Sterling jumps sharply after BoE indicated that it didn’t want to send a signal to the market on adopting negative rates. Dollar is also firm on overall mixed market sentiments. Thanks to the selloff against both the Pound and the greenback, Euro is currently the worst performing one for the day, trailed closely by the Swiss Franc. As for the week, Kiwi and Dollar the the strongest ones, but Sterling has the potential to over taken them. Euro and Swissy are relatively unlikely to be displaced from the bottom places.

Technically, EUR/GBP’s downside acceleration is a clear bearish development, which could bring it to 0.8670 support soon. GBP/JPY is following to break 144.07 resistance to resume larger up trend. An immediate focus would be 1.3758 resistance in GBP/USD. The pair is staying well indicate near term rising channel despite this week’s retreat. Break of 1.3758 will confirm resumption of recent up trend too. That would confirm the broad based come back of the Pound.

In Europe, currently, FTSE is down -0.11%. DAX is up 0.41%. CAC is up 0.43%. Germany 10-year yield is up 0.012 at -0.451. Earlier in Asia, Nikkei dropped -1.06%. Hong Kong HSI dropped -0.66%. China Shanghai SSE dropped -0.44%. Singapore Strait Times dropped -0.75%. Japan 10-year JGB yield rose 0.0008 to 0.059.

US initial jobless claims dropped to 779k, continuing claims dropped to 4.6m

US initial jobless claims dropped -33k to 779k in the week ending January 30, better than expectation of 850k. Four-week moving average of initial claims dropped -1.25k to 848.3k. Continuing claims dropped -193k to 4592k in the week ending January 23. Four-week moving average of continuing claims dropped -120k to 4882k.

Nonfarm productivity dropped -4.8% in Q4 versus expectation of -1.8%. Unit labor costs rose 6.8% versus expectation of 3.4%.

BoE stands pat, expects GDP to recover rapidly towards pre-Covid levels over 2021

BoE kept monetary policy unchanged as widely expected. Bate Rate is held at 0.10%. Total target stock of asset purchases also stayed at GBP 895B. Both decisions were made with unanimous votes.

The central bank pledged that, “if the outlook for inflation weakens, the Committee stands ready to take whatever additional action is necessary to achieve its remit.” Also, “the Committee does not intend to tighten monetary policy at least until there is clear evidence that significant progress is being made in eliminating spare capacity and achieving the 2% inflation target sustainably.”

Outlook for the economy remains “unusually uncertain”, depending on the “evolution of the pandemic, measures taken to protect public health, and how households, businesses and financial markets respond to these developments.”

In BoE’s economic projections, based on assumption of constant interest rate at 0.1%:

- GDP is seen as growing 5% in 2021 (revised down from November forecast of 7.25%), 7.25% in 2022 (revised up from 6.25%), and 1.25% in 2023 (revised down from 1.75%.

- Unemployment rate was forecast to be at 6.5% in 2021 (revised down from 6.34%), 5% in 2022 (unchanged) and 4.50% in 2023 (revised up from 4.25%).

- CPI inflation was projected to be 2 2% in 2021 (unchanged), 2.25% in 2022 (revised up from 2%), and 2% in 2023 (unchanged).

BoE didn’t want to signal setting negative rate

In the BoE minutes noted, “the Committee was clear that it did not wish to send any signal that it intended to set a negative Bank Rate at some point in the future”. Though, on balance, “it would be appropriate to start the preparations to provide the capability to do so if necessary in the future,””

“The MPC therefore agreed to request that the PRA should engage with PRA-regulated firms to ensure they commence preparations in order to be ready to implement a negative Bank Rate at any point after six months,” the minutes added.

UK PMI construction dropped to 49.2, renewed slide in commercial work

UK PMI Construction dropped sharply to 49.2 in January, down from 54.6, missed expectation of 52.8. Markit noted the renewed down turn in commercial activity. House building recovery lost momentum. But purchase price inflation was highest since June 2018.

Tim Moore, Economics Director at IHS Markit: “The latest survey highlighted that construction companies have become more cautious about the business outlook. Output rebounded quickly after stoppages on site at the start of the pandemic, but hesitancy among clients in January and worries about near-term economic conditions resulted in a dip in growth expectations for the first time in six months.”

