The Asian markets opened the week relatively mixed. Stocks gained initially on US Senate passage of the USD 1.9T stimulus bill. But sentiments are weighed down by concerns of inflation as oil prices jumped. Dollar is firm against Yen, Euro and Swiss Franc and look set to continue with last week’s rally. But the greenback struggles to pick up momentum against commodity currencies, except Kiwi. Gold is struggling to get persistent buying despite recovery attempt.

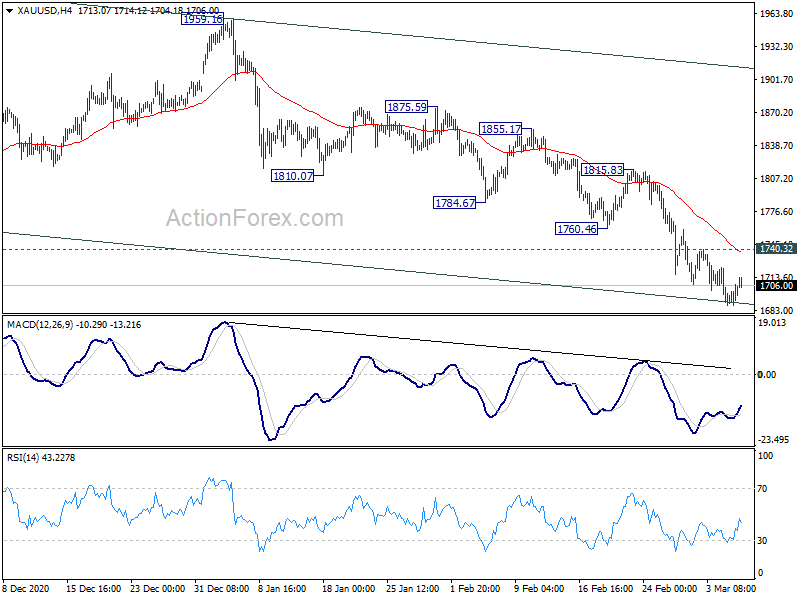

Technically, further rise is still in favor in Dollar, in particular against Euro, Swiss and Yen. Levels to watch include 1.1990 minor resistance in EUR/USD, 0.9192 minor support tin USD/CHF and 107.81 minor support in USD/JPY. Dollar’s rally is not under threat as long as these levels hold. Additionally, more downside is expected in gold as long as 1740.32 minor resistance holds. Another round of selloff could push gold through medium term channel support, while prompt some downside acceleration. That would create a favorable condition for Dollar to extend rally.

In Asia, currently, Nikkei is down -0.39%. Hong Kong HSI is down -1.34%. China Shanghai SSE is down -1.01%. Singapore Strait Times is up 1.78%. Japan 10-year JGB yield is up 0.0183 at 0.115.

China exports and imports jumped in Jan-Feb period, Hong Kong HSI not impressed

Released during the weekend, China’s exports, in USD term, surged 60.6% yoy in the period of Jan-Feb, well above expectations of 38.9% yoy. Imports also rose 22.2% yoy, above expectation of 15.0% yoy. Trade surplus came in at USD 103.3B, much wider than expected USD 60.0B.

The impressive data could be distorted by usual volatility for the January to February period. Additionally, the strong growth partly reflected the low base set in 2020. Nevertheless, some analysts still noted the strong rebound in both global and domestic demand.

Stock traders were not too impressed with the data though. Hong Kong HSI quickly reversed initial gains and it’s currently down -1.6%, or -470 pts, at the time of writing. Immediate focus is now on last week’s low at 28513.13. Break there will extend the correction from 31183.35.

Still, key support lies in 38.2% retracement of 21139.26 to 31183.35 at 27346.50. As long as it holds, the up trend from 21139.26 is still in favor to resume at a later stage.

