Canadian Dollar rises mildly in early US session after stronger than expected consumer inflation reading. But strength of the Loonie is related limited. It remains one of the worst performing for the week, just next to Australian and New Zealand Dollar. Aussie continues to be weighed down by lockdowns while Kiwi is soft after RBNZ stood pat. Nevertheless, Swiss Franc, Yen and Dollar are just digesting this week’s gains, awaiting the next move.

Technically, the next move in the forex markets could be triggered by development in stocks. NASDAQ would try to draw support from 55 day EMA (now at 14467.02) again, to resume long term up trend. In that case, Swiss Franc, Yen and Dollar could turn softer. However, sustained break of the EMA will be an early sign of larger reversal and put 14k handle at risk. We could then see buying of the three safe haven currencies come back.

In Europe, at the time of writing, FTSE is down -0.35%. DAX is flat. CAC is down -0.67%. Germany 10-year yield is down -0.014 at -0.482. Earlier in Asia, Nikkei rose 0.59%. Hong Kong HSI rose 0.47%. China Shanghai SSE rose 1.11%. Singapore Strait Times rose 0.41%. Japan 10-year JGB yield rose 0.0077 to 0.017.

Canada CPI accelerated to 3.7% yoy in Jul

Canada CPI rose 0.6% mom in July, fastest pace since January. Annually, CPI accelerated to 3.7% yoy in July, up from June’s 3.1% yoy, above expectation of 3.4% yoy. Prices rose at a faster pace year over year in six of the eight major components, with shelter prices contributing the most to the all-items increase.

CPI common was unchanged at 1.7% yoy, below expectation of 1.8% yoy. CPI median rose from 2.4% yoy to 2.6% yoy, above expectation of 2.4% yoy. CPI trimmed rose from 2.7% yoy to 3.1% yoy, above expectation of 2.5% yoy.

From the US, housing starts dropped to 1.53m annualized rate in July, versus expectation of 1.60m. Building permits rose to 1.64m, above expectation of 1.61m.

Eurozone CPI finalized at 2.2% yoy in Jul, core CPI at 0.7% yoy

Eurozone CPI was finalized at 2.2% yoy in July 2021, up from June’s 1.9% yoy. Core CPI was finalized at 0.7% yoy. Highest contribution came from energy (+1.34%), followed by food, alcohol & tobacco (+0.35%), services (+0.31%) and non-energy industrial goods (+0.17%).

EU CPI was finalized at 2.5%, up from 2.2% in June. The lowest annual rates were registered in Malta (0.3%), Greece (0.7%) and Italy (1.0%). The highest annual rates were recorded in Estonia (4.9%), Poland and Hungary (both 4.7%). Compared with June, annual inflation fell in nine Member States, remained stable in two and rose in sixteen.

UK CPI slowed to 2.0% yoy in Jul, core CPI down to 1.8% yoy

UK CPI slowed to 2.0% yoy in July, down from 2.5% yoy, below expectation of 2.2% yoy. Core CPI slowed to 1.8% yoy, down from 2.3% yoy, below expectation of 2.2% yoy. RPI dropped to 3.8% yoy, down from 3.9% yoy, below expectation of 3.7% yoy.

PPI input came in at 0.8% mom, 9.9% yoy, versus expectation of 1.2% mom, 10.8% yoy. PPI output was at 0.6% mom, 4.9% yoy, versus expectation of 0.4% mom, 4.8% yoy. PPI core output was at 0.7% mom, 3.9% yoy.

RBNZ keeps rate unchanged on heightened uncertainty

RBNZ kept Official Cash Rate unchanged at 0.25% today, instead of raising it. The decision was “made in the context of the Government’s imposition of Level 4 COVID restrictions on activity across New Zealand.” Nevertheless, it reiterated that the “least regrets policy stance” was still to “further reduce the level of monetary stimulus”. But the Committee agreed to stand pat at this meeting “given the heightened uncertainty with the country in a lockdown.”

In the summary record, it’s also noted that committee members “now had more confidence that rising capacity pressures will feed through into inflation, and that employment is at its maximum sustainable level.” They concluded that “they could continue removing monetary stimulus”, following haling the LSAP program in July.

Also from New Zealand, PPI input accelerated to 3.0% qoq in Q2, up from 2.1% qoq, well above expectation of 0.5% qoq. PPI output jumped to 2.6% qoq, up from 1.2% qoq, above expectation of 0.1% qoq.

