The financial markets are generally steady today, as European indices are mixed in tight range. US futures point to slightly higher open, as S&P 500 could extend record run. Gold and oil are both still range bound. In the currency markets, Aussie and Kiwi continue to trade as the strongest ones for today, followed by Euro. Canadian Dollar, Dollar, and Swiss Franc are the weakest ones.

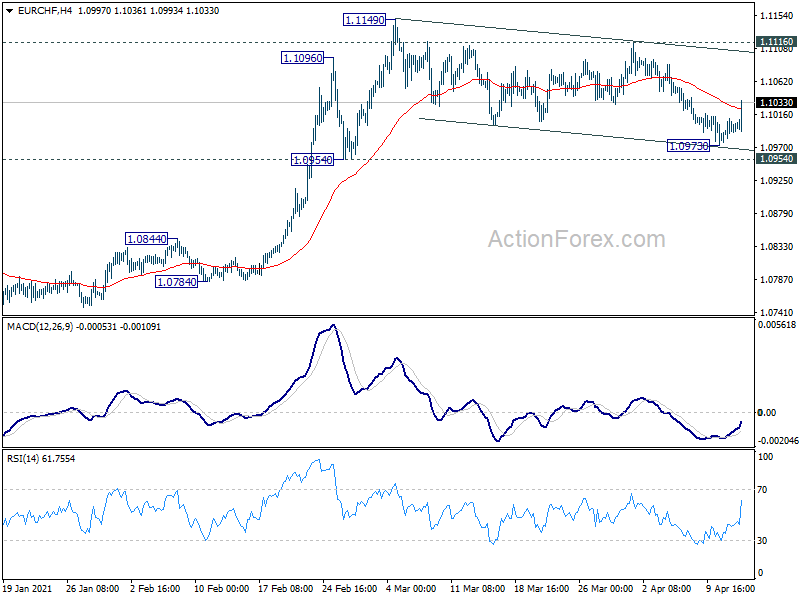

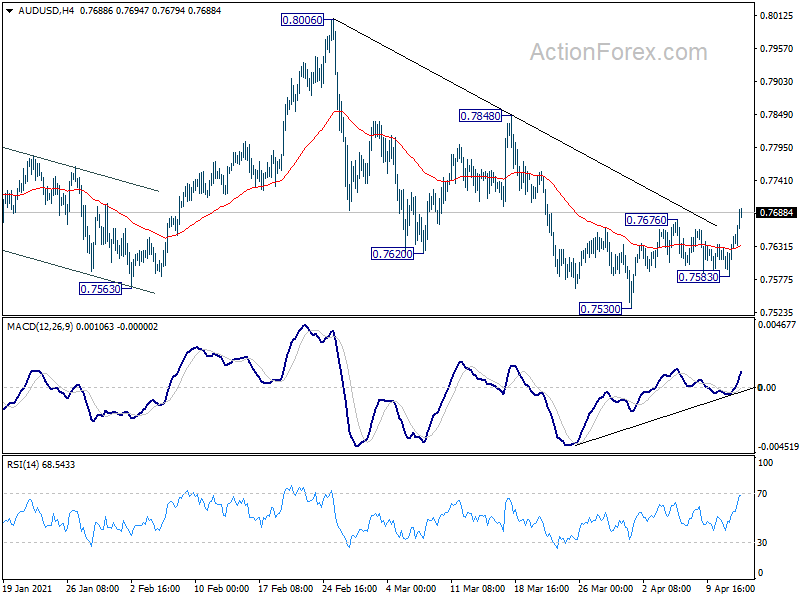

Technically, AUD/USD’s break of 0.7676 minor resistance suggests resumption of rebound from 0.7530. That affirms Dollar’s general weakness. Though, we’d like to se USD/CAD breaking through 1.2501 minor support, as well as GBP/USD breaking 1.3917 resistance to give us more confidence. On the other hand, Swiss Franc could be starting to reverse, in particular against Euro. We’ll see if a strong rebound in EUR/CHF would result in EUR/USD breaking through 1.1988 resistance, or USD/CHF breaking through 0.9258 minor resistance.

In Europe, currently, FTSE is up 0.30%. DAX is down -0.15%. CAC is up 0.40%. Germany 10-year yield is down -0.001 at -0.289. Earlier in Asia, Nikkei dropped -0.44%. Hong Kong HSI rose 1.42%. China Shanghai SSE rose 0.60%. Singapore Strait Times dropped -0.27%. Japan 10-year JGB yield dropped -0.0134 to 0.090.

Eurozone industrial production dropped -1.0% mom in Feb, EU down -0.9% mom

Eurozone industrial production dropped -1.0% mom in February, worse than expectation of 0.5% mom rise. Production of capital goods fell by -1.9%, energy by -1.2%, durable consumer goods by -1.1%, intermediate goods by 0.7% and non-durable consumer goods by -0.1%.

EU industrial production dropped -0.9% mom. Among Member States for which data are available, the largest decreases were registered in France (-4.8%), Malta (-3.8%) and Greece (-2.5%). The highest increases were observed in Hungary (+4.8%), Ireland (+4.2%) and Croatia (+3.4%).

ECB de Guindos: All stakeholders must avoid cliff effects from premature scaling back of policies

ECB Vice President Luis de Guindos said in a speech that “at the moment, risks from the early withdrawal of policies are higher than the risks associated with keeping support measures in place.”

He also surged that “all stakeholders”, partly fiscal ones, “must keep complementing our accommodative monetary stance”. For a timely recovery in Europe, “we have to avoid any cliff effects from the premature scaling back of these policies”.

