Dollar dropped notably overnight after Fed Chair Jerome Powell surprised the markets by ruling out a 75bps rate hike. The comment also boosted US stocks sharply higher. Risk-on sentiment helped commodity currencies rebound. But European majors are lagging behind. Yen is so far mixed, with slight retreat in US 10-year yield. BoE rate decision would provide more volatility to the markets, and non-farm payrolls tomorrow too.

Technically, it’s still early to call for a deep correction in Dollar, no to mention a bearish reversal. Nevertheless, AUD/USD’s breach of 0.7228 minor resistance suggest short term bottoming. USD/CAD could also break through 1.2717 support to indicate short term topping too. Other levels to watch will include 1.0756 support turned resistance in EUR/USD and 126.91 support in USD/JPY.

In Asia, Japan is on holiday. Hong Kong HSI is up 0.52%. China Shanghai SSE is up 0.76%. Singapore Strait Times is down -0.16%. Overnight, DOW rose 2.81%. S&P 500 rose 2.99%. NASDAQ rose 3.19%. 10-year yield dropped -0.043 to 2.917.

Fed hikes by 50bps, starts balance sheet runoff, highly attentive to inflations risks

Fed raised interest rate target by 50bps to 0.75% to 1.00% as expected. It also announced to start the balance sheet runoff, by USD 95B as expected (USD 60B treasuries and USD 35B MBS). The decision was by unanimous vote.

The FOMC is “highly attentive to inflations risks”. The accompany statement noted that the implications of invasion of Ukraine by Russia for US economy are “highly uncertain”. ” The invasion and related events are creating additional upward pressure on inflation and are likely to weigh on economic activity.” Meanwhile, lockdowns in China are “likely to exacerbate supply chain disruptions”

Fed pledged to “adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals”.

DOW jumped 2.8% as Fed Powell ruled out 75bps hike

US stocks staged a strong rebound overnight after Fed Chair Jerome Powell ruled out a 75bps hike. In the post-meeting press conference, he clearly said in a rare fashion, “a 75 basis point increase is not something that the committee is actively considering.” Traders were swift in adjusting their expectations. Just a day ago, markets were pricing in 99% chance of a 75bps hike in June.

DOW closed up 932.27 pts or 2.81% at 34061.06. Immediate focus is now back on 55 day EMA (at 34276.20). A weekly close above this level will set the base for further rally back to 35492.22 resistance in the near term. Break there will bring retest of 36952.65 high. Overall, while corrective pattern from 36952.65 could still extend for while. The range should have been set in this case.

China Caixin PMI services dropped to 36.2 in Apr, PMI composite down to 37.2

China Caixin PMI Services dropped from 42.0 to 36.2 in April, below expectation of 40.9. That’s the second straight month of steep decline, and the worst reading since February 2020. Caixin said decline in new business gathered pace but employment fell only slightly. PMI Composite dropped from 43.9 to 37.2, also the worst since the onset of the pandemic.

Wang Zhe, Senior Economist at Caixin Insight Group said: “Overall, in April, local Covid outbreaks continued and activity in the manufacturing and service sectors continued to contract, with services shrinking more. Demand was under pressure, external demand deteriorated, supply shrank, supply chains were disrupted, delivery times were prolonged, backlogs of work grew, workers found it difficult to return to their jobs, inflationary pressures lingered, and market confidence remained below the long-term average.”

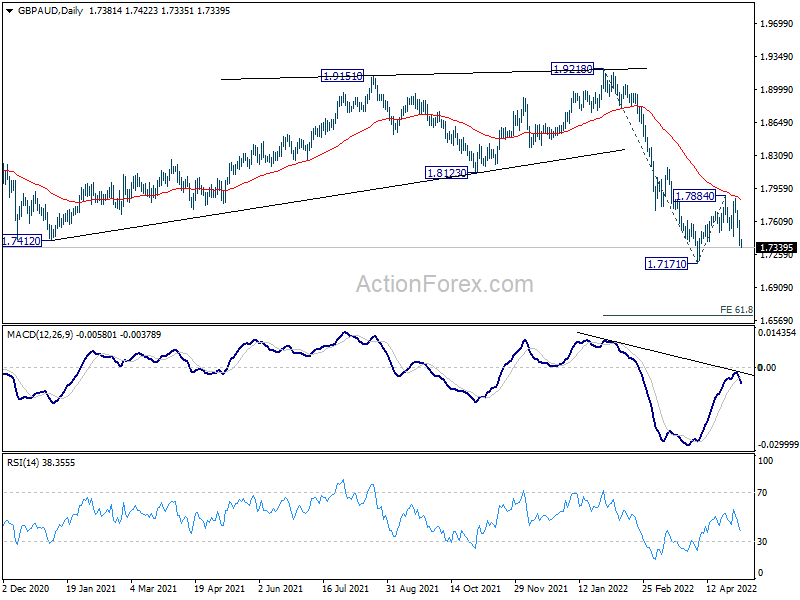

BoE to hike another 25ps, a look at bearish GBP/AUD

BoE is widely expected to continue with its tightening cycle, and raise Bank rate by 25bps to 1.00% today. Focus is firstly on the voting, on the whether any hawks would push for faster pace of hikes. Secondly, BoE might make a decision to actively shrink its balance sheet. Thirdly the new economic projections will also be scrutinized for the policy path and economic outlook.

