Markets are generally trading in risk-on mode today. NASDAQ surged to new record highs overnight following solid US job data. Better than expected China services data continue to support sentiment. Yen, Dollar and Euro are set to end the week as the worst performing ones while Sterling and commodity currencies would be the strongest. Technically, there weren’t much new developments though, and breakouts are awaited. But we might need to wait till next week.

In Asia, currently, Nikkei is up 0.26%. Hong Kong HSI is up 0.69%. China Shanghai SSE is up 0.95%. Singapore Strait Times is up 0.62%. Japan 10-year JGB yield is down -0.0034 at 0.032. Overnight, DOW rose 0.36%. S&P 500 rose 0.45%. NASDAQ rose 0.52% to 10207.63, new record. 10-year yield dropped -0.013 to 0.669.

China Caixin PMI services rose to 58.4, employment remained the key problem

China Caixin PMI Services jumped to 58.4 in June, up from 55.0, beat expectation of 53.8. The rate of expectation was the quickest recorded since April 2010. The upturn was widely attributed to the recent easing of coronavirus related restrictions and stronger demand conditions. PMI Composite rose to 55.7, up from 54.5, strongest since November 2010.

Wang Zhe, Senior Economist at Caixin Insight Group said: “Employment remained the key problem. Multiple data showed that work resumption rates at manufacturing and service companies continued rising in June, but it still takes time for the economy to fully recover.

“Therefore, although businesses were optimistic about the economic outlook, they remained cautious about increasing hiring, with employment in both the manufacturing and services sectors shrinking. Addressing the employment problem requires not only macro policies to further promote work resumption, but also more targeted relief measures introduced by governments to tide companies over.”

Australia retail sales rose 16.9% in May on lockdown easing

Australia retail sales rose 16.9% mom in May, revised up from preliminary reading of 16.3% mom. But that’s not enough to recovery the -17.7% mom decline back in April.

“The gradual easing of social distancing regulations, and the re-opening of physical stores, bolstered retail trade in May,” said Ben James, Director of Quarterly Economy Wide Surveys. “Retailers across a range of industries reported high numbers of consumers returning to stores, with some retailers noting levels similar to those seen in December.”

Australia AiG construction rose to 35.5, slower pace of contraction

Australia AiG Performance of Construction Index rose to 35.5 in June, up from 24.9. The data indicates improvement in business conditions in the sector, with pace of contracted eased from the record lows experienced since March. In trend terms, all components improved but stayed below 50. IN particular, activity rose 13.7 pts to 35.1. New orders rose 9.8 pts to 32.8. Employment rose 11.3 pts to 40.4.

UK Gfk consumer confidence rose to -27, remains fragile and volatile

UK Gfk Consumer Confidence rose to -27 in July’s flash reading, up from June’s -30. General Economic Situation over the next 12 months also improved to -42, up from -48.

“After the recent near-historic low of -36 for the Consumer Confidence Barometer last month, we’re seeing some early signs of improvement across most measures for our fourth COVID-19 flash, even though all our core scores remain negative… Economic headwinds could easily blow any recovery off-course with confidence remaining fragile and volatile amid few signs of stability.”

Looking ahead

Eurozone PMI services and UK PMI services are the only features today. US will be on holiday.

