Swiss Franc is strengthening notably today, but selling focus has somewhat shifted from Euro to Sterling. Still, the franc is outshone by New Zealand Dollar, which is overwhelming the strongest. On the other hand, Yen is the weaker one following extended risk-on sentiments from Japan to Europe. Sterling is following closely as second weakest. Dollar is mixed with Canadian.

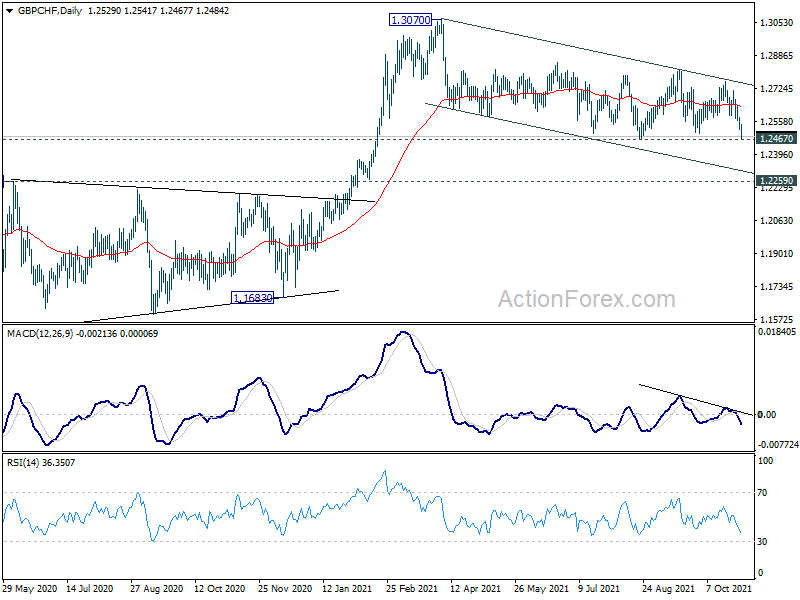

Technically, selloff in GBP/CHF today suggests that corrective pattern from 1.3070 is ready to resume. Break of 1.2467 support will target 1.2259 resistance turned support next. If that happens, we’d pay attention to 1.3646 support in GBP/USD, 0.8474 resistance in EUR/GBP, as well as 0.9101 support in USD/CHF. Price actions in these pairs should reveal whether it’s Sterling’s weakness, or Franc’s strength, or both.

In Europe at the time of writing, FTSE is up 0.36%. DAX is up 0.67%. CAC is up 0.74%. Germany 10-year yield is up 0.031 at -0.073. Earlier in Asia, Nikkei rose 2.61%. Hong Kong HSI dropped -0.88%. China Shanghai SSE dropped -0.08%. Singapore Strait Times rose 0.65%. Japan 10-year yield dropped -0.0030 to 0.097.

UK PMI manufacturing finalized at 57.8, low growth environment met with inflationary pressures

UK PMI Manufacturing was finalized at 57.8 in October, slightly up from September’s 57.1. That’s, nonetheless, the first rise in five months. Market said new order growth ticked higher despite dropped in new export work. But selling prices rose at record pace.

Rob Dobson, Director at IHS Markit, said: ” Strained global supply chains are disrupting production schedules, while staff shortages and declining intakes of new export work are also stymieing the upturn. This low growth environment is occurring in tandem with a severe upshot in inflationary pressures, with manufacturers reporting both a near-record increase in input costs and record rise in selling prices.”

China Caixin PMI manufacturing rose to 50.6, supply strains became the paramount factor

China Caixin PMI Manufacturing rose to 50.6 in October, up from 50.0, above expectation of 50.6. Caixin noted total new work had the strongest increase in four months. Production fell modestly amid rising costs and reduced power supply. Average lead times rose at fastest rate since March 2020.

Wang Zhe, Senior Economist at Caixin Insight Group said: “To sum up, manufacturing recovered slightly in October from the previous month. But downward pressure on economic growth continued. We noticed that the pandemic’s impact on manufacturing faded from late September to mid-October as the number of new Covid-19 cases dropped, which boosted demand.

“However, supply strains became the paramount factor affecting the economy. Shortages of raw materials and soaring commodity prices, combined with electricity supply problems, created strong constraints for manufacturers and disrupted supply chains. Input costs for manufacturers have risen much faster than output prices for several months, putting a lot of pressure on downstream enterprises.”

Released over the weekend, official PMI Manufacturing dropped to 49.2 in October, down from 49.6, below expectation of 49.7. PMI Non-Manufacturing dropped to 52.4, down from 53.2, below expectation of 53.0.

Japan PMI manufacturing finalized at 53.2 in Oct, record business optimism

Japan PMI Manufacturing was finalized at 53.2 in October, up from September’s 51.5. Markit said there were renewed rises in output and new orders. Input prices and output charges rose at quickest rate in over 13 years. Business optimism accelerated to series-record high.

