Sterling weakens mildly today after UK sold government bond with a negative yield for the first time ever. According to the Debt Management office, It auctioned GBP 3.75B of 3-year bonds at an average rate of -0.003%. Demand was weak too with bid-to-cover ratio at 2.15, lowest since March. Nevertheless, Dollar and yen are not too far away with investors staying in positive mood. DOW futures point to another day of higher open. New Zealand and Australian Dollar continues to extend gains while Swiss Franc is having a sudden spike up.

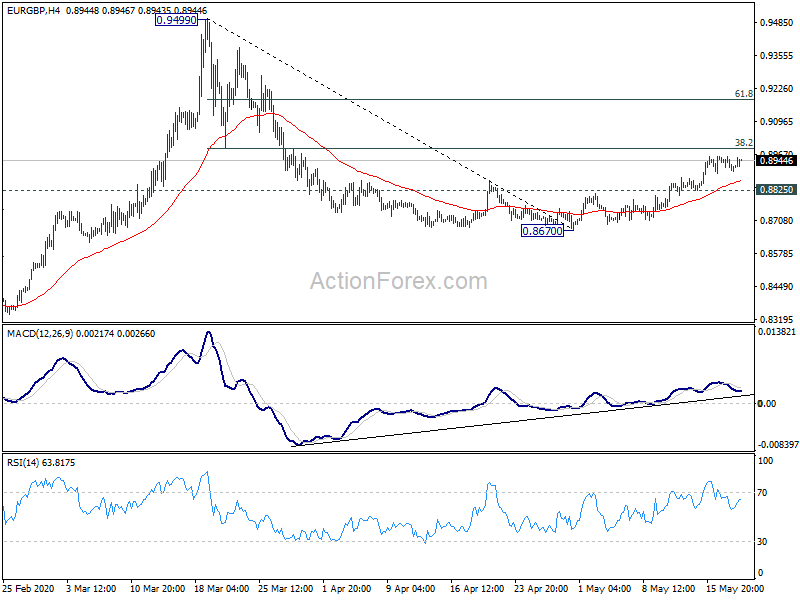

Technically, GBP/USD and GBP/JPY are losing some upside momentum but this week’s rebounds are not threatened yet. EUR/GBP is more of the focus in Sterling weakness, and is still on track to 0.8987 near term fibonacci resistance. Euro’s strength is somewhat capped by the volatility in EUR/CHF. In spite of today’s retreat, further rise is still expected in EUR/CHF as long as 1.0578 minor support holds, to 1.0710 cluster resistance. However, break of 1.0578 would turn focus back to 1.0503 low. AUD/USD would be a focus for the rest of the week as rally resumption will put 0.6670 key resistance level into focus.

In Europe, FTSE is currently up 0.47%. DAX is up 0.29%. CAC is down -0.22%. German 10-year yield is up 0.008 at -0.455. Earlier in Asia, Nikkei rose 0.79%. Hong Kong HSI rose 0.05%. China Shanghai SSE dropped -0.51%. Singapore Strait Times dropped -0.75%. Japan 10-year JGB yield rose 0.0017 to 0.003.

Canada in deflation with CPI at -0.2% in April

Canada CPI turned negative in April, dropped to -0.2% yoy, down from March’s 0.9% yoy. That’s also slightly below expectation of -0.1% yoy. The decline was mainly due to fall in energy prices as a result of coronavirus pandemic.

CPI common slowed slightly by -01.% to 1.6% yoy, below expectation of 1.7% yoy. CPI median, was unchanged at 2.0% yoy, above expectation of 1.9% yoy. CPI trimmed was unchanged at 1.8% yoy, matched expectations.

Also from Canada, whole sale sales dropped -2.2% mom in March, better than expectation of -4.5% mom.

Eurozone CPI finalized at 0.3% in April, core CPI at 0.9%

Eurozone CPI was finalized at 0.3% yoy in April, down from 0.7% yoy in March. Core CPI was finalized at 0.9% yoy, down from March’s 1.0% yoy. In April, the highest contribution to the annual Eurozone inflation rate came from food, alcohol & tobacco (+0.67%), followed by services (+0.52%), non-energy industrial goods (+0.09%) and energy (-0.97%)

EU CPI was finalized at 0.7% yoy, down from March’s 1.2% yoy. The lowest annual rates were registered in Slovenia (-1.3%), Cyprus (-1.2%), Estonia and Greece (both -0.9%). The highest annual rates were recorded in Czechia (3.3%), Poland (2.9%) and Hungary (2.5%).

Eurozone current account surplus narrowed to EUR 27.4B in March, down from EUR 37.8B.