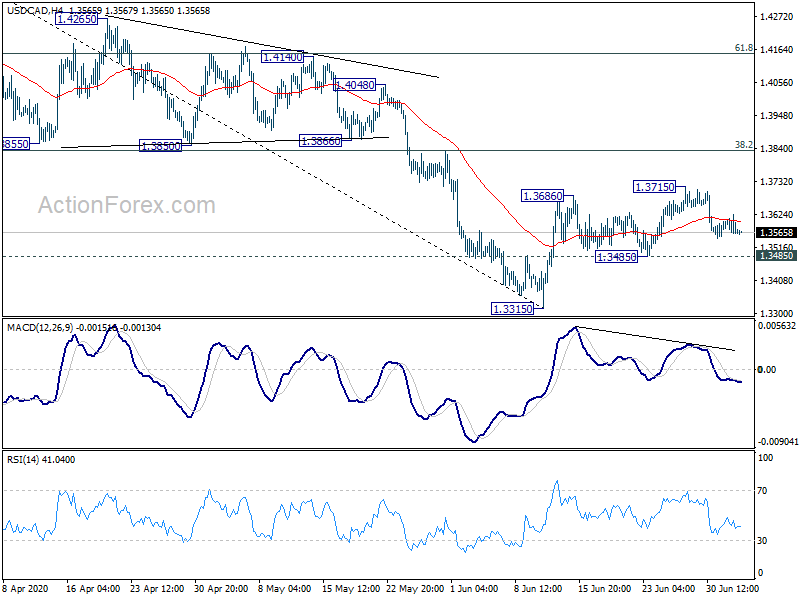

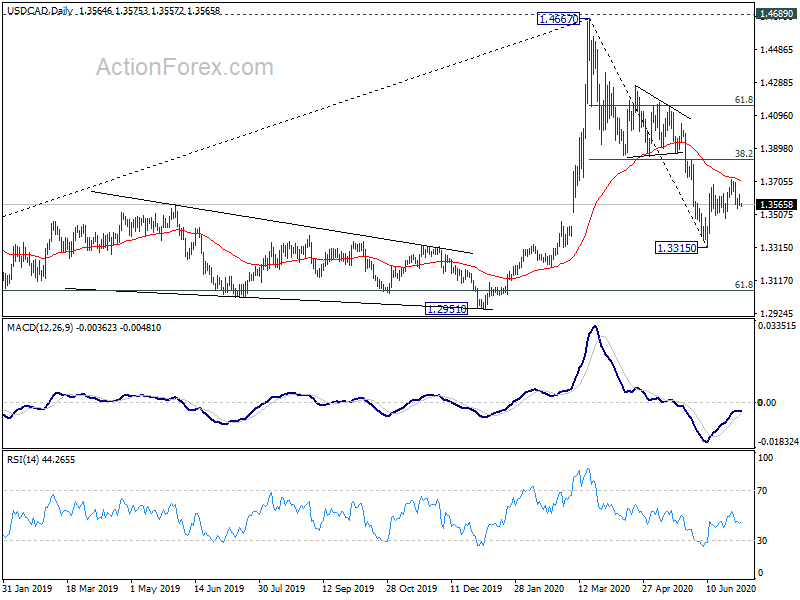

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3543; (P) 1.3583; (R1) 1.3607; More….

No change in USD/CAD’s outlook and intraday bias stays neutral first. Further rise will remain in favor as long as 1.3485 support holds. On the upside, break of 1.3715 will resume the rebound from 1.3315 to 38.2% retracement of 1.4667 to 1.3315 at 1.3831. Nevertheless, break of 1.3485 will argue that the rebound has completed and turn bias back to the downside for retesting 1.3315 low.

In the bigger picture, the rise from 1.2061 (2017 low) could have completed at 1.4667 after failing 1.4689 (2016 high). Fall from 1.4667 could be the third leg of the corrective pattern from 1.4689. Deeper fall is expected to 61.8% retracement at 1.3056 and possibly below. This will now remain the favored case as long as 1.3855 support turned resistance holds. However, sustained break of 1.3855 will turn focus back to 1.4689 key resistance.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Construction Index Jun | 35.5 | 24.9 | ||

| 0:30 | AUD | Retail Sales M/M May | 16.90% | 16.30% | 16.30% | |

| 1:45 | CNY | Caixin Services PMI Jun | 58.4 | 53.8 | 55 | |

| 7:45 | EUR | Italy Services PMI Jun | 46.6 | 28.9 | ||

| 7:50 | EUR | France Services PMI Jun F | 50.3 | 50.3 | ||

| 7:55 | EUR | Germany Services PMI Jun F | 45.8 | 45.8 | ||

| 8:00 | EUR | Eurozone Services PMI Jun F | 47.3 | 47.3 | ||

| 8:30 | GBP | Services PMI Jun F | 47 | 47 |

{kind=link}