Eurozone retail sales rose 2% mom in Dec, EU up 1.4% mom

Eurozone retail sales rose 2.0% mom in December, above expectation of 1.3% mom. The volume of retail trade increased by 5.1% mom for automotive fuels, by 1.9% mom for food, drinks and tobacco and by 1.5% mom for non-food products (within this category textile, clothing and footwear increased by 12.4% mom).

EU retail sales rose 1.4% mom. Among Member States for which data are available, the highest increases in the total retail trade volume were observed in France (22.3% mom), Belgium (15.9% mom) and Ireland (11.4% mom). The largest decreases were registered in the Netherlands (-10.9% mom), Germany (-9.6% mom) and Denmark (-8.0% mom).

From Swiss,. SECO consumer climate dropped to -15 in Q1, down from -13, better than expectation of -16.

Australia NAB Business Confidence rose to 14 in Q4, strong rebound in conditions

Australia NAB Business Confidence rose to 14 in Q4, up from -8. Current Business Conditions rose to 9, up from -5. Next 3 months Business Conditions rose to 19, up from -3. Next 12 months Business Conditions rose from 0 to 24. Capex plans rose from 13 to 31. Looking at some more details, trading condition rose from 1 to 16. Profitability condition rose form -1 to 14. Employment condition rose from -14. to -1.

According to Alan Oster, NAB Group Chief Economist “like many other indicators the survey shows that the economy continued to rebound strongly late in Q4. Optimism in the business sector continued to strengthen as the impacts of severe lockdowns faded”.

“What is even more encouraging is the fact that businesses have seen a strong rebound in actual conditions – particularly in trading conditions and profitability. This likely reflects the huge support provided to the economy by policy makers” said Oster.

Also released, trade surplus widened to AUD 6.79B in December, missed expectation of AUD 9.0B.

New Zealand ANZ business confidence rose to 11.8, no more RBNZ cut expected

New Zealand ANZ Business Confidence rose to 11.8 in February’s preliminary reading, up from December’s 9.4. Own activity outlook rose to 22.3, up from 21.7. Looking at some more details, employment intensions rose to 10.6, up from8.8. Investment intentions improved notably to 17.8, up from 8.56. But export intensions dropped to 6.3, down from 10.3.

ANZ said: “We are forecasting wobble in demand in the first few months of this year as the true cost of the closed border for the tourism industry starts to become apparent. But it’s fair to say there’s not much sign of it yet, with the roaring housing and construction sectors filling the void, albeit fuelled by credit rather than foreign exchange earnings. Further monetary stimulus is looking less necessary by the week, and we no longer expect any more OCR cuts this cycle.”

Also released, building permits rose 4.9% mom in December.

