Dollar is back under pressure again as risk-on sentiments seem to be back as indicated by US futures. Swiss Franc and Euro are not too far away, as both turn softer, while Yen is following. On the other hand, New Zealand Dollar continues to lead the way after RBNZ’s halt of asset purchase program. Canadian Dollar is also firm as focus turns to BoC policy decision, at which further tapering should be announced.

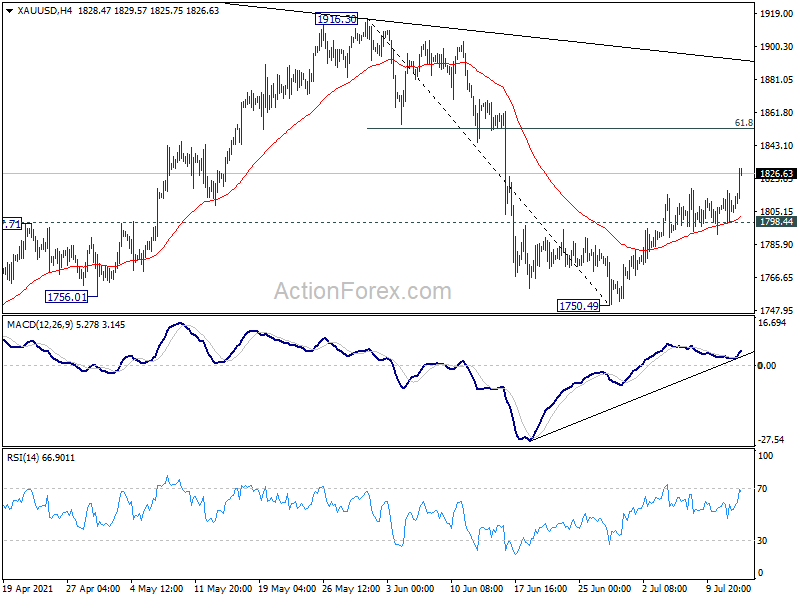

Technically, Gold’s upside breakout suggests that rebound from 1750.49 has resumed. Notable support was seen from 4 hour 55 EMA, which is a near term bullish sign. Further rise is expected as long as 1798.44 support holds, targeting 61.8% retracement of 1916.30 to 1750.49 at 1852.96. Sustained break there will pave the way to 1916.30 key structural resistance. Such development could be an indication of more downside in Dollar ahead.

In Europe, at the time of writing, FTSE is down -0.38%. DAX is up 0.04%. CAC is down -0.07%. Germany 10-year yield is down -0.0145 at -0.308. Earlier in Asia, Nikkei dropped -0.38%. Hong Kong HSI dropped -0.63%. China Shanghai SSE dropped -1.07%. Singapore Strait Times dropped -0.43%. Japan 10-year JGB yield dropped -0.0047 to 0.021.

US PPI accelerated to new record of 7.3% yoy

US PPI for final demand rose 1.0% mom in June, above expectation of 0.5% mom. For the 12 month period, PPI accelerated to 7.3% yoy, up from 6.6% yoy, above expectation of 7.1% yoy. That’s the largest annual rise since 12-month data were first calculated in November 2021. PPI core came in at 1.0% mom, 5.6% yoy, above expectation of 0.4% mom, 5.3% yoy.

From Canada, manufacturing sales dropped -0.6% mom in May, better than expectation of -1.1% mom.

BoE Cunliffe not expecting smooth reopening, but with bumps in way

BoE Deputy Governor Jon Cunliffe told CNBC, “one shouldn’t expect the reopening of the economy to be smooth, this is not something that you can just close down and reopen without bumps in the way.” He admitted, “we’re seeing a surge in demand. We’re seeing some constrictions in supply that’s driving inflation.”

“Are these factors that the economy will then adjust, supply will recover and adjust, and demand after the initial burst will cool off, or is this something more persistent that will become embedded in people’s expectations?” he questioned. But he emphasized that BoC will try to analyze the situation as the economy returns tor normal.