Looking ahead, “completing the banking union and deepening the capital markets union are the best policy tools we have at our disposal to ensure that the EU financial sector is conducive to fostering long-term growth and that it embraces all the opportunities offered by the digital transformation and the transition to green technologies.”

ECB de Galhau: We still have quartet of instruments even after PEPP exit

ECB Governing Council member Francois Villeroy de Galhau said, “our monetary policy should remain accommodative for the years to come, but our combination of instruments could evolve.”

“We could also have net asset purchases with our other program, APP, possibly somewhat adapted, and we would have the full range of what I call the quartet of our instruments.” The tools include the APP, negative interest rates, liquidity measures such as TLTROs, and forward guidance.

The combinations could facilitate a “possible exit of the PEPP by March 2022. Though, he emphasized, “we’re not yet there. We have time to judge.”

BoJ Kuroda: Recovery sustains as business sentiments improves for three straight quarters

BoJ Governor Haruhiko Kuroda said “while Japan’s economy remains in a severe state due to the pandemic’s impact, it is picking up as a trend”. As a whole, “recovery is being sustained as business sentiment improves for three straight quarters.”

Still, Kuroda warned that “downside risks remain high”. BoJ will continue to “patiently” maintain its powerful monetary easing to achieve the 2% inflation target.

RBNZ stands pat, outlook remains highly uncertain

RBNZ left stimulatory monetary policy unchanged as widely expected, with OCR at 0.25% and Large Scale Asset Purchase and Funding for Lending program unchanged. It maintained that to meet the requirements of sustainable 2% inflation and maximum employment will “necessitate considerable time and patience”. The committee is also “prepared to lower the OCR if required”.

The medium-term growth outlook was “similar” to the scenario presented in the February statement. Outlook remains “highly uncertain, determined in large part by both health-related restrictions, and business and consumer confidence.” The would be some temporary factors for near-term price pressures, including global supply chain disruptions and higher oil prices. But medium-term inflation and employment will “likely remain below its remit targets in the absence of prolonged monetary stimulus.”

Australia Westpac consumer sentiment rose to 118.8, highest since 2010

Australia Westpac consumer sentiment rose 6.2% to 118.8 in April, up from 111.8. it’s the highest level since August 2010, “when the Australia’s post-GFC rebound and mining boom were in full swing”. The survey continues to signal that “consumer will be the key driver of above-trend growth in 2021”.

Westpac expects RBA to maintain currency policy settings on May 4. Markets will focus on the new economic projections to be released with the SoMP on May 7. Overall, the forecasts would be consistent with the policy guidance that, “it will still be some time – 2024 at the earliest – before the Bank expects to achieve its full employment and inflation targets.”

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.7604; (P) 0.7626; (R1) 0.7667; More…

AUD/USD’s break of 0.7676 resistance indicates resumption of rebound from 0.7530. Intraday bias is back on the upside for 0.7848 resistance. Firm break there should completion of the corrective fall from 0.8006. For now, risk will stay mildly on the upside as long as 0.7583 minor support holds, in case of retreat.

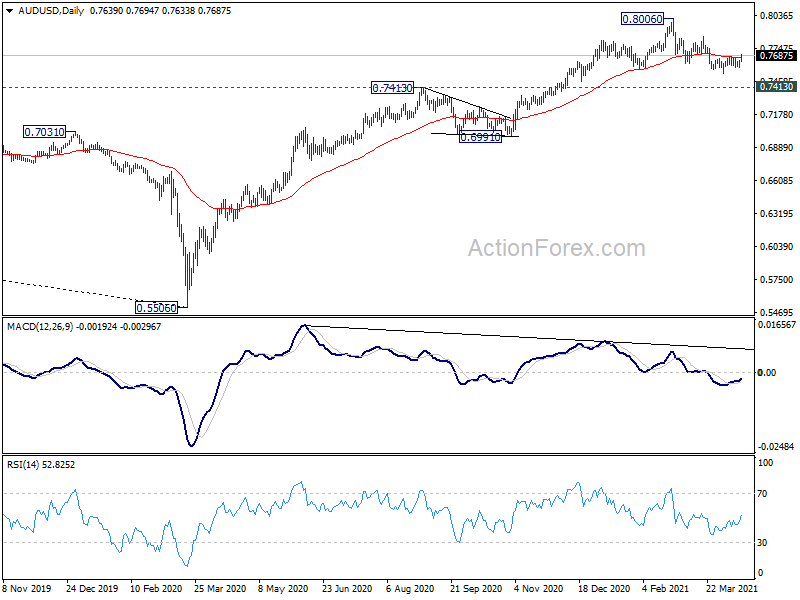

In the bigger picture, whole down trend from 1.1079 (2001 high) should have completed at 0.5506 (2020 low) already. Rise from 0.5506 could either be the start of a long term up trend, or a corrective rise. Reactions to 0.8135 key resistance will reveal which case it is. But in any case, medium term rally is expected to continue as long as 0.7413 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Machinery Orders M/M Feb | -8.50% | 2.80% | -4.50% | |

| 00:30 | AUD | Westpac Consumer Confidence Apr | 6.20% | 2.60% | ||

| 01:00 | NZD | RBNZ Rate Decision | 0.25% | 0.25% | 0.25% | |

| 09:00 | EUR | Eurozone Industrial Production M/M Feb | -1.00% | 0.50% | 0.80% | |

| 12:30 | USD | Import Price Index M/M Mar | 1.20% | 0.90% | 1.30% | |

| 14:30 | USD | Crude Oil Inventories | -2.4M | -3.5M | ||

| 18:00 | USD | Fed’s Beige Book |

{kind=link}