Swiss Franc surges sharply higher today after surprised rate hike by SNB. Sterling also rises on BoE rate hike with hawkish voting. Yen is following closely on risk aversion but Dollar is lagging slightly behind. The greenback is still digesting post FOMC position adjustments. Risk-off sentiment sends commodity currencies lower, as led by Aussie. But Euro is also weak as pressured by selling against Pound and Franc.

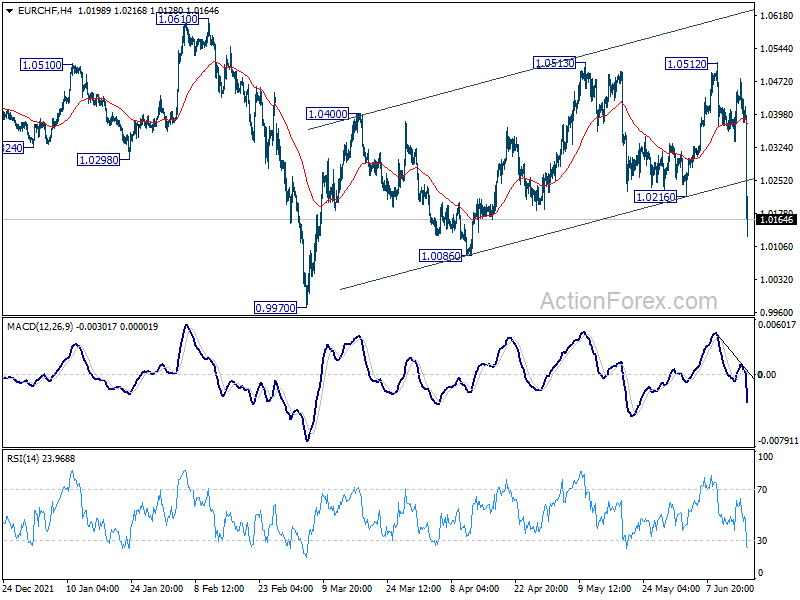

Technically, Euro is one again displaying some notable weakness. The break of 1.0216 support in EUR/CHF raises the chance of revisiting 0.9970 low. Focus will now be on 0.8484 support in EUR/GBP. Firm break there will suggest near term bearish reversal, after rejection by 0.8697 medium term fibonacci level. Meanwhile, decisive break of 1.0339 key support in EUR/USD will confirm down trend resumption.

In Europe, at the time of writing, FTSE is down -2.57%. DAX is down -2.49%. CAC is down -1.81%. Germany 10-year yield is up 0.162 at 1.805. Earlier in Asia, Nikkei rose 0.40%. Hong Kong HSI dropped -2.17%. China Shanghai SSE dropped -0.61%. Singapore Strait Times dropped -0.27%. Japan 10-year JGB yield rose 0.0148 to 0.270.

US initial jobless claims dropped to 229k, slightly below expectations

US initial jobless claims dropped -3k to 229k in the week ending June 11, slightly better than expectation of 230k. Four-week moving average of initial claims rose 3k to 219k. Continuing claims rose 3k to 1312k in the week ending June 4. Four-week moving average of continuing claims dropped slightly by -750 to 1317.5k, lowest since January 10, 1970, when it was 1311k.

Housing starts dropped to 1.55m annualized in May, below expectation of 1.71m. Building permits dropped to 1.695m, below expectation of 1.79m. Philly Fed manufacturing survey dropped from 2.6 to 5.5 in June, below expectation of 5.5.

BoE hikes by 25bps, three members want 50bps

BoE raises the Bank Rate by 25bps to 1.25%. The decision was not unanimous, with three members (Catherine Mann, Michael Saunders and Jonathan Haskel) voted for a 50bps hike. The MPC said it will take necessary actions to return inflation to 2% target. The scale, pace and timing of further rate hikes will reflect the assessment of economic outlook and inflation pressures.

Nevertheless, it emphasized, “the Committee will be particularly alert to indications of more persistent inflationary pressures, and will if necessary act forcefully in response.”

BoE also said GDP was weaker than expected in April, and it expect GDP to fall by -0.3% in Q2 as a while, weaker than anticipated at in the May Monetary Policy Report. CPI inflation’s rise to 9% was “close to expectations” at the time of the May report. CPI is expected to be over 9% “during the next few months” and rise to “slightly above 11% in October.

SNB surprisingly hikes 50bps, adopts tightening bias

SNB surprises the markets by raising the sight deposit rate by 50bps to -0.25% today, “to counter increased inflationary pressure”. It also adopts a tightening bias and said, “it cannot be ruled out that further increases in the SNB policy rate will be necessary in the foreseeable future to stabilise inflation in the range consistent with price stability over the medium term.” SNB also maintains the willingness to intervene in the currency markets if necessary.