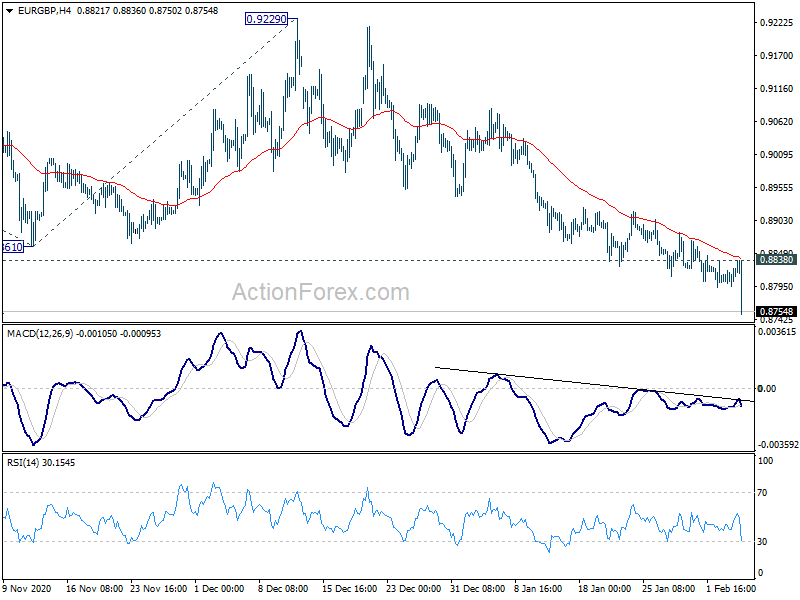

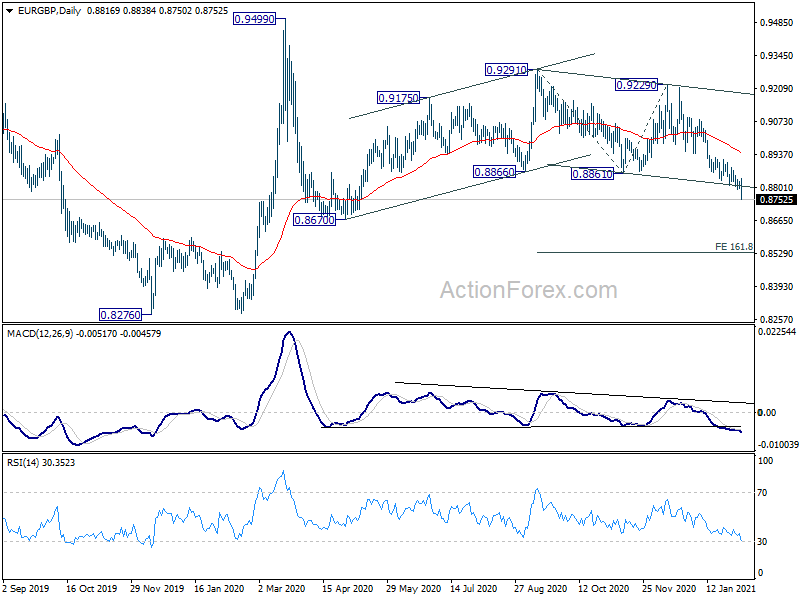

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8805; (P) 0.8815; (R1) 0.8833; More…

EUR/GBP’s decline resumes today and accelerates to as low as 0.8751 so far. Price actions from 0.9291 are seen as the third leg of the corrective pattern from 0.9499. Intraday bias is now on the downside for 0.8670 support first. Break will target 161.8% projection of 0.9291 to 0.8861 from 0.9229 at 0.8533. On the upside, break of 0.8838 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, we’re seeing the price actions from 0.9499 as developing into a corrective pattern. That is, up trend from 0.6935 (2015 low) would resume at a later stage. This will remain the favored case as long as 0.8276 support holds. Decisive break of 0.9499 will target 0.9799 (2008 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Dec | 4.90% | 1.20% | ||

| 00:00 | NZD | ANZ Business Confidence Feb P | 11.8 | -15.6 | 9.4 | |

| 00:30 | AUD | Trade Balance (AUD) Dec | 6.79B | 9.00B | 5.02B | 5.01B |

| 07:00 | CHF | SECO Consumer Climate Q1 | -15 | -16 | -13 | |

| 09:30 | GBP | Construction PMI Jan | 49.2 | 52.8 | 54.6 | |

| 10:00 | EUR | Eurozone Retail Sales M/M Dec | 2.00% | 1.30% | -6.10% | |

| 12:00 | GBP | BoE Interest Rate Decision | 0.10% | 0.10% | 0.10% | |

| 12:00 | GBP | BoE Asset Purchase Facility | 895B | 895B | 895B | |

| 12:00 | GBP | MPC Official Bank Rate Votes | 0–0–9 | 0–0–9 | 0–0–9 | |

| 12:00 | GBP | MPC Asset Purchase Facility Votes | 0–0–9 | 0–0–9 | 0–0–9 | |

| 12:30 | USD | Challenger Job Cuts Jan | 17.40% | 134.50% | ||

| 13:30 | USD | Initial Jobless Claims (Jan 29) | 779K | 850K | 847K | 812K |

| 13:30 | USD | Nonfarm Productivity Q4 P | -4.80% | -1.80% | 4.60% | 5.10% |

| 13:30 | USD | Unit Labor Costs Q4 P | 6.80% | 3.40% | -6.60% | -7.00% |

| 15:00 | USD | Factory Orders M/M Dec | 0.60% | 1.00% | ||

| 15:30 | USD | Natural Gas Storage | -194B | -128B |

{kind=link}