Usamah Bhatti, Economist at IHS Markit, said: “October PMI data pointed to a stronger expansion in the Japanese manufacturing sector at the start of the fourth quarter… Overall, the headline Manufacturing PMI was at its highest reading since April and the second-highest in the year to date…

“Material shortages and delivery delays induced sharp rises in input prices, as average cost burdens rose at the sharpest pace since August 2008. This contributed to higher charges for clients in attempts to cover margins, with factory gate inflation quickening to a 13-year high..

“Confidence about the outlook reached the highest level since the series began in July 2012, as hopes that the end of the pandemic would stimulate a broad market recovery gathered pace. This is broadly in line with the IHS Markit forecast for industrial production to grow 7.1% this year and 4.3% in 2022.”

Australia AiG manufacturing dropped to 50.4, but encouraged by rise in new orders

Australia AiG Performance of Manufacturing Index dropped -0.8 to 50.4 in October. That’s the fourth consecutive month of decline and lowest reading since September 2020. Looking at some details, production dropped -5.3 to 47.8. Employment rose 0.9 to 48.0. New orders rose 6.3 to 58.3. Exports dropped -5.8 to 46.1. Input prices rose 3.7 to 81.8. Selling prices dropped -0.8 to 63.9. Average wages rose 10.8 to 63.7.

Ai Group Chief Executive Innes Willox said: “Although restrictions began to be eased, vaccination rates rose and the country edged towards a living with COVID approach, the year-long run of improving manufacturing performance was put on hold in October…. Although October was nothing to write home about, manufacturers will be encouraged by the sharp lift in new orders received and by the further progress towards removing COVID restrictions.

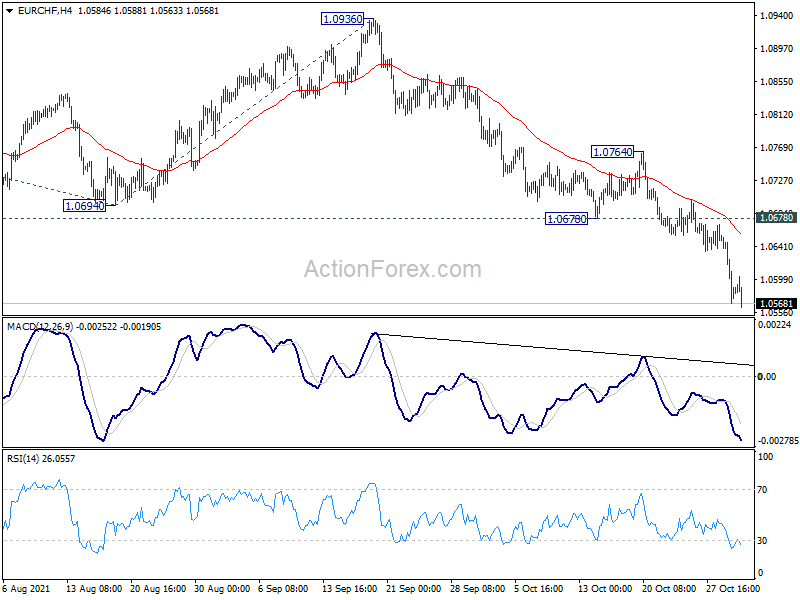

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.0549; (P) 1.0603; (R1) 1.0635; More….

EUR/CHF’s down trend continues today and hit as low as 1.0563 so far. Intraday bias stays on the downside for 100% projection of 1.1149 to 1.0694 from 1.0936 at 1.0481. On the upside, break of 1.0678 support turned resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, current downside momentum argues that fall from 1.1149 is probably resuming the downside from 1.2004 (2018 high). Next focus is 1.0505 (2020 low). Decisive break there will confirm this bearish case and target 61.8% projection of 1.2004 to 1.0505 to 1.1149 at 1.0223 next. Strong support from 1.0505 will bring rebound first. But outlook will stay bearish as long as 1.0936 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Manufacturing Index Oct | 50.4 | 51.6 | ||

| 0:30 | JPY | Manufacturing PMI Oct | 53.2 | 53 | 53 | |

| 1:45 | CNY | Caixin Manufacturing PMI Oct | 50.6 | 50.2 | 50 | |

| 7:00 | EUR | Germany Retail Sales M/M Sep | -2.50% | 0.60% | 1.10% | |

| 8:30 | CHF | SVME PMI Oct | 65.4 | 65.5 | 68.1 | |

| 9:30 | GBP | Manufacturing PMI Oct F | 57.8 | 57.7 | 57.7 | |

| 13:30 | CAD | Manufacturing PMI Oct | 57.2 | 57 | ||

| 13:45 | USD | Manufacturing PMI Oct F | 59.2 | 59.2 | ||

| 14:00 | USD | ISM Manufacturing PMI Oct | 60.4 | 61.1 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Oct | 82.5 | 81.2 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Oct | 50.2 | |||

| 14:00 | USD | Construction Spending M/M Sep | 0.50% | 0.00% |

{kind=link}