European majors are all trading broadly lower today on worsening coronavirus spread and return to lockdowns. Mild risk aversion keeps the Japanese Yen afloat but it’s outperformed slightly by Aussie, after slightly stronger than expected Australian CPI reading. Dollar is mixed for the moment, benefitting little from risk aversion. Traders remain cautious ahead of US elections. Meanwhile, Canadian Dollar also display some weakness as BoC rate decisions is awaited.

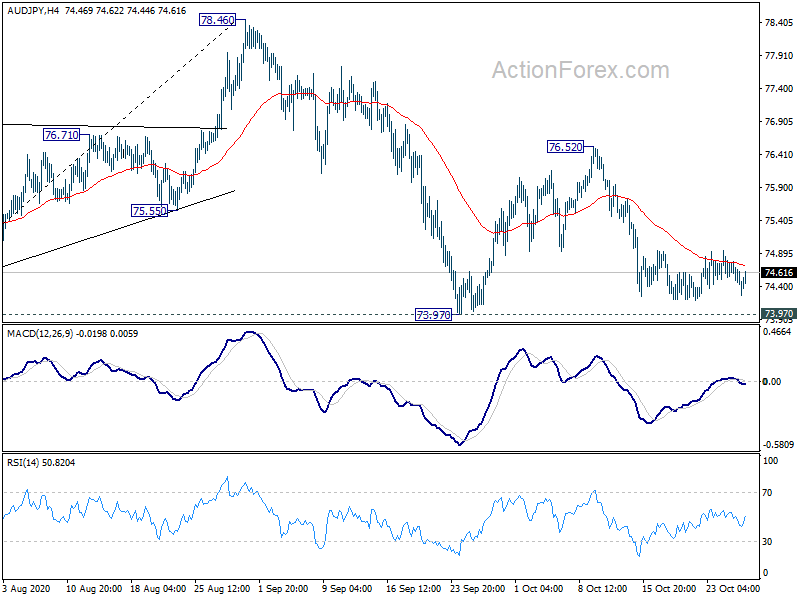

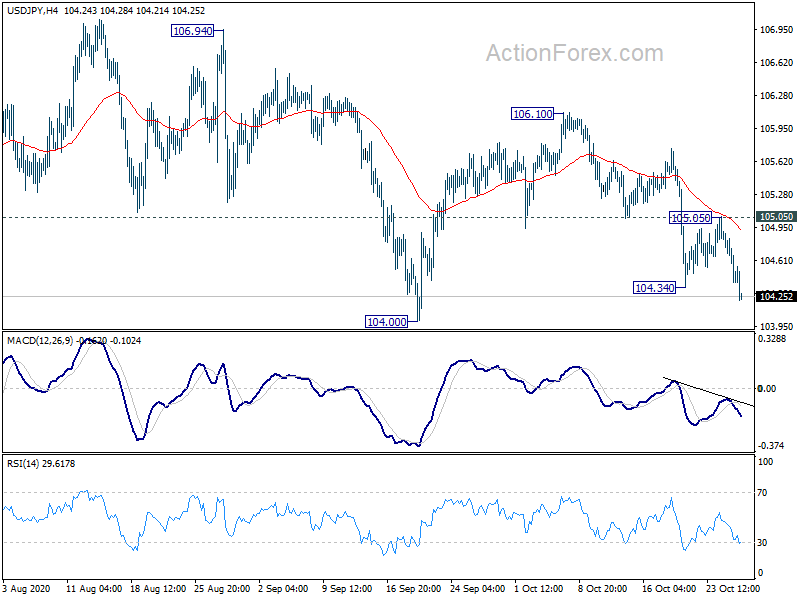

Technically, USD/JPY resumes the fall from 106.10 and it’s now heading to 104.00 low. Break there will resume larger decline from 111.71.EUR/JPY’s break of 123.01 also suggests that decline from 127.07 is resuming through 122.37 support. 135.30 support in GBP/JPY will be a gauge on overall Yen strength. 73.97 support in AUD/JPY will be another.

In Asia, Nikkei is currently down -0.32%. Hong Kong HSI is down -0.13%. China Shanghai SSE is up 0.39%. Singapore Strait Times is down -0.37%. Japan 10-year JGB yield is down -0.0032 at 0.027. Overnight, DOW dropped -0.80%. S&P 500 dropped -0.30%. NASDAQ rose 0.64%. 10-yaer yield dropped -0.0023 to 0.778.

10-yr yield falls as Trump confirms no stimulus deal before election

It’s now clear that there won’t be any stimulus deal before elections. President Donald Trump indicated, “after the election we’ll get the best stimulus package you’ve ever seen.” DOW and S&P 500 closed lower overnight while NASDAQ ended with small gain. Treasury yield also finally moved in tandem with risk sentiments this week. 10-year yield dropped -0.023 to 0.778 overnight, giving up 0.8 handle.