UK CPI jumped to 2.5% yoy in Jun, highest since Aug 2018

UK CPI surged to 2.5% yoy in June, up from 2.1% yoy, above expectation of 2.2% yoy. That’s also the highest reading since August 2018. Core CPI also rose to 2.3% yoy, up from 2.0% yoy, above expectation of 2.0% yoy. RPI rose to 3.9% yoy, up from 3.3% yoy, above expectation of 3.4% yoy.

Also released, PPI input came in at -0.1% mom, 9.1% yoy in June, versus expectation of 1.2% mom, 10.8% yoy. PPI output was at 0.4% mom, 0.6% yoy, versus expectation of 4.3% mom, 4.8% yoy. PPI core output was at 0.3% mom, 2.7% yoy, versus expectation of 0.3% mom, 3.2% yoy.

Eurozone industrial production dropped -1.0% mom in May, EU down -0.9% mom

Eurozone industrial production dropped -1.0% mom in May, much worse than expectation of 0.2% mom rise. Production of non-durable consumer goods fell by -2.3%, energy by -1.9%, capital goods by -1.6% and intermediate goods by -0.2%, while production of durable consumer goods rose by 1.6%.

EU industrial production dropped -0.9% mom. Among Member States for which data are available, the largest decreases were registered in Romania (-8.5%), Greece (-4.7%) and Ireland (-4.6%). The highest increases were observed in Lithuania (+7.7%), Hungary (+3.4%) and Finland (+2.2%).

Australia Westpac consumer sentiment rose to 108.8 despite NSW lockdown

Australia Westpac-Melbourne Institute Consumer Sentiment rose 1.5% to 108.8 in July, up from 107.2. Confidence has “held up overall” despite a sharp fall in New South Wales, as Victoria and Western Australia recorded strong “bounce-backs”.

Westpac said RBA is not expected announce any change at August 3 meeting. The focus would mainly be on the Statement on Monetary Policy on August 6. RBA would have a few more weeks to assess the impact of the lockdown in Sydney.

RBNZ halts asset purchases

RBNZ surprised the markets as it announced to halt the additional asset purchases under the Large Scale Asset Purchase (LSAP) program by July 23. Meanwhile, OCR was kept unchanged at 0.25%. and the Funding for Lending Program was maintained. The Committee agreed that “the level of monetary stimulus could now be reduced to minimise the risk of not meeting its mandate.”

The central bank said the economy “remains robust” despite ongoing impact from international border restrictions. Aggregate economic activity is already “above its pre-COVID-19 level”. It expected “near-term spikes” in headline CPI in Q2 and Q3, reflecting “one-off” or “temporary” factors. In the absence of any further significant shocks, “more persistent consumer price inflation pressure is expected to build over time due to rising domestic capacity pressures and growing labour shortages”.

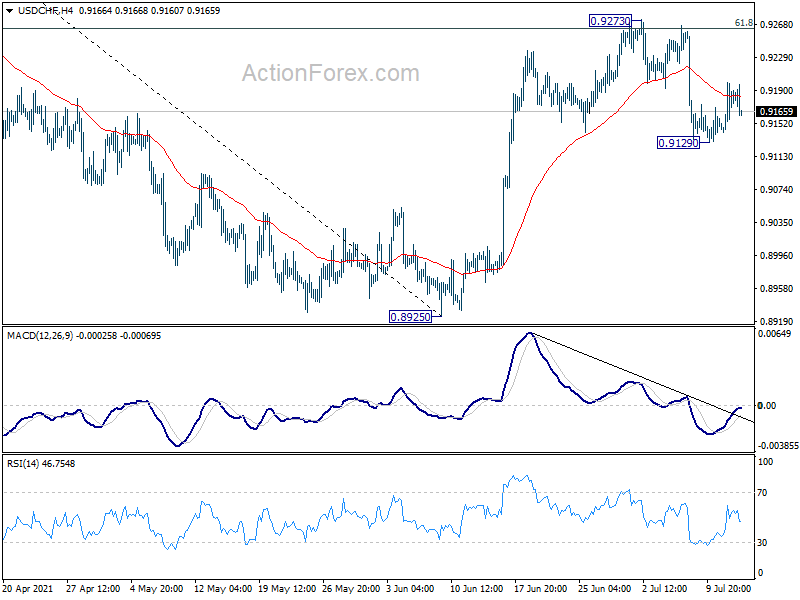

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9153; (P) 0.9177; (R1) 0.9211; More….