Australia leading index dropped to 1.3 in Jul, still consistent with above trend growth

Australia Westpac-MI leading index dropped from 1.36% to 1.30% in July. The index is still consistent with above trend growth over the next 3 to 9 months. Nevertheless, Westpac also said, “no Leading Index can accurately predict the impact of sudden virus lockdowns, although the direct effects of measures will start to become more apparent in the August Index.”

Also, with the deteriorating outlook in New South Wales and Melbourne due to lockdowns, West pact has revised down Q3 GDP forecast to a contraction of -2.6%, to be followed by 2.6% growth in Q4, and very strong growth of 5.0% in 2022.

Westpac added that RBA would likely to “take the same approach” as August in September meeting. That is, there would be no response to the current lockdown risks. However, it added, “we certainly cannot rule out a policy change in September especially if, as we assess, developments have raised some questions as to the vulnerability and timing of the expected recovery.

Also released, Wage price index rose 0.4% qoq in Q2, below expectation of 0.6% qoq.

Japan exports rose 37.0% yoy in Jul, imports rose 28.5% yoy

Japan export rose 37.0% yoy to JPY 7356B in July, slightly below expectation of 39.0% yoy. By region, exports to China rose 18.9% yoy, led by chip-making equipment and plastic. Exports to the US grew 26.8% yoy, led by exports of cars, car parts and motors. Imports rose 28.5% yoy to JPY 6915B, below expectation of 35.1% yoy. Trade balance came in at JPY 441B.

In seasonally adjusted term, exports was unchanged at JPY 7049B. Imports dropped -1.6% mom to 6997B. Trade balanced reported a surplus of JPY 52.7B.

Also from Japan, machinery orders dropped -1.6% mom in June, versus expectation of -2.8% mom.

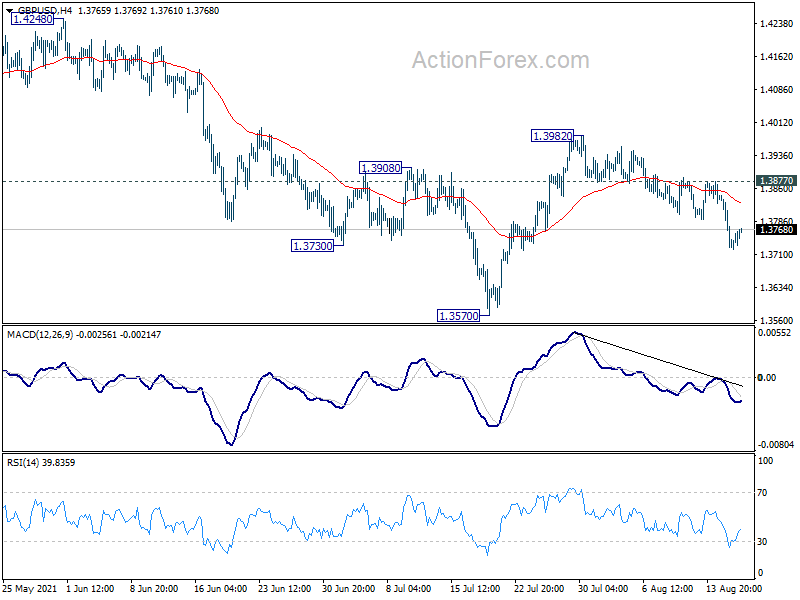

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3695; (P) 1.3770; (R1) 1.3815; More…

Intraday bias in GBP/USD remains mildly on the downside at this point. Rebound from 1.3570 should have completed at 1.3982, after the rejection by 55 day EMA. Deeper fall would be seen to retest 1.3570 first. Break will 1.3482 resistance turned support. On the upside, above 1.3877 minor resistance will turn bias back to the upside for 1.3982.