More downside is mildly in favor in TNX for the near term, as investors adjust their risk positions ahead of US elections. We’d anticipating further decline in stocks towards the end of the week, which should theoretically push bonds higher and yields lower. Still for TNX, downside should be contained by 55 day EMA (now at 0.719) unless there are very drastic developments.

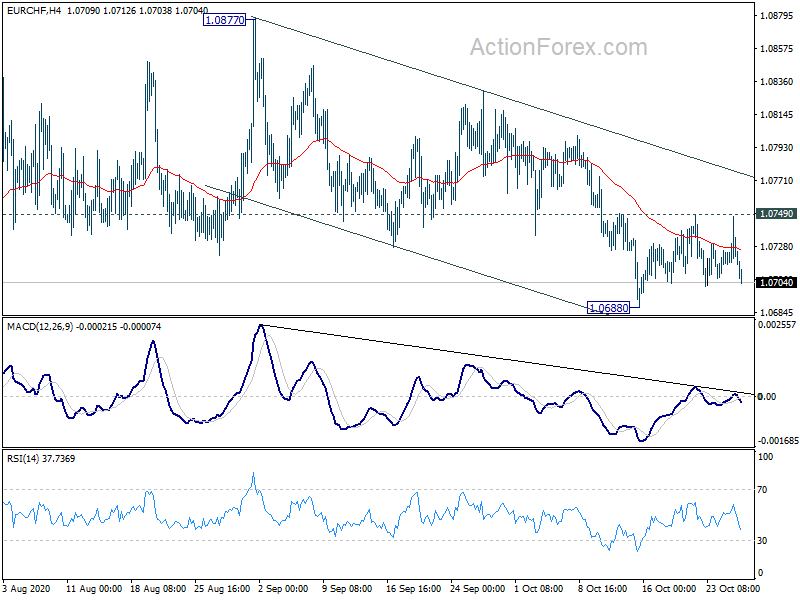

Euro down as France prepares for tougher lockdown, EUR/CHF maintains bearishness

European majors are trading generally lower today on worries over coronavirus spread and lockdowns. France reported 523 deaths on Tuesday, highest since April. UK also reported 367 new deaths, highest since May. Italy and Greece also saw new cases surged to new record.

French President is scheduled to give a televised address on Wednesday evening. It’s uncertain what the speech is about for now. But reports are flowing around that the government is exploring imposition of lockdown from midnight on Thursday. That might be a slightly more flexible one than that in March, as schools could remain open. But options could still include confining people to homes at weekends, closing shops and starting curfews earlier.

EUR/CHF was once again rejected by 1.0749 resistance after yesterday’s rally attempt. Near term bearishness is kept intact as fall from 1.0877 is expected to extend through 1.0688 low, probably rather soon.

Australia CPI rose 1.6% qoq in Q3 as childcare fees returned to pre-pandemic rate

Australia CPI rose 1.6% qoq in Q3, above expectation of 1.5% qoq. But that was insufficient to recover the record -1.9% qoq fall in Q2. Annually, CPI turned positive to 0.7% yoy, matched expectation. RBA trimmed mean CPI came in at 0.4% qoq, 1.2% yoy, above expectation of 0.3% qoq, 1.1% yoy.

Head of Prices Statistics at the ABS Andrew Tomadini said: “In the September quarter child care fees returned to their pre-COVID-19 rate having been free during the June quarter. This was the largest contributor to the CPI rise in the September quarter. Excluding the impact of child care, the CPI would have risen 0.7 per cent.”

Tomadini said: “Annual inflation returned to positive territory rising 0.7 per cent in the September quarter. This followed negative annual inflation for only the third time in the 72-year history of the CPI of 0.3 per cent in the June quarter.”

