Overall markets are quite mixed for now. While US indexes surged to new record highs overnight, positive sentiment was not carried forward to Asia. Major pairs and crosses are also stuck in range. It seems that traders and investors have turned into cautious mode, awaiting Fed’s tapering decision. For now, Euro and Swiss Franc are the stronger ones for the week. Aussie and Kiwi are the weaker ones despite solid job data from New Zealand. The greenback is mixed, together with Yen and Canadian.

Technically, Dollar’s outlook is rather mixed for the moment. The fall in GBP/USD suggests that rebound from 1.3410 might have completed at 1.3833, as a corrective move. That aligns GBP/USD with EUR/USD’s near term bearish outlook. But more downside is still in favor in USD/CHF with 0.9174 minor resistance holds. AUD/USD’s pull back doesn’t warrant near term reversal yet. USD/CAD also also struggling in tight range with bears bias. We’d be cautious in trading Dollar’s post-FOMC reaction today, and pay attention to the bigger picture of all mostly traded pairs before making a judgement.

In Asia, at the time of writing, Hong Kong HSI is down -0.91%. China Shanghai SSE is down -0.38%. Singapore Strait Times is down -0.37%. Japan is on holiday. Overnight, DOW rose 0.39%. S&P 500 rose 0.37%. NASDAQ rose 0.34%. 10-year yield dropped -0.026 to 1.549.

New Zealand unemployment dropped to record low 3.4% in Q3

New Zealand employment rose 2.0% qoq in Q3, much better than expectation of 0.4% qoq. Growth was largely driven by full-time jobs, which increased 2.3% qoq or 50k, while part-time jobs dropped slightly. Unemployment rate dropped sharply from 4.0% to 3.4%, better than expectation of 3.9%. The total employment matched the lowest level on record, reached last time in 2007. Labor force participation rate rose 0.7% to 71.2%.

“The fall in the unemployment rate is in line with reports of difficulty finding workers and high labour turnover, and continued travel restrictions on international arrivals, which put pressure on domestic labour supply,” work and wellbeing statistics senior manager Becky Collett said.

Australia AiG construction rose to 57.6, healthy leap in activity

Australia AiG Performance of Construction rose 4.3 pts to 57.6 in October. Looking at some details, activity rose 15.4 to 65.2. Employment dropped -0.2 to 56.8. New orders dropped -0.2 to 58.7. Supplier deliveries dropped -1.3 to 41.3. Input prices dropped -1.2 to 97.2. Selling prices dropped -0.5 to 78.3. Average wages dropped -1.5 to 75.1.

Ai Group Head of Policy, Peter Burn, said: “The healthy leap in activity levels across the Australian construction sector in October is a taste of what is expected to be a strong rebound for the broader economy over the next few months as New South Wales, Victoria and the ACT, liberated from COVID restrictions, catch up with the rest of the country and as barriers to the movement of people within Australia are removed.”

Also released building permits dropped -4.3% mom in September, versus expectation of -2.0% mom.

China Caixin PMI services rose to 53.8, composite rose to 51.5

China Caixin PMI Services rose to 53.8 in October, up from 53.4, above expectation of 53.6. PMI Composite ticked up to 51.5, from 51.4.

Wang Zhe, Senior Economist at Caixin Insight Group said: “As the number of new Covid-19 cases dropped from late September to the middle of October, related disruption faded and market demand recovered while supply was relatively weak. Manufacturing was significantly weaker than services.

“Supply strains became the paramount factor affecting the economy. Shortages of raw materials and soaring commodity prices, combined with electricity supply problems, created strong constraints for manufacturers. Those factors also had a significant impact on services enterprises.

“Input costs for manufacturers have risen much faster than their output prices for several months. The growth rate of input costs for service providers was also higher than that for prices they charged, putting pressure on downstream enterprises.”

Fed to announce tapering, some previews

FOMC monetary policy decision is the major focus today, as Fed should finally make a formal announcement on QE tapering. As the September minutes indicates, the pace would be “monthly reductions in the pace of asset purchases, by US$10B in the case of Treasury securities and US$5B in the case of agency mortgage-backed securities (MBS)”. The would eventually lead to completion of entire asset purchases by mid -2022. But, a hawkish surprise – monthly reduction at a faster pace – cannot be ruled out given the inflationary pressure.

Also, September’s dot plot revealed that half of the members had anticipated a rate hike in 2022. Meanwhile, the market has priced in futures have priced in over 60% of a rate hike by June next year. But Fed Chair Jerome Powell would likely reiterate that decision on interest rate is complete separated from that of asset purchases. There wouldn’t be any new hint on the timing of rate hike until December’s dot plot.