Here are some previews:

- BoE Policy Meeting: A Normal Rate Hike Amid Stagflation Fears

- BoE Preview: MPC Won’t Deviate Much from Recent Hawkish Path

- BoE Meeting Preview – A Trade-off Between Growth and Inflation

- Bank of England Preview: Another Rate Hike and Active QT

GBP/AUD is a pair to watch for the near term, considering the possible return of risk-on sentiment too. The corrective recovery from 1.7171 might have completed at 1.7884, after failing to break through 55 day EMA. That is, medium term down trend might be ready to resume.

For the near term, deeper decline is in favor to retest 1.7171 support first. Firm break there will confirm this bearish case, and target 61.8% projection of 1.9218 to 1.7171 from 1.7884 at 1.6619. In any case, outlook will stay bearish as long as 1.7884 resistance holds.

Elsewhere

Australia building permits dropped -18.5% mom in March, versus expectation of -12.0% mom. Australia trade surplus widened to AUD 9.31B in March, versus expectation of AUD 7.80B. Germany factor orders dropped -4.7% in March, versus expectation of -0.5%.

Swiss CPI, France industrial output, UK PMI services will be released in European session. later in the day, US will release jobless claims and non-farm productivity.

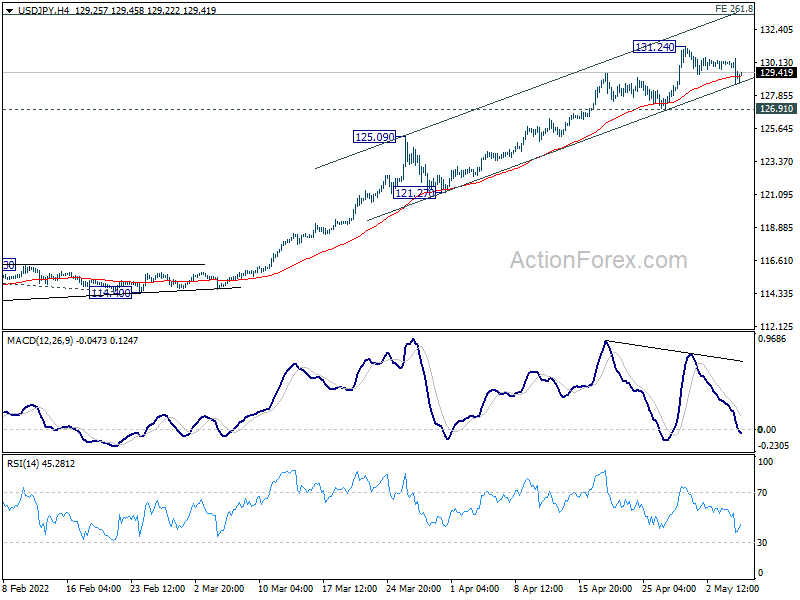

USD/JPY Daily Outlook

Daily Pivots: (S1) 129.79; (P) 130.04; (R1) 130.38; More…

USD/JPY dips notably as correction from 131.24 extends, but stays well above 126.91 support. Near term outlook remains bullish with further rally expected. On the upside, break of 131.24 will resume recent up trend to 261.8% projection of 109.11 to 116.34 from 114.40 at 133.26. However, considering bearish divergence condition in 4 hour MACD, break of 126.91 will confirm short term topping and turn bias back to the downside for 121.27/125.09 support zone.

In the bigger picture, current rally is seen as part of the long term up trend form 75.56 (2011 low). Sustained trading above 61.8% projection of 75.56 (2011 low) to 125.85 (2015 high) from 98.97 at 130.04 will pave the way to 100% projection at 149.26, which is close to 147.68 (1998 high). For now, this will remain the favored case as long as 121.27 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Building Permits M/M Mar | -18.50% | -12.00% | 43.50% | 42.00% |

| 01:30 | AUD | Trade Balance (AUD) Mar | 9.31B | 7.80B | 7.46B | 7.44B |

| 01:45 | CNY | Caixin Services PMI Apr | 36.2 | 40.9 | 42 | |

| 06:00 | EUR | Germany Factory Orders Mar | -4.70% | -0.50% | -2.20% | -0.80% |

| 06:30 | CHF | CPI M/M Apr | 0.20% | 0.60% | ||

| 06:30 | CHF | CPI Y/Y Apr | 2.50% | 2.40% | ||

| 06:45 | EUR | France Industrial Output M/M Mar | 0.00% | -0.90% | ||

| 08:30 | GBP | Services PMI Apr F | 58.3 | 58.3 | ||

| 11:00 | GBP | BoE Interest Rate Decision | 1.00% | 0.75% | ||

| 11:00 | GBP | MPC Official Bank Rate Votes | 8–0–1 | 8–0–1 | ||

| 11:30 | USD | Challenger Job Cuts Y/Y Apr | -30.10% | |||

| 12:30 | USD | Initial Jobless Claims (Apr 29) | 176K | 180K | ||

| 12:30 | USD | Nonfarm Productivity Q1 P | -2.30% | 6.60% | ||

| 12:30 | USD | Unit Labor Costs Q1 P | 7.40% | 0.90% | ||

| 14:30 | USD | Natural Gas Storage | 69B | 40B |

{kind=link}