly unthinkable before COVID-19 reached our shores. Businesses are really hurting. And it’s not just expectations. The proportion of firms that have already seen lower activity and have let staff go continues to rise. That will clearly remain a theme for some time.

Looking ahead – ECB to highlight an extremely busy day

The economic calendar is very busy today. ECB rate decision and press conference is a highlight. We expect ECB to keep its powder dry at this week’s meeting, after launching several stimulus measures last month. The central bank should maintain a dovish tone, indicating disappointing economic data and pledging the take further actions if needed. As EU has so far failed to agree on substantial fiscal actions, we expect ECB will in coming months step up its QE measures. Extension of PEPP would be a likely move. More in ECB to Send a Dovish Tone and Pledge to Take Further Actions if Needed. Rate Cut Appears Less Relevant than QE.

On the data front, Eurozone will also release Q1 GDP, unemployment rate and CPI. Swiss will release retail sales and KOF economic barometer. Later in the day, Canada will release February GDP, which carries little significance. US will release March personal income and spending, jobless claims and Chicago PMI.

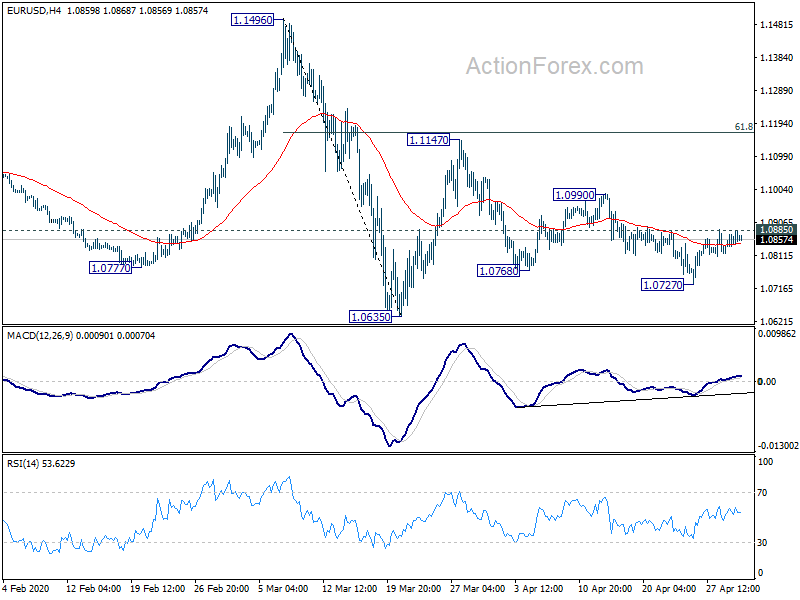

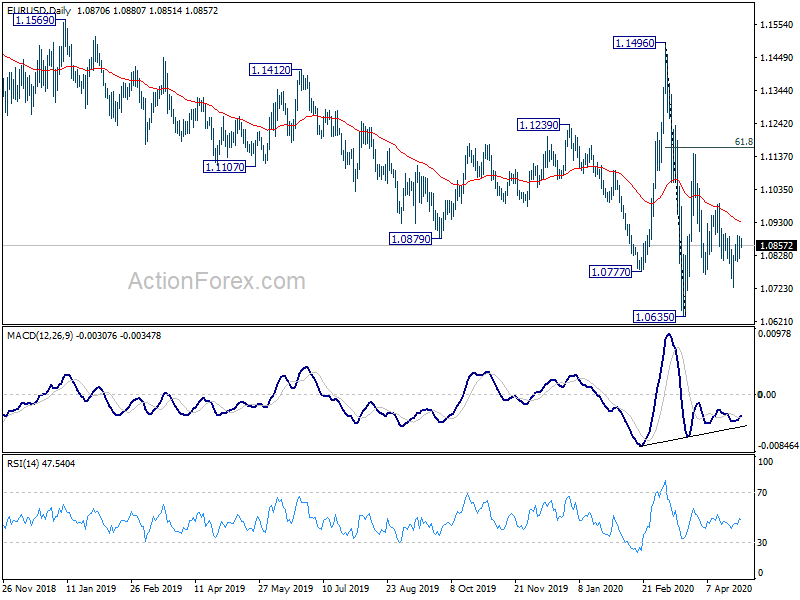

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0836; (P) 1.0861; (R1) 1.0903; More…

Intraday bias in EUR/USD stays neutral and outlook is unchanged. Price actions from 1.0635 are seen as a corrective pattern. on the upside, break of 1.0885 minor resistance will start the third leg, towards 1.1147 resistance. But upside should be limited by 61.8% retracement of 1.1496 to 1.0635 at 1.1167. On the downside, break of 1.0727 will target a test on 1.0635 low.

