Euro is sold off broadly, together with Sterling, after Russia announced partial military mobilization. Reactions in European stock markets are muted, nevertheless. For now, Swiss Franc is the strongest one for today, followed by Dollar, Canadian and Yen. Aussie and Kiwi are mixed. Focuses will now turn to FOMC rate decision first, followed by BoJ, SNB and BoE tomorrow.

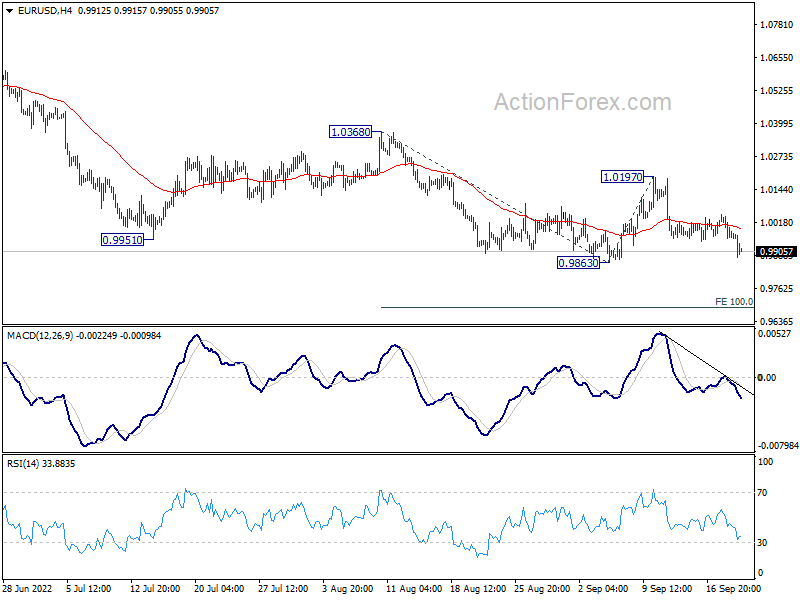

Technically, EURUSD is looking vulnerable for further selloff. Firm break of 0.9863 will resume larger down trend to 100% projection of 1.0368 to 0.9863 from 1.0197 at 0.9296 next. Such development, if happens, could also help push EUR/CHF through 0.9530 temporary low.

In Europe, at the time of writing, FTSE is up 0.58%. DAX is up 0.14%. CAC is up 0.29%. Germany 10-year yield is down -0.039 at 1.899. Earlier in Asia, Nikkei dropped -1.36%. Hong Kong HSI dropped -1.79%. China Shanghai SSE dropped -0.17%. Singapore Strait Times dropped -0.16%. Japan 10-year JGB yield rose 0.0015 to 0.261.