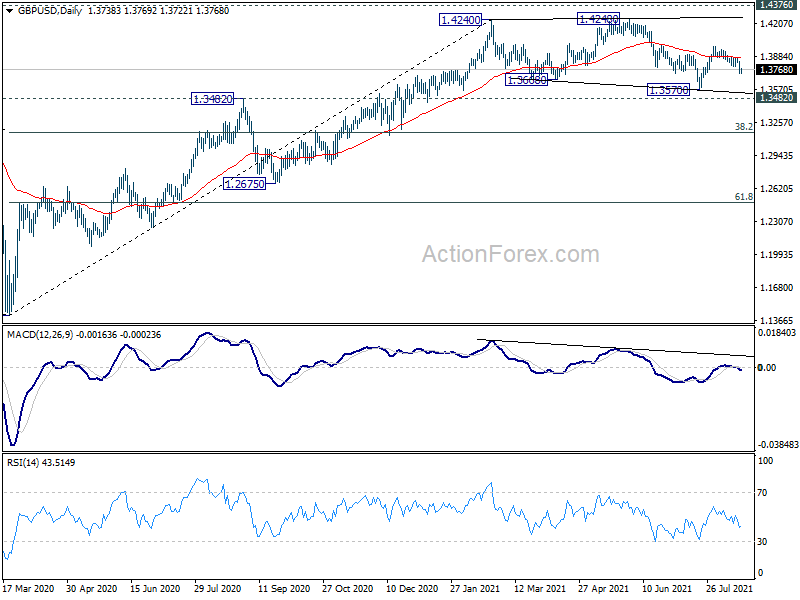

In the bigger picture, as long as 1.3482 resistance turned support holds, up trend from 1.1409 should still continue. Decisive break of 1.4376 resistance will carry larger bullish implications. However, firm break of 1.3482 support will argue that the rise from 1.1409 has completed. GBP/USD would then be seen as in another leg of long term range pattern between 1.1409 and 1.4376. Deeper fall could then be seen to 61.8% retracement of 1.1409 to 1.4248 at 1.2493, and even below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | PPI Input Q/Q Q2 | 3.00% | 0.50% | 2.10% | |

| 22:45 | NZD | PPI Output Q/Q Q2 | 2.60% | 0.10% | 1.20% | |

| 23:50 | JPY | Trade Balance (JPY) Jul | 0.05T | 0.12T | -0.09T | -0.06T |

| 23:50 | JPY | Machinery Orders M/M Jun | -1.50% | -2.80% | 7.80% | |

| 00:30 | AUD | Westpac Leading Index M/M Jul | -0.10% | -0.06% | ||

| 01:30 | AUD | Wage Price Index Q/Q Q2 | 0.40% | 0.60% | 0.60% | |

| 02:00 | NZD | RBNZ Rate Decision | 0.25% | 0.50% | 0.25% | |

| 03:00 | NZD | RBNZ Press Conference | ||||

| 06:00 | GBP | CPI M/M Jul | 0.00% | 0.30% | 0.50% | |

| 06:00 | GBP | CPI Y/Y Jul | 2.00% | 2.20% | 2.50% | |

| 06:00 | GBP | Core CPI Y/Y Jul | 1.80% | 2.20% | 2.30% | |

| 06:00 | GBP | RPI M/M Jul | 0.50% | 0.30% | 0.70% | |

| 06:00 | GBP | RPI Y/Y Jul | 3.80% | 3.70% | 3.90% | |

| 06:00 | GBP | PPI Input M/M Jul | 0.80% | 1.20% | -0.10% | 0.50% |

| 06:00 | GBP | PPI Input Y/Y Jul | 9.90% | 10.80% | 9.10% | 9.70% |

| 06:00 | GBP | PPI Output M/M Jul | 0.60% | 0.40% | 0.40% | 0.60% |

| 06:00 | GBP | PPI Output Y/Y Jul | 4.90% | 4.80% | 4.30% | 4.90% |

| 06:00 | GBP | PPI Core Output M/M Jul | 0.70% | 0.30% | 0.60% | |

| 06:00 | GBP | PPI Core Output Y/Y Jul | 3.90% | 2.70% | 3.70% | |

| 09:00 | EUR | Eurozone CPI Y/Y Jul F | 2.20% | 2.20% | 2.20% | |

| 09:00 | EUR | Eurozone CPI – Core Y/Y Jul F | 0.70% | 0.70% | 0.70% | |

| 12:30 | USD | Housing Starts Jul | 1.53M | 1.60M | 1.64M | 1.65M |

| 12:30 | USD | Building Permits Jul | 1.64M | 1.61M | 1.59M | 1.59M |

| 12:30 | CAD | CPI M/M Jul | 0.60% | 0.40% | 0.30% | |

| 12:30 | CAD | CPI Y/Y Jul | 3.70% | 3.40% | 3.10% | |

| 12:30 | CAD | CPI Common Y/Y Jul | 1.70% | 1.80% | 1.70% | |

| 12:30 | CAD | CPI Median Y/Y Jul | 2.60% | 2.40% | 2.40% | |

| 12:30 | CAD | CPI Trimmed Y/Y Jul | 3.10% | 2.50% | 2.60% | 2.70% |

| 14:30 | USD | Crude Oil Inventories | -1.5M | -0.4M | ||

| 18:00 | USD | FOMC Minutes |

{kind=link}