UK CPI slowed to 0.8% in April, lowest since 2016

UK CPI dropped -0.2% mom in April. Annually, CPI slowed to 0.8% yoy, down from 1.5% yoy, below expectation of 0.9% yoy. That’s also the lowest level since August 2016. Core CPI slowed to 1.4% yoy, down from 1.6% yoy, matched expectations. RPI, an older measure of inflation, slowed to 1.5% yoy, down from 2.6% yoy.

“Falling petrol and diesel prices, combined with changes to the domestic energy price cap were the main reasons for lower inflation in April,” ONS Deputy National Statistician Jonathan Athow said.

Also released, PPI input came in at -5.2% mom, -9.8% yoy, below expectation of -3.7% mom, -8.4% yoy. PPI output was at -0.8% mom, 0.7% yoy, below expectation of -0.4% mom, -0.4% yoy. PPI output core was at -0.1% mom, 0.6% yoy, matched expectations.

Australia retail sales dropped record -17.9 in April, falls in every industry

According to preliminary data, Australia retail sales dropped -17.9% mom in April. That’s the biggest seasonally adjusted fall on record, and came after the biggest jump in March. Comparing to a year ago, retail turnover dropped -9.4% yoy. Falls were seen in every industry, with particularly strong falls in food retailing, cafes, restaurants and takeaways, and clothing, footwear and personal accessories.

Westpac-Melbourne Institute Leading Index dropped form -2.34 to -5.16 in April. The indicator points to a “broad-based economic contraction”. This is “easily the weakest reading since the GFC and is comparable to readings seen prior to Australia’s recessions in the 1990–91, 1982–83, 1974–75 and 1960–61.”

Westpac also said, ‘we do not expect the economy to return to pre-Coronavirus levels of activity before 2022.” But for now, RBA has already indicated that it’s “committed to maintaining its significant support for the economy for the foreseeable future.”

RBNZ Orr prepared to go to negative rate but a lot later

RBNZ Governor Adrian Orr said in a Bloomberg interview today that he’s currently “targeting a low and flat yield curve through the purchases bonds.” The central bank “does not want to go to negative rate at this point”. It’s “prepared to go to negative rate but a lot later” And it remains one option for RBNZ.

Also, he reiterated the view that “the operational challenge still remains with some banks still working on being able to actually operate with negative official cash rate and negative wholesale rates”.

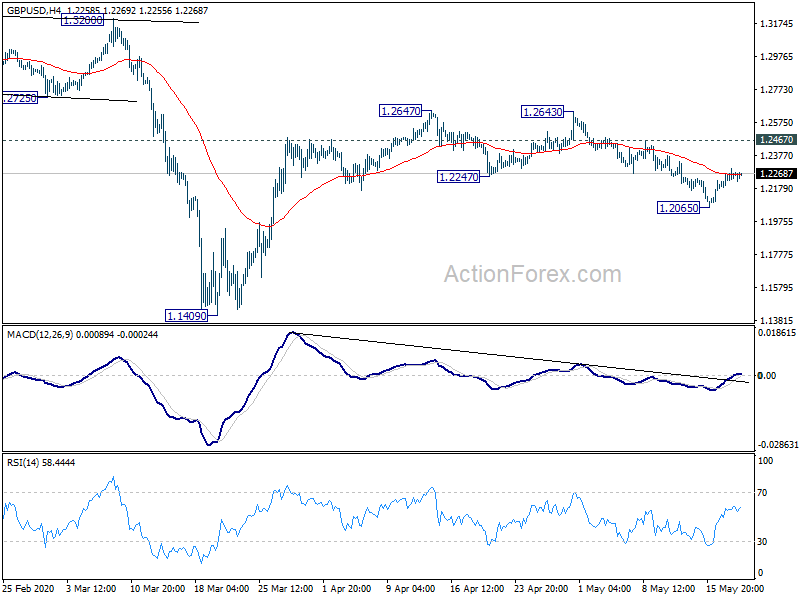

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2191; (P) 1.2243; (R1) 1.2303; More….

GBP/USD continues to struggle around 4 hour 55 EMA and intraday bias remains neutral first. Recovery from 1.2065 might extend higher. But as long as 1.2467 resistance holds, another fall is mildly in favor. We’ll holding on to the view that corrective rise from 1.1409 should have completed. On the downside, below 1.2065 will target a test on 1.1409 low. However, on the upside, break of 1.2467 will turn bias to the upside for 1.2647 resistance.