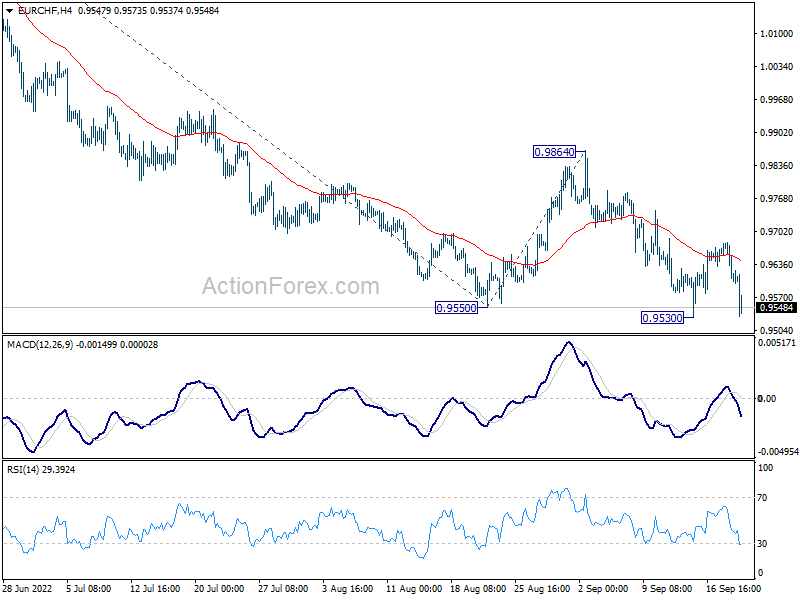

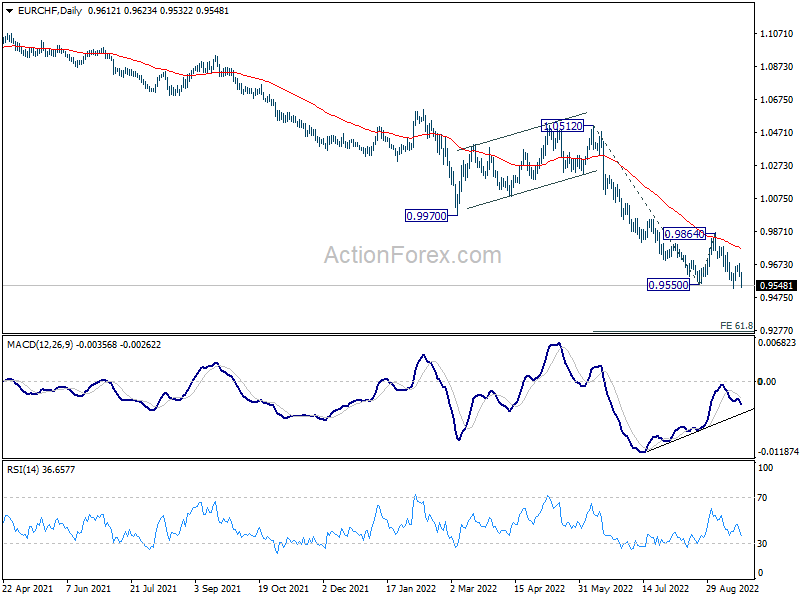

EUR/CHF holding above 0.9530 temp low after selloff

Euro drops broadly today, in particular against Swiss Franc. The selloff came after Russian President Vladimir Putin announced partial military mobilization for the invasion of Ukraine. That’s the first such mobilization since World War II, and would call up 300k reservists. Putin also warned that Russia has “various means of destruction”. “If the territorial integrity of our country is threatened, we will certainly use all the means at our disposal to protect” he said, adding that “this is not a bluff!”.

For now, EUR/CHF is still holding above 0.9530 temporary low, and down trend resumption is not confirmed yet. On break of 0.9530, EUR/CHF should target 61.8% projection of 1.0512 to 0.9550 from 0.9864 at 0.9269.

Fed to hike 75bps as 10-year yield resumed up trend

FOMC rate decision is the main focus of the day and another jumbo rate hike is expected. Based on current market pricing, there is 82% chance of a 75bps hike to 3.00-3.25%, and just 18% chance of a 100bps hike to 3.25-3.50%. Thus, there is little chance for Fed to upset the markets.

Overall rhetoric should be unchanged that tightening is set to continue while Fed is committed to bring inflation down to target. The bigger questions are on the new economic projections and the dot plot. Some hawkish surprise could be seen there, which indicates higher terminal rate for current cycle, and a longer period to stay there.

Here are some previews:

- FOMC Meeting Preview: 100bps Unlikely, But Longer Rate Hike Path in Play

- Another Fed Hike is Coming; Mind the Dots

- Is the Fed Preparing to Crash the Markets, Or Will it Give Them a Helping Hand?

- Fed Preview: Fast Pace Hiking Cycle Continues

- September Flashlight for the FOMC Blackout Period

RBA Bullock: Interest rate not yet restrictive

RBA Deputy Governor Michele Bullock said interest rate at 2.35% is not yet restrictive. But the central was already looking for opportunities to slow the pace of tightening at some point. The monthly inflation data to be released next week would have a lot of statistical noises, and would unlikely be having much impact of the deliberations at the October meeting.

Regarding the asset purchased during the pandemic bond buying program, Bullock said RBA had taken a mark-to-market valuation loss of AUD 33.9B in 2021/22. That would let the central bank in a negative net equity position of AUD 12.4B. But she added, since it has the ability to create money, the Bank can continue to meet its obligations as they become due and so it is not insolvent… The negative equity position will, therefore, not affect the ability of the Reserve Bank to do its job.”

ADB slashes developing Asia growth forecast to 4.3%, China to 3.3%

The Asian Development Bank slashed growth forecasts for developing Asia from 5.2% (April forecast) to 4.3% in 2022, and 5.3% to 4.9% in 2023. It said, “The revised outlook is shaped by a slowing global economy, the fallout from Russia’s protracted invasion of Ukraine, more aggressive monetary tightening in advanced economies, and lockdowns resulting from the People’s Republic of China’s zero-COVID policy.”

As for China, growth forecasts was downgraded sharply from 5.0% to 3.3% in 2022, and from 4.8% to 4.5% in 2023. India’s growth forecast was also cut from 7.5% to 7.0% in 2022, and from 8.0% to 7.2% in 2023.

