Dollar and Yen trade slightly higher on mild risk-off sentiment in Asia. Australian and Canadian Dollar are the weaker ones for the time being. But overall, most major pairs and crosses are stuck in range. Except that, some extra strengthen is seen in Kiwi against Aussie. Kiwi could be ready for a ride ahead of RBNZ rate decision this week.

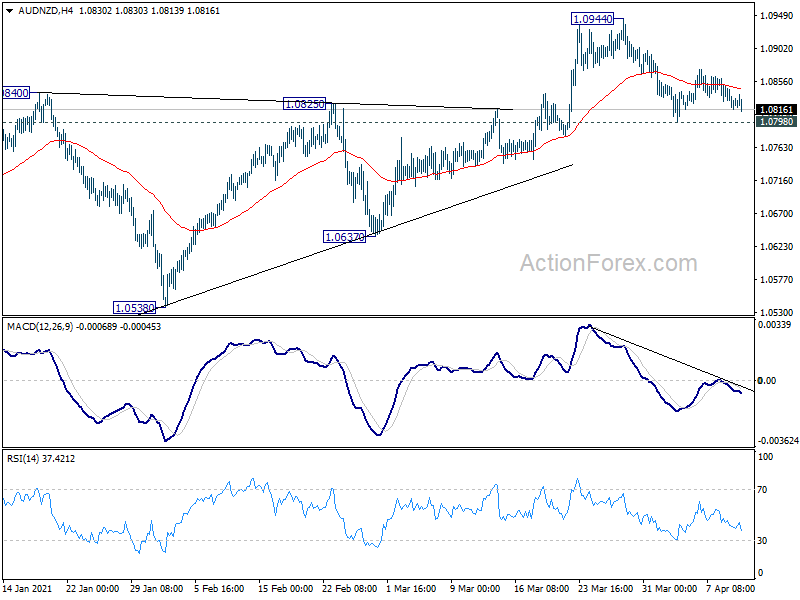

Technically, AUD/NZD’s recovery should have completed after failing to sustain above 4 hour 55 EMA. Focus is back on 1.0798 temporary temporary low. Break there will resume the correction from 1.0944. Such development could be accompanied by break of 0.7587 minor support to retest 0.7530 low.

In Asia, currently, Nikkei is down -0.56%. Hong Kong HSI is down -1.06%. China Shanghai SSE is down -0.81%. Singapore Strait Times is down -0.45%. Japan 10-year JGB yield is down -0.0012 at 0.104, staying above 0.1 handle.

Fed Powell: H2 going to be very strong but risks are still out there

In the CBS’ 60 Minutes aired on Sunday, Fed Chair Jerome Powell said “we feel like we’re at a place where the economy’s about to start growing much more quickly and job creation coming in much more quickly”. He added that the growth in H2 is “going to be very strong”.

“There really are risks out there,” he added. “And the principal one just is that we will reopen too quickly, people will too quickly return to their old practices, and we’ll see another spike in cases.” But even in that case, any spike in cases wouldn’t be as disastrous as prior ones, thanks to vaccinations. The economy will still “move ahead more quickly to the extent we keep the spread of COVID under control.”

The time to for the administration to reduce the budget deficit is “when the economy is strong and we’re fully recovered and people are working and taxes are rolling in,” he said. “The time to do that is not now.”

ECB: Panetta: Waiting on inflation will even be more costly

Fabio Panetta told Spanish newspaper El Pais in an interview published on Sunday, “the ECB has failed to reach its aim for too many years already.” And, “we cannot be satisfied with inflation at 1.2% in 2022 and 1.4% in 2023. The argument that we could extend the horizon to meet the aim is not a convincing one.”

“Waiting will be even more costly,” Panetta added. “It would make it more difficult to re-anchor inflation expectations and we would risk a permanent reduction of economic potential.”