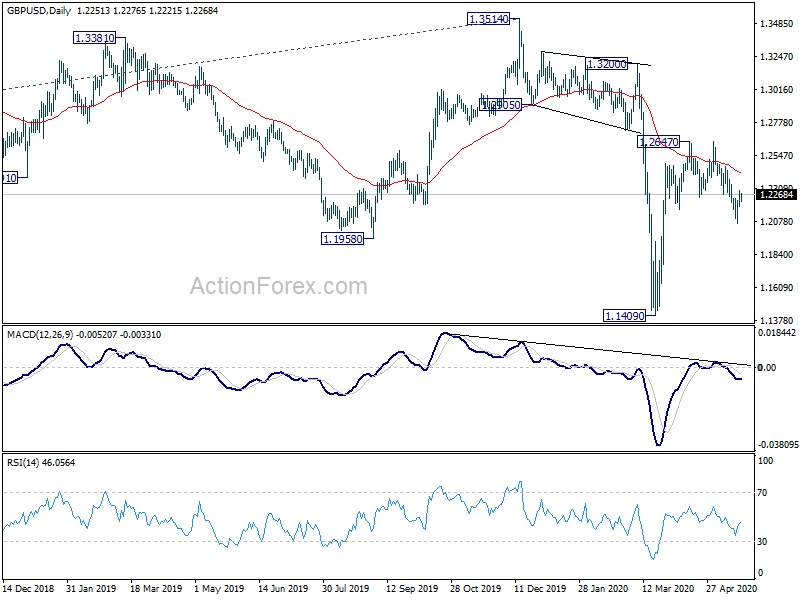

In the bigger picture, while the rebound from 1.1409 is strong, there is no indication of trend reversal yet. Down trend from 2.1161 (2007 high) should still resume sooner or later. Next medium term target will be 61.8% projection of 1.7190 to 1.1946 from 1.3514 at 1.0273. In any case, outlook will remain bearish as long as 1.3514 resistance holds, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Machinery Orders M/M Mar | -0.40% | -7.10% | 2.30% | |

| 00:30 | AUD | Westpac Leading Index M/M Apr | -1.50% | -0.80% | -0.70% | |

| 06:00 | GBP | CPI M/M Apr | -0.20% | -0.10% | 0.00% | |

| 06:00 | GBP | CPI Y/Y Apr | 0.80% | 0.90% | 1.50% | |

| 06:00 | GBP | Core CPI Y/Y Apr | 1.40% | 1.40% | 1.60% | |

| 06:00 | GBP | RPI M/M Apr | 0.00% | 0.10% | 0.20% | |

| 06:00 | GBP | RPI Y/Y Apr | 1.50% | 1.60% | 2.60% | |

| 06:00 | GBP | PPI Input M/M Apr | -5.10% | -3.70% | -3.60% | -3.80% |

| 06:00 | GBP | PPI Input Y/Y Apr | -9.80% | -8.40% | -2.90% | -3.10% |

| 06:00 | GBP | PPI Output M/M Apr | -0.70% | -0.40% | -0.20% | |

| 06:00 | GBP | PPI Output Y/Y Apr | -0.70% | -0.40% | 0.30% | |

| 06:00 | GBP | PPI Output Core M/M Apr | -0.10% | -0.10% | 0.30% | |

| 06:00 | GBP | PPI Output Core Y/Y Apr | 0.60% | 0.60% | 0.90% | |

| 08:00 | EUR | Eurozone Current Account (EUR) Mar | 27.4B | 40.2B | 37.8B | |

| 09:00 | EUR | Eurozone CPI M/M Apr F | 0.30% | 0.30% | 0.50% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Apr F | 0.90% | 0.90% | 0.90% | |

| 09:00 | EUR | Eurozone CPI Y/Y Apr F | 0.30% | 0.40% | 0.40% | |

| 12:30 | CAD | Wholesale Sales M/M Mar | -2.20% | -4.50% | 0.70% | |

| 12:30 | CAD | CPI M/M Apr | -0.70% | -0.40% | -0.60% | |

| 12:30 | CAD | CPI Y/Y Apr | -0.20% | -0.10% | 0.90% | |

| 12:30 | CAD | CPI Common Y/Y Apr | 1.60% | 1.70% | 1.70% | |

| 12:30 | CAD | CPI Median Y/Y Apr | 2.00% | 1.90% | 2.00% | |

| 12:30 | CAD | CPI Trimmed Y/Y Apr | 1.80% | 1.80% | 1.80% | |

| 14:00 | EUR | Eurozone Consumer Confidence May P | -23 | -23 | ||

| 14:30 | USD | Crude Oil Inventories | 1.7M | -0.7M | ||

| 18:00 | USD | FOMC Minutes |

{kind=link}