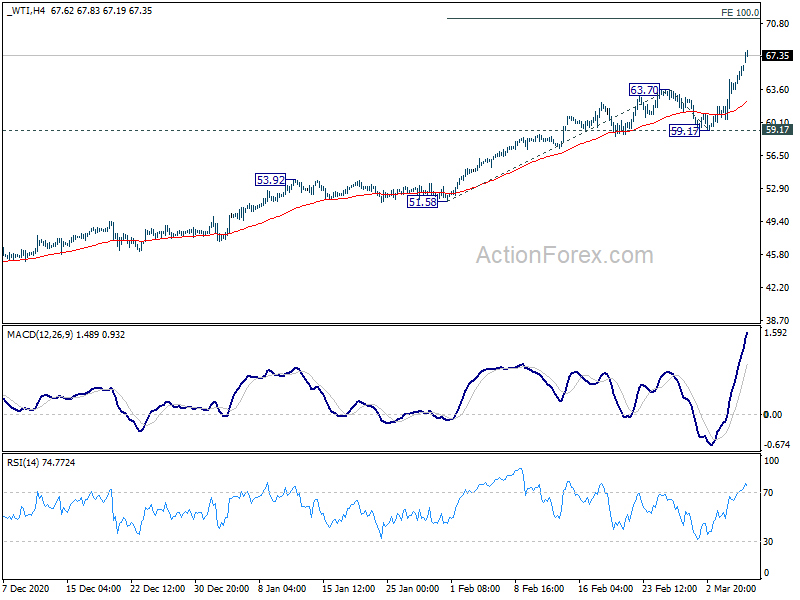

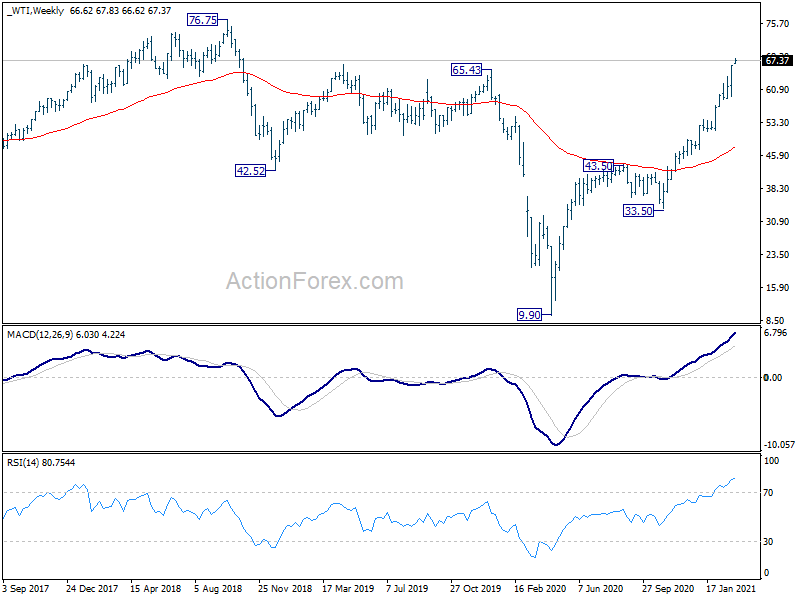

WTI gaps up after Saudi facilities attacked, targets 71.29

Oil price rises today, in response to news of attack on Saudi Arabia’s facilities over the weekend. Energy Ministry confirmed that its largest export terminal at Ras Tanura in the Persian Gulf received drone attack on March 17, allegedly launched by Iranian backed Houthi rebels from Yeomen.

“Such acts of sabotage not only target the Kingdom of Saudi Arabia but also the security and stability of energy supplies to the world, and therefore, the global economy,” the ministry said.

WTI gaps up and hit as high as 67.83. Current up trend is still in acceleration mode. Next term target is 100% projection of 51.58 to 63.70 from 59.17 at 71.29. In any case, near term outlook will stay bullish as long as 59.17 support holds. Also, in the picture, with 65.43 resistance cleared, WTI is looking at 76.75 next.

ECB and BoC to meet, US inflation data watched too

Two central banks will meet this week and ECB is the main focus. Policymakers appeared to be increasingly uncomfortable with rise in global treasury yields. Yet, it’s generally seen that it’s not yet the timing to announce any counter measures. Though, the markets would be very eager to hear hints on the central bank’s actions, probably step up of asset purchase, when necessary.

BoC rate decision will, on the other hand, be more likely a non-event. No change in policy is expected while BoC will likely hold any change in outlook, or forward guidance, until April’s Monetary Policy Report. Friday’s Canadian job data will be more market moving.

On the data front, US inflation data, CPI and PPI, catch some attention. UK will also release GDP and productions. Here are some highlights for the week:

- Monday: Japan current account, leading indicators; Swiss unemployment rate; Germany industrial production; Eurozone Sentix investor confidence.

- Tuesday: New Zealand manufacturing sales, ANZ business confidence; Australia NAB business confidence; Japan GDP final, average cash earnings, household spending, machine tool orders; Germany trade balance; Italy industrial production; Eurozone GDP revision, employment change.

- Wednesday: China CPI, PPI; Australia Westpac consumer sentiment; France industrial production; US CPI; BoC rate decision.

- Thursday: Japan PPI; ECB rate decision; US jobless claims.

- Friday: New Zealand BusinessNZ manufacturing; Japan BSI manufacturing; Germany CPI final; UK GDP, production, trade balance; Eurozone industrial production; Canada employment, capacity utilization, whole sales sales; US PPI, U of Michigan sentiment.