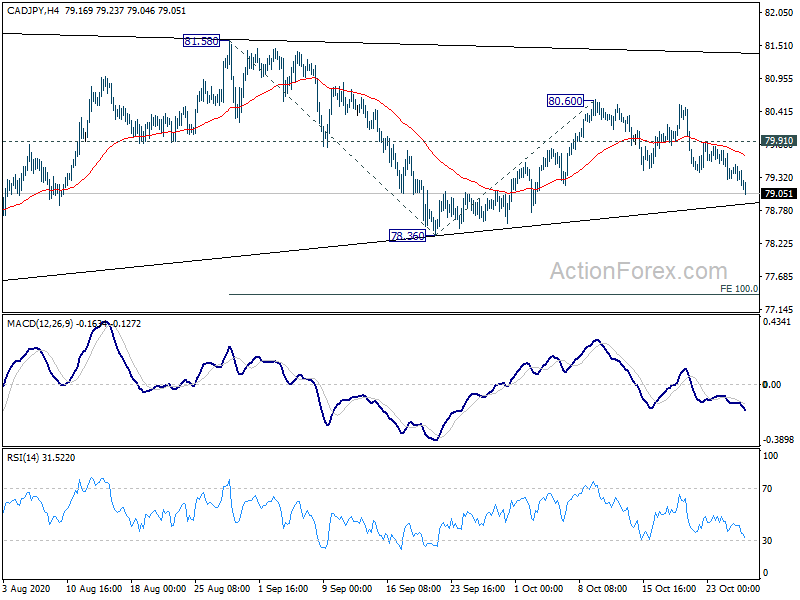

CAD/JPY accelerating downwards as BoC awaited

Canadian dollar is trading mixed in Asian session today, as markets await BoC rate decision. No change in monetary policy is expected as overnight rate will be kept at 0.25%. There might be some adjustments in the asset purchases program but the fine-tuning has already started earlier this month. BoC is also expected to reiterate the pledge to maintain the current accommodative monetary policy stance.

Suggested readings on BoC:

CAD/JPY’s decline from 80.60 is accelerating downward today, partly on overall risk aversion. The current development suggest that CAD/JPY is still staying in the third leg (started at 81.58) of the pattern from 81.91. Focus is immediately on trend line support (now at 78.90). Break there will affirm this view and bring deeper fall through 78.36 support, to 100% projection of 81.58 to 78.36 from 80.60 at 77.38.

Looking ahead

Germany will release import price index in European while Swiss will release ZEW expectations. US will release goods trade balance and wholesales inventories.

USD/JPY Daily Outlook

Daily Pivots: (S1) 104.26; (P) 104.57; (R1) 104.76; More...

USD/JPY’s fall from 106.10 resumes by taking out 104.34. Intraday bias is back on the downside for 104.00 low. Break will resume larger decline from 111.71, towards 101.18 key support. On the upside, break of 105.05 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

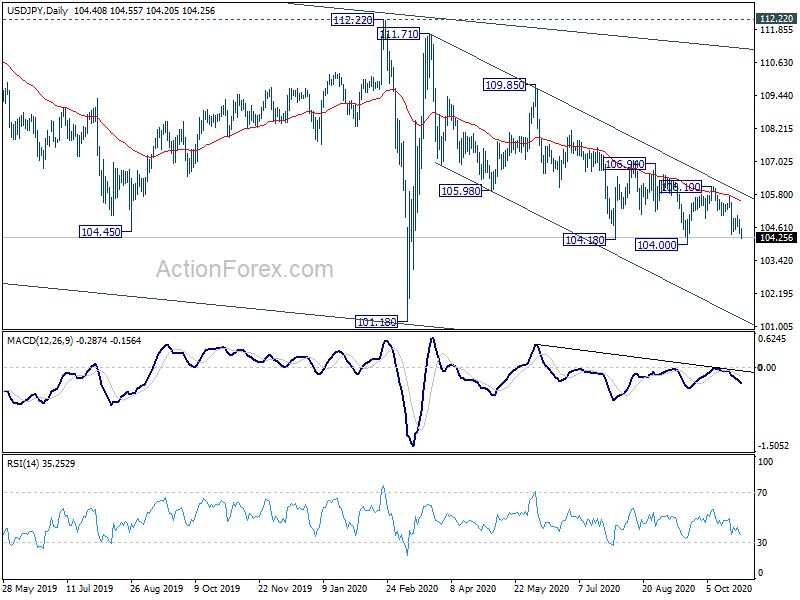

In the bigger picture, USD/JPY is still staying in long term falling channel that started back in 118.65 (Dec. 2016). Hence, there is no clear indication of trend reversal yet. The down trend could still extend through 101.18 low. However, sustained break of 112.22 resistance should confirm completion of the down trend and turn outlook bullish for 118.65 and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:30 | AUD | CPI Q/Q Q3 | 1.60% | 1.50% | -1.90% | |

| 0:30 | AUD | CPI Y/Y Q3 | 0.70% | 0.70% | -0.30% | |

| 0:30 | AUD | RBA Trimmed Mean CPI Q/Q Q3 | 0.40% | 0.30% | -0.10% | |

| 0:30 | AUD | RBA Trimmed Mean CPI Y/Y Q3 | 1.20% | 1.10% | 1.20% | |

| 7:00 | EUR | Germany Import Price Index M/M Sep | -0.30% | 0.10% | ||

| 9:00 | CHF | ZEW Expectations Oct | 26.2 | |||

| 12:30 | USD | Goods Trade Balance (USD) Sep | -85.0B | -82.9B | ||

| 12:30 | USD | Wholesale Inventories Sep P | 0.00% | 0.40% | ||

| 14:00 | CAD | BoC Interest Rate Decision | 0.25% | 0.25% | ||

| 14:30 | USD | Crude Oil Inventories | -1.0M |

{kind=link}