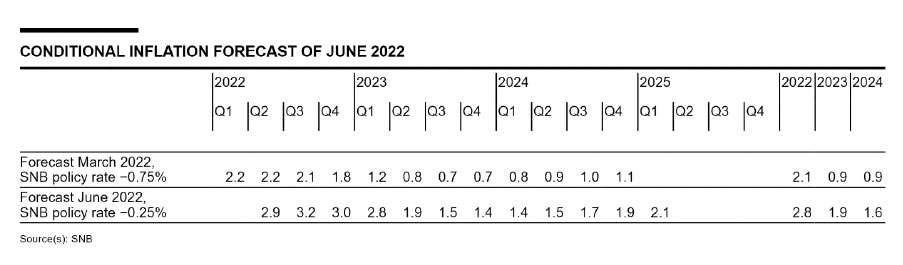

Even with higher interest rates, the conditional inflation forecasts were also raised across forecast horizon. Inflation is projected to peak at 3.2% in Q3, then slow to below 1.4% in Q4 2023, then rise back to 2.1% in Q1 2025. Average inflation is forecasts to be at 2.8% in 2022, 1.9% in 2023, and 1.6% in 2024, upgraded from 2.1%, 0.9% and 0.9% respectively.

As for the economy, SNB still expected 2.5% GDP growth in 2022 while unemployment is “likely to remain low”. However, “if the energy supply in Europe were to be adversely affected, this could have a serious impact on the Swiss economy. The global supply bottlenecks and further increases in commodity prices could also slow growth. Furthermore, a resurgence of the coronavirus pandemic cannot be ruled out.”

SNB Jordan: Swiss Franc no longer highly valued

SNB Chairman Thomas Jordan said in the post-meeting pressing conference, “the new inflation forecast shows that further increases in the policy rate may be necessary in the foreseeable future.”

“In the current environment, price increases were being passed on more quickly, and are also being more readily accepted, than was the case until recently,” he said. “There is the threat of second-round effects becoming entrenched if inflation remains above 2% for a long period.”

Jordan also noted that the Franc’s strength on safe-haven flow helped dampen the impact on higher fuel and food import prices. But that was less the case following recent decline. “Thus the inflation imported from abroad has increased,” he said. “Another consequence of this depreciation coupled with significantly higher inflation abroad is that the franc is no longer highly valued.”

Australia employment rose 60.6k in May, strong growth in hours worked

Australia employment rose 60.6k in May, better than expectation of 25.0k. Full-time jobs rose 69.4k while part-time jobs dropped -8.7k. Unemployment rate was unchanged at 3.9%, above expectation of 3.8%. Participation rate rose 0.3% to 66.7%. Monthly hours worked rose 0.9% mom or 17m.

Bjorn Jarvis, head of labour statistics at the ABS, said: “The increase in May 2022 was the seventh consecutive increase in employment, following the easing of lockdown restrictions in late 2021. Average employment growth over the past three months (30,000) continues to be stronger than the pre-pandemic trend of around 20,000 people per month.

“In addition to the continuing trend of increasing employment, we have continued to see relatively stronger growth in hours worked. This is something we also saw this time last year, before the Delta outbreak.”

New Zealand GDP fell -0.2% qoq in Q1, primary industries drove contraction

New Zealand GDP contracted -0.2% qoq in Q1, much worse than expectation of 0.6% qoq.

StatsNZ said: “Primary industries drove the decrease in GDP, down 1.2 percent in the quarter. Goods producing industries also experienced a slight decline, down 0.1 percent.

“The service industry group, which makes up approximately two thirds of the economy, remained flat. This result reflects falls in some industries being offset by rises in others.”