USD/CHF weakens after failing to sustain above 4 hour 55 EMA, but downside is contained well above 0.9129 support. Intraday bias remains neutral first. Risk is mildly on the downside with 0.9273 resistance intact. On the downside, sustained trading below 55 day EMA (now at 0.9126) will affirm the case that rebound from 0.8925 has completed at 0.9273. Deeper fall would then be seen back to retest 0.8925 low. On the upside though, break of 0.9273 and sustained trading above 61.8% retracement of 0.9471 to 0.8925 at 0.9262 will target 0.9471 resistance next.

In the bigger picture, medium term outlook is currently neutral with focus on 0.9471 resistance. Sustained break there will indicate completion of whole decline from 1.0342 (2016 high). Medium term outlook will be turned bullish for a test on 1.0342 high. But, rejection by 0.9471 again will revive bearishness for another fall through 0.8756 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Westpac Consumer Confidence Jul | 1.50% | -5.20% | ||

| 02:00 | NZD | RBNZ Interest Rate Decision | 0.25% | 0.25% | 0.25% | |

| 04:30 | JPY | Industrial Production M/M May F | -6.50% | -5.90% | -5.90% | |

| 06:00 | GBP | CPI M/M Jun | 0.50% | 0.20% | 0.60% | |

| 06:00 | GBP | CPI Y/Y Jun | 2.50% | 2.20% | 2.10% | |

| 06:00 | GBP | Core CPI Y/Y Jun | 2.30% | 2.00% | 2.00% | |

| 06:00 | GBP | RPI M/M Jun | 0.70% | 0.30% | 0.30% | |

| 06:00 | GBP | RPI Y/Y Jun | 3.90% | 3.40% | 3.30% | |

| 06:00 | GBP | PPI Input M/M Jun | -0.10% | 1.20% | 1.10% | 1.20% |

| 06:00 | GBP | PPI Input Y/Y Jun | 9.10% | 10.80% | 10.70% | 10.40% |

| 06:00 | GBP | PPI Output M/M Jun | 0.40% | 0.60% | 0.50% | 0.80% |

| 06:00 | GBP | PPI Output Y/Y Jun | 4.30% | 4.80% | 4.60% | 4.40% |

| 06:00 | GBP | PPI Core Output M/M Jun | 0.30% | 0.30% | 0.40% | 0.70% |

| 06:00 | GBP | PPI Core Output Y/Y Jun | 2.70% | 3.20% | 2.70% | 2.30% |

| 09:00 | EUR | Eurozone Industrial Production M/M May | -1.00% | 0.20% | 0.80% | 0.60% |

| 12:30 | USD | PPI M/M Jun | 1.00% | 0.50% | 0.80% | |

| 12:30 | USD | PPI Y/Y Jun | 7.30% | 7.10% | 6.60% | |

| 12:30 | USD | PPI Core M/M Jun | 1.00% | 0.40% | 0.70% | |

| 12:30 | USD | PPI Core Y/Y Jun | 5.60% | 5.30% | 4.80% | |

| 12:30 | CAD | Manufacturing Sales M/M May | -0.60% | -1.10% | -2.10% | |

| 14:00 | CAD | BoC Interest Rate Decision | 0.25% | 0.25% | ||

| 14:30 | USD | Crude Oil Inventories | -4.3M | -6.9M | ||

| 15:15 | CAD | BoC Press Conference | ||||

| 18:00 | USD | Fed’s Beige Book |

{kind=link}