On the other hand, inflation forecast was raised from 3.7% to 4.5% in 2022, and from 3.1% to 4.0% in 2023, “due to higher energy and food prices”.

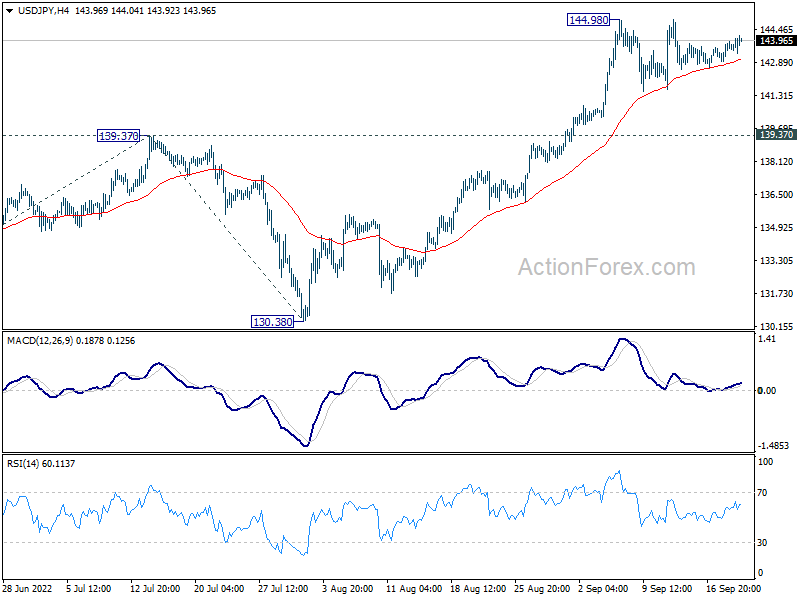

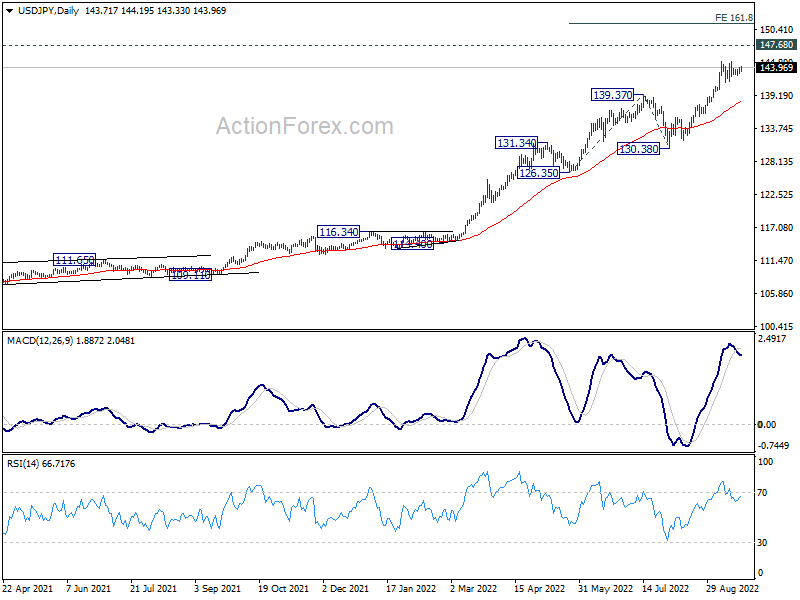

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.13; (P) 143.53; (R1) 144.11; More…

Intraday bias in USD/JPY remains neutral as sideway consolidations continues. Deeper retreat cannot be ruled out, but downside should be contained by 139.37 resistance turned support. On the upside, break of 144.98 will resume larger up trend to 147.68 long term resistance. Break there will target 161.8% projection of 126.35 to 139.37 from 130.38 at 151.44 next.

In the bigger picture, up trend from 101.18 is still in progress, as part of the whole up trend from 75.56 (2011 low). Further rise should be seen to 147.68 (1998 high). For now, break of 130.38 support is needed to be the first indication of medium term topping. Otherwise, outlook will stay bullish even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Westpac Leading Index M/M Aug | -0.10% | -0.15% | ||

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Aug | 11.1B | 7.5B | 4.2B | 2.1B |

| 14:00 | USD | Existing Home Sales Aug | 4.70M | 4.81M | ||

| 14:30 | USD | Crude Oil Inventories | 2.0M | 2.4M | ||

| 18:00 | USD | Fed Interest Rate Decision | 3.25% | 2.50% | ||

| 18:30 | USD | FOMC Press Conference |

{kind=link}