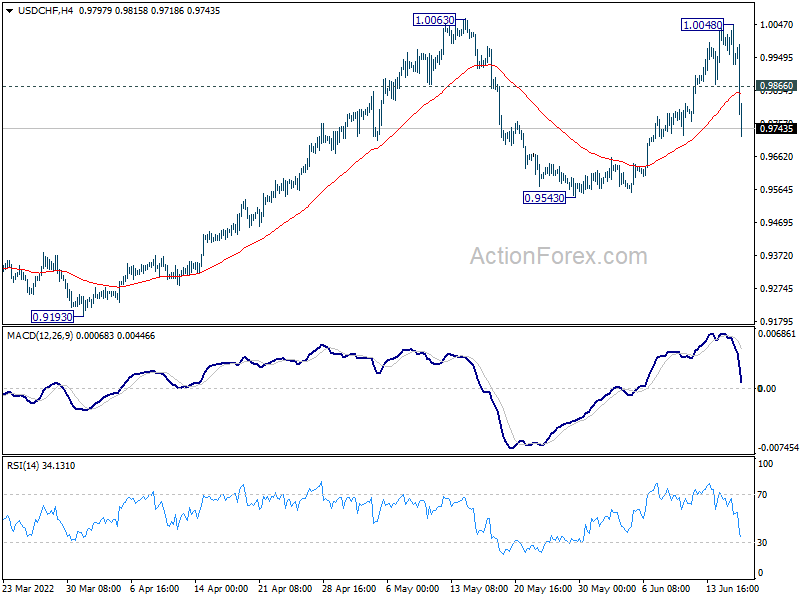

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9899; (P) 0.9974; (R1) 1.0017; More…

USD/CHF’s steep decline suggests that rebound from 0.9543 has completed at 1.0048, after rejection by 1.0063 resistance. Intraday bias mildly on the downside for 0.9543 support. Such fall is seen as the third leg of the corrective pattern from 1.0063. Strong support should be seen at around 0.9543 to contain downside to bring rebound. On the upside, above 0.9866 minor resistance will turn bias back to the upside for retesting 1.0063 resistance.

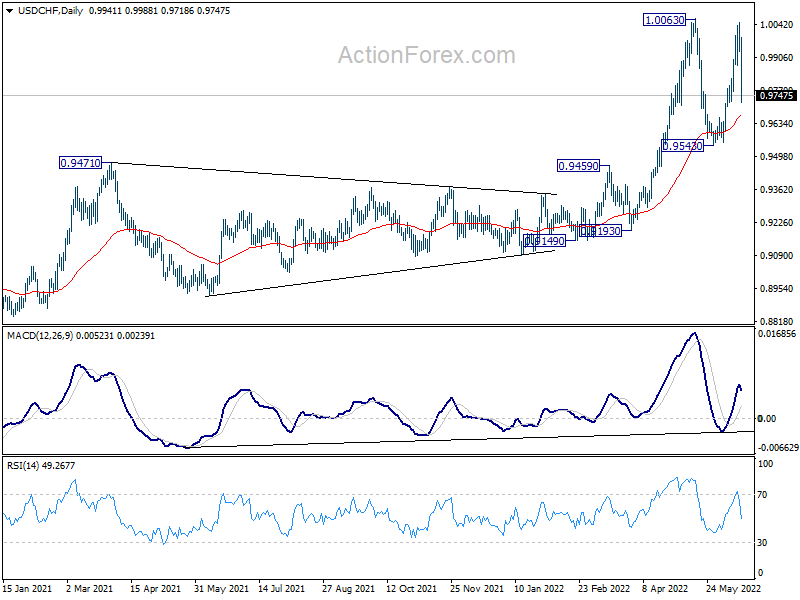

In the bigger picture, down trend from 1.0342 (2016 high) should have completed with three waves down to 0.8756 (2021 low) already. Rise from 0.8756 is likely a medium term up trend of its own. Next target is 1.0237/0342 resistance zone. This will remain the favored case as long as 0.9471 resistance turned support holds. However, sustained break of 0.9471 will extend long term range trading with another falling leg.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | GDP Q/Q Q1 | -0.20% | 0.60% | 3.00% | |

| 23:50 | JPY | Trade Balance (JPY) May | -1.93T | -1.70T | -1.62T | -1.58T |

| 01:00 | AUD | Consumer Inflation Expectations Jun | 6.70% | 5.00% | ||

| 01:30 | AUD | Employment Change May | 60.6K | 25.0K | 4.0K | 4.4K |

| 01:30 | AUD | Unemployment Rate May | 3.90% | 3.80% | 3.90% | |

| 07:30 | CHF | SNB Interest Rate Decision | -0.25% | -0.75% | -0.75% | |

| 11:00 | GBP | BoE Interest Rate Decision | 1.25% | 1.25% | 1.00% | |

| 11:00 | GBP | MPC Official Bank Rate Votes | 9–0–0 | 9–0–0 | 9–0–0 | |

| 12:30 | CAD | Wholesale Sales M/M Apr | -0.50% | 0.50% | 0.30% | |

| 12:30 | USD | Initial Jobless Claims (Jun 10) | 229K | 230K | 229K | |

| 12:30 | USD | Housing Starts May | 1.55M | 1.71M | 1.72M | |

| 12:30 | USD | Building Permits May | 1.695M | 1.79M | 1.82M | |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Jun | -3.3 | 5.5 | 2.6 | |

| 14:30 | USD | Natural Gas Storage | 92B | 97B |

{kind=link}