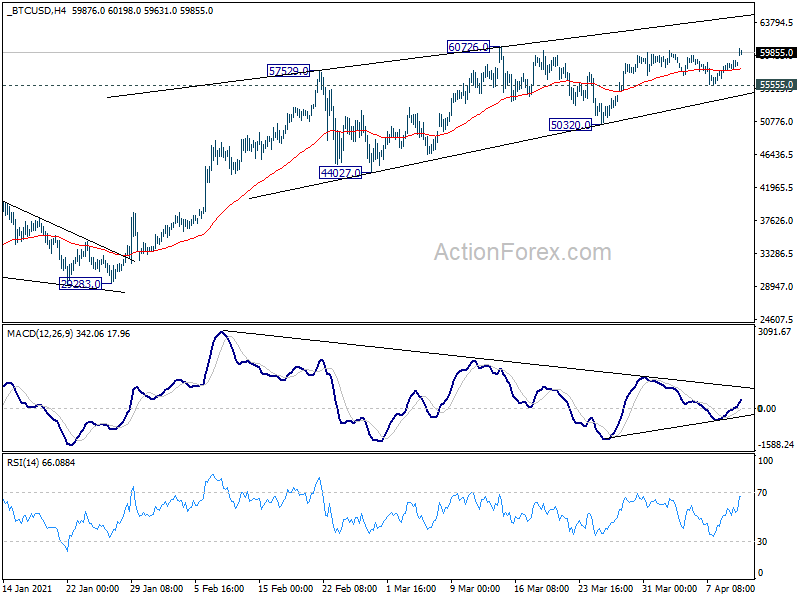

Bitcoin back pressing 60k on strong open, aiming for new record

Bitcoin gapped higher as the week starts, breaking through last week’s high and it’s back pressing 60k handle. Recent up trend is still in progress and bitcoin could break through record high at 60726 any time soon.

Yet, we’d maintain that it has been losing upside momentum since February, as seen in 4 hour MACD. Also, current rise from 50320 is seen as the fifth leg of the terminal triangle that started 29283. Hence the break to new record high should be relatively brief, and a sizeable correction should follow.

Nevertheless, in case of a pull back, break of 55555 support is needed to confirm short term topping first. Otherwise, outlook will remain bullish and risk will stay on the upside.

RBNZ to stand pat, lots of data to watch

RBNZ is generally expected to keep interest rate unchanged at 0.25% this week. The central will also reiterate the guidance that policy will be on hold for some time to come. Overall, the announce would likely be a non-event. Economic data to be released are more noteworthy. There will be sentiment indicators like Germany ZEW, inflation data like US CPI and, growth data like UK and China GDP. Here are some highlights for the week:

- Monday: Japan PPI, machine tool orders; Eurozone retail sales; BoC business outlook survey.

- Tuesday: Japan M2; Australia NAB business confidence; China trade balance; UK goods trade balance, productions, GDP; German ZEW economic sentiment; industrial production; US CPI.

- Wednesday: Japan machine orders; Australia Westpac consumer sentiment; RBNZ rate decision; Eurozone industrial production; US import prices.

- Thursday: Australia MI inflation expectations, employment; Germany CPI final; Canada ADP employment, manufacturing sales; US retail sales, Philly Fed manufacturing index, jobless claims, Empire State manufacturing index, industrial production, business inventories, NABH housing market index.

- Friday: New Zealand BusinessNZ manufacturing index, China GDP, fixed asset investment, industrial production, retail sales; Swiss PPI; Eurozone CPI final, trade balance; Canada housing starts, wholesale sales, foreign securities purchases; US housing starts, building permits, U of Michigan consumer sentiment.