Suggested readings on Fed

- FOMC Preview – Tapering to Formally Begin

- FOMC Preview: It’s Time To Taper

- Fed Research Preview: Tapering, Yes, But How Fast?

- October Flashlight for the FOMC Blackout Period

Also featured

Eurozone will release unemployment rate in European session while UK will release PMI services final. US will release ADP employment, ISM services and factory orders too.

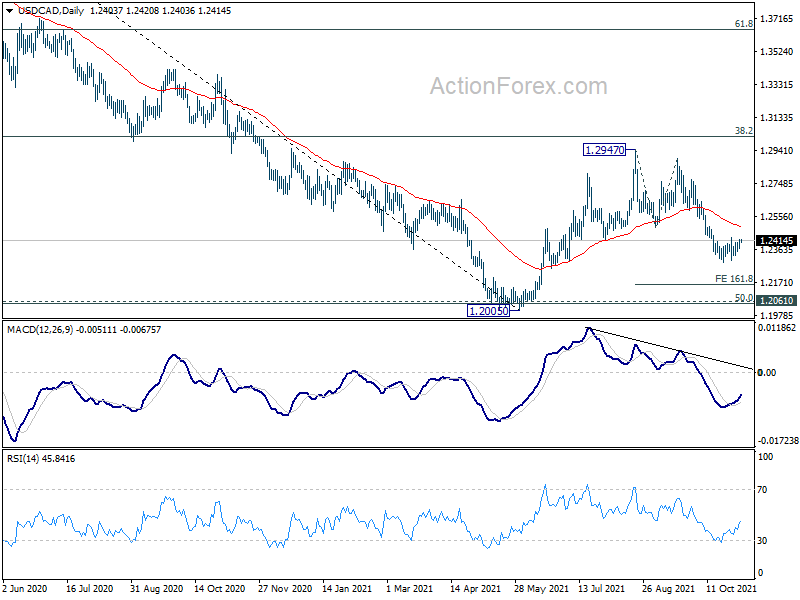

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2377; (P) 1.2401; (R1) 1.2434; More…

Intraday bias in USD/CAD remains neutral as consolidation from 1.2286 is still extending. Outlook is unchanged that in case of stronger recovery, upside should be limited by 1.2497 resistance. On the downside, break of 1.2286 will resume the fall from 1.2947 to 161.8% projection of 1.2947 to 1.2492 from 1.2894 at 1.2158 next. However, firm break of 1.2497 will turn bias back to the upside for stronger rebound.

In the bigger picture, the rejection by 38.2% retracement of 1.4667 to 1.2005 at 1.3022 argues that rebound from 1.2005 is merely a corrective rise, which is complete. More importantly, the down trend from 1.4667 (2020 high) is not over yet. Sustained break of 1.2005 will extend the down trend to next long term fibonacci level at 61.8% retracement of 0.9406 to 1.4689 at 1.1424. In any case, outlook will not turn bullish as long as 1.2947 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Construction Index Oct | 57.6 | 53.3 | ||

| 21:45 | NZD | Employment Change Q3 | 2.00% | 0.40% | 1.00% | |

| 21:45 | NZD | Unemployment Rate Q3 | 3.40% | 3.90% | 4.00% | |

| 21:45 | NZD | Labour Cost Index Q/Q Q3 | 0.70% | 0.80% | 0.90% | |

| 00:30 | AUD | Building Permits M/M Sep | -4.30% | -2.00% | 6.80% | 7.60% |

| 01:45 | CNY | Caixin Services PMI Oct | 53.8 | 53.6 | 53.4 | |

| 09:00 | EUR | Eurozone Unemployment Rate Sep | 7.40% | 7.50% | ||

| 09:30 | GBP | Services PMI Oct F | 58 | 58 | ||

| 12:15 | USD | ADP Employment Change Oct | 400K | 568K | ||

| 13:45 | USD | Services PMI Oct F | 58.2 | 58.2 | ||

| 14:00 | USD | ISM Services PMI Oct | 62 | 61.9 | ||

| 14:00 | USD | ISM Services Employment Index Oct | 53.3 | 53 | ||

| 14:00 | USD | Factory Orders M/M Sep | -0.10% | 1.20% | ||

| 14:30 | USD | Crude Oil Inventories | 1.9M | 4.3M | ||

| 18:00 | USD | Fed Interest Rate Decision | 0.25% | 0.25% | ||

| 18:30 | USD | FOMC Press Conference |

{kind=link}