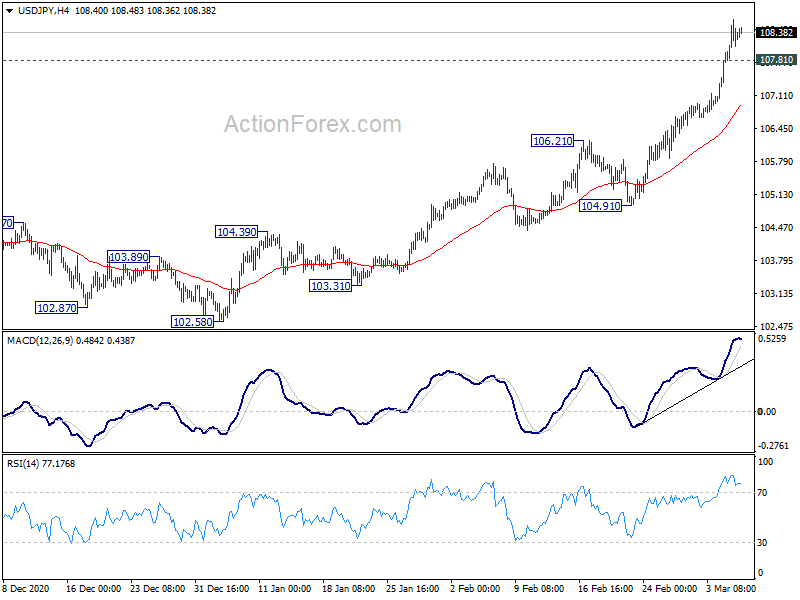

USD/JPY Daily Outlook

Daily Pivots: (S1) 107.93; (P) 108.28; (R1) 108.75; More..

Intraday bias in USD/JPY remains on the upside at this point. Current rally from 102.58 should target long term channel resistance at 110.02 next. Decisive break there will carry larger bullish implications. On the downside, below 107.81 minor support will turn intraday bias neutral and bring consolidations. But outlook will stay bullish as long as 106.21 resistance turned support holds.

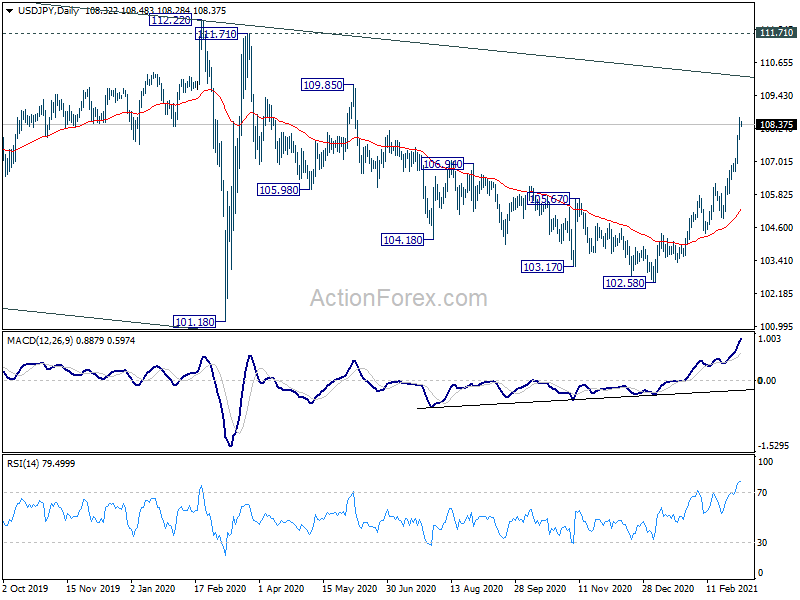

In the bigger picture, focus is now back on long term channel resistance (now at 110.02). Sustained break there will indicate that the down trend from 118.65 (Dec 2016) has completed. Further break of 112.22 resistance will confirm this bullish case and target 118.65 next. However, rejection by the channel resistance will keep medium term outlook bearish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Feb | 6.20% | 6.10% | ||

| 23:50 | JPY | Current Account (JPY) Jan | 1.50T | 2.20T | 2.28T | 2.08T |

| 5:00 | JPY | Leading Economic Index Jan P | 94.4 | 95.3 | ||

| 6:00 | JPY | Eco Watchers Survey: Current Feb | 43.4 | 31.2 | ||

| 6:45 | CHF | Unemployment Rate M/M Feb | 3.60% | 3.50% | ||

| 7:00 | EUR | Germany Industrial Production M/M Jan | -1.40% | 0.00% | ||

| 9:30 | EUR | Eurozone Sentix Investor Confidence Mar | 1 | -0.2 | ||

| 15:00 | USD | Wholesale Inventories Jan F | 1.30% | 1.30% |

{kind=link}