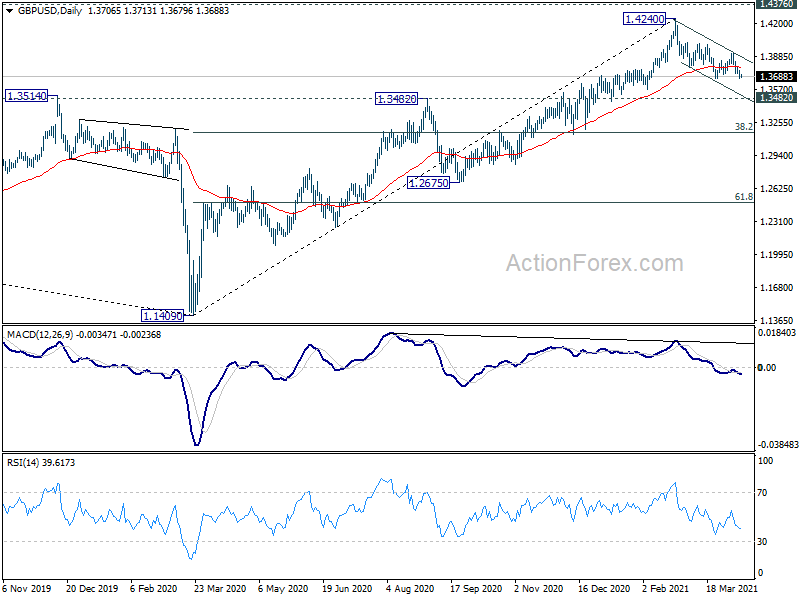

GBP/USD Daily Outlook

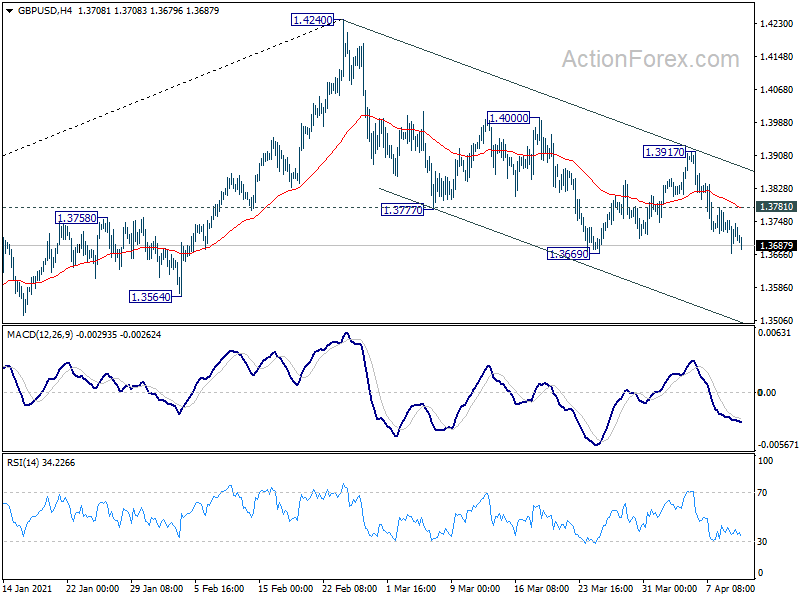

Daily Pivots: (S1) 1.3665; (P) 1.3708; (R1) 1.3746; More…

Intraday bias sin GBP/USD stays mildly on the downside. Break of 1.3669 will resume the correction from 1.4240. Next target is 1.3482 key resistance turned support On the upside, above 1.3781 minor resistance will turn bias neutral first. But risk will stay on the downside as long as 1.3917 resistance holds.

In the bigger picture, as long as 1.3482 resistance turned support holds, up trend from 1.1409 should still continue. Decisive break of 1.4376 resistance will carry larger bullish implications and target 38.2% retracement of 2.1161 (2007 high) to 1.1409 (2020 low) at 1.5134. However, firm break of 1.3482 support will argue that the rise from 1.1409 has completed and bring deeper fall to 1.2675 support and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Mar | 6.30% | 6.30% | 6.20% | |

| 23:50 | JPY | PPI Y/Y Mar | 1.00% | 0.50% | -0.70% | -0.60% |

| 6:00 | JPY | Machine Tool Orders Y/Y Mar | 36.70% | |||

| 9:00 | EUR | Eurozone Retail Sales M/M Feb | 1.40% | -5.90% | ||

| 14:30 | CAD | BoC Business Outlook Survey |

{kind=link}