In the bigger picture, as long as 1.1496 resistance holds, whole down trend from 1.2555 (2018 high) should still be in progress. Next target is 1.0339 (2017 low). However, sustained break of 1.1496 will argue that such down trend has completed. Rise from 1.0635 could then be seen as the third leg of the pattern from 1.0339. In this case, outlook will be turned bullish for retesting 1.2555.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Industrial Production M/M Mar P | -3.70% | -5.20% | -0.30% | |

| 23:50 | JPY | Retail Trade Y/Y Mar | -4.60% | -4.70% | 1.60% | |

| 1:00 | CNY | NBS Manufacturing PMI Apr | 50.8 | 51 | 52 | |

| 1:00 | CNY | NBS Non-Manufacturing PMI Apr | 53.2 | 52.8 | 52.3 | |

| 1:00 | NZD | ANZ Business Confidence Apr | -66.6 | -73.1 | ||

| 1:30 | AUD | Private Sector Credit M/M Mar | 1.10% | 0.30% | 0.40% | |

| 1:30 | AUD | Import Price Index Q/Q Q1 | -1.00% | 1.00% | 0.70% | |

| 5:00 | JPY | Housing Starts Y/Y Mar | -7.60% | -16.00% | -12.30% | |

| 5:30 | EUR | France GDP Q/Q Q1 P | -5.8% | -4.00% | -0.10% | |

| 6:00 | EUR | Germany Retail Sales M/M Mar | -5.6% | -7.50% | 1.20% | |

| 6:30 | CHF | Real Retail Sales Y/Y Mar | -3.60% | 0.30% | ||

| 6:45 | EUR | France Consumer Spending M/M Mar | -5.50% | -0.10% | ||

| 7:00 | CHF | KOF Economic Barometer Apr | 58 | 92.9 | ||

| 7:55 | EUR | Germany Unemployment Change Apr | 70K | 1K | ||

| 7:55 | EUR | Germany Unemployment Rate Apr | 5.20% | 5.00% | ||

| 8:00 | EUR | Italy Unemployment Rate Mar | 10.50% | 9.70% | ||

| 9:00 | EUR | Eurozone GDP Q/Q Q1 P | -3.30% | 0.10% | ||

| 9:00 | EUR | Eurozone GDP Y/Y Q1 P | -2.80% | 1.00% | ||

| 9:00 | EUR | Eurozone Unemployment Rate Mar | 7.70% | 7.30% | ||

| 9:00 | EUR | Eurozone CPI Y/Y Apr P | 0.00% | 0.70% | ||

| 9:00 | EUR | Eurozone CPI Core Y/Y Apr P | 0.70% | 1.00% | ||

| 10:00 | EUR | Italy GDP Q/Q Q1 P | -5.00% | -0.30% | ||

| 10:00 | EUR | Italy GDP Y/Y Q1 P | -3.90% | 0.10% | ||

| 11:45 | EUR | ECB Interest Rate Decision | 0.00% | 0.00% | ||

| 12:30 | EUR | ECB Press Conference | ||||

| 12:30 | CAD | GDP M/M Feb | 0.10% | 0.10% | ||

| 12:30 | CAD | Raw Material Price Index Mar | -4.70% | |||

| 12:30 | CAD | Industrial Product Price M/M Mar | -0.50% | |||

| 12:30 | USD | Personal Income M/M Mar | -1.40% | 0.60% | ||

| 12:30 | USD | Personal Spending Mar | -5.00% | 0.20% | ||

| 12:30 | USD | PCE Price Index M/M Mar | 0.10% | |||

| 12:30 | USD | PCE Price Index Y/Y Mar | 1.60% | 1.80% | ||

| 12:30 | USD | Core PCE Price Index M/M Mar | -0.10% | 0.20% | ||

| 12:30 | USD | Core PCE Price Index Y/Y Mar | 1.70% | 1.80% | ||

| 12:30 | USD | Initial Jobless Claims (Apr 24) | 4427K | |||

| 12:30 | USD | Employment Cost Index Q1 | 0.70% | 0.70% | ||

| 13:45 | USD | Chicago PMI Apr | 36 | 47.8 | ||

| 14:30 | USD | Natural Gas Storage | 43B |

{kind=link}