Dollar retreated notably overnight, following the rebound in US stocks and steep pull back in treasury yields. But it’s so far staying as the second strongest for the week, next to Swiss Franc, while Euro is third. Sterling stabilized further with another recovery attempt in progress. Commodity currencies are on the weaker side, with New Zealand Dollar flaring worst, while Yen is extending its pull back.

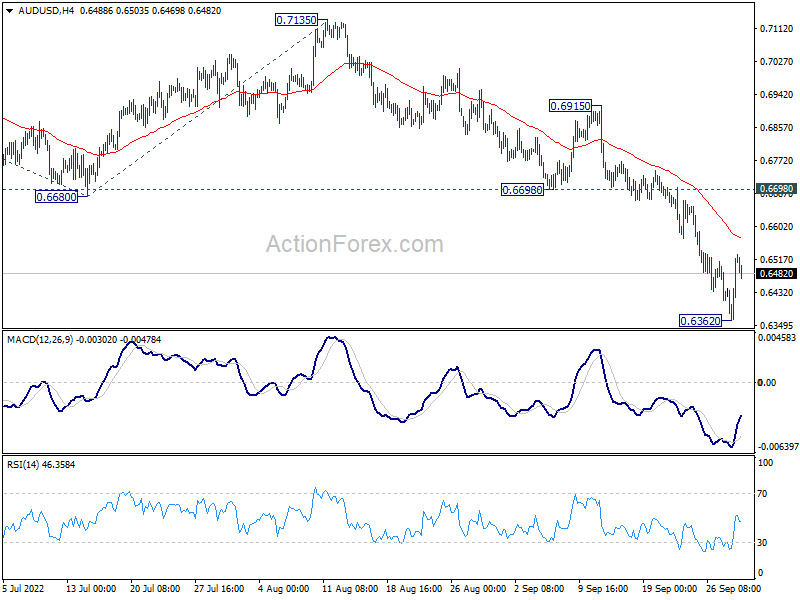

Technically, the loss of upside momentum in Dollar is becoming more apparent. Yet, there is no clear sign of reversal. At least, some levels need to be taken out to confirm short term topping in the greenback, including 0.9863 support turned resistance in EUR/USD, and 0.6698 support turned resistance in AUD/USD.

In Asia, at the time of writing, Nikkei is up 0.75%. Hong Kong HSI is up 1.19%. China Shanghai SSE is up 0.27%. Singapore Strait Times is up 0.96%. Japan 10-year yield is down -0.0019 at 0.250. Overnight, DOW rose 1.88%. S&P 500 rose 1.97%. NADSAQ rose 2.05%. 10-year yield dropped sharply by -0.259 to 3.705.

Fed Bostic wants rate at 4.25% to 4.5% by year end

Atlanta Fed President Raphael Bostic said yesterday, “the lack of progress thus far has me thinking much more now that we have to get to a moderately restrictive stance. And for me, that is in the 4.25% to 4.5% range for our policy. My preference is that we get there by year end.”

Bostic said that his expects another 75bps rate hike in November, followed by 50bps in December. But he added that “I don’t think it’ll be appropriate for us to continue to tighten and increase your rates until inflation gets to 2%. That will be guaranteeing that we’ve gone too far and we’ll take the economy into a negative space.”

“I’m still in the place of not really thinking that a recession is a foregone conclusion as we battle this,” he said. “So we can have some weakening, but I don’t think it, at this point, will take us to the historical recessionary experience.”

Fed Evans: Current interest rate not nearly restrictive enough

Chicago Fed President Charles Evans said while interest at 3-3.25% is restrictive, “with inflation as high as it is, and getting inflation under control being job one, it’s not nearly restrictive enough.”

“The risks continue to be high about more persistent inflation, and we just really need to get inflation in check,” Evans said.

Evans added that he expects interest rate to reach top by March.

Australia monthly CPI slowed to 6.8% yoy in Aug on fuel costs

In its first monthly release, Australia CPI rose 6.8% yoy in June, accelerated to 7.0% yoy in July, and slowed to 6.8% yoy in August

Monthly CPI excluding fruit, vegetables and fuel rose 5.5% yoy in June, accelerated to 6.1% yoy in July, then 6.2% yoy in August.

David Gruen, Australian Statistician, said: ” The slight fall in the annual inflation rate from July to August was mainly due to a decrease in prices for Automotive fuel. This saw the annual movement for Automotive fuel fall from 43.3 per cent in June to 15.0 per cent in August.”

New Zealand ANZ business confidence rose to -36.7, a temporary reprieve

New Zealand ANZ Business Confidence rose from -47.8 to -36.7 in September. Own Activity Outlook rose from -4.0 to -1.8. investment intentions rose from -2.0 to 1.8. Employment intentions rose from 3.4 to 5.9. Pricing intentions rose from 68.0 to 70.1. Cost expectations dropped from 90.9 to 89.8. inflation expectations eased from 6.13 % to 5.98%.

ANZ said: “It’s fair to say that demand has not yet rolled over as feared as the Reserve Bank has raised interest rates. But insofar as the RBNZ can just keep on going until they see the cooling in demand they need to tame inflation, that’s likely to be a temporary reprieve, if not an outright double-edged sword for firms that have considerable debt.”

“Inflation pressures are easing, but painfully slowly. It’s not enough for the RBNZ to see inflation pressures top out and ever so gradually fall. They will be concerned about the chance that wage and price-setting behaviour will change in structural ways that make bringing inflation down more difficult. We expect that the RBNZ will need to deliver a policy rate closer to 5% than 4% to get on top of inflation pressures.”

Looking ahead

Eurozone will release economic sentiment indicator and Germany will release CPI flash in European session. Later in the day, Canada monthly GDP, US Q2 GDP final and jobless claims will be featured.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6416; (P) 0.6473; (R1) 0.6583; More…

Intraday bias in AUD/USD is turned neutral with current recovery. Some consolidations could be seen first. But outlook will remain bearish as long as 0.6698 support turned resistance holds. Break of 0.6362 will resume larger down trend. Next target is 100% projection of 0.7660 to 0.6680 from 0.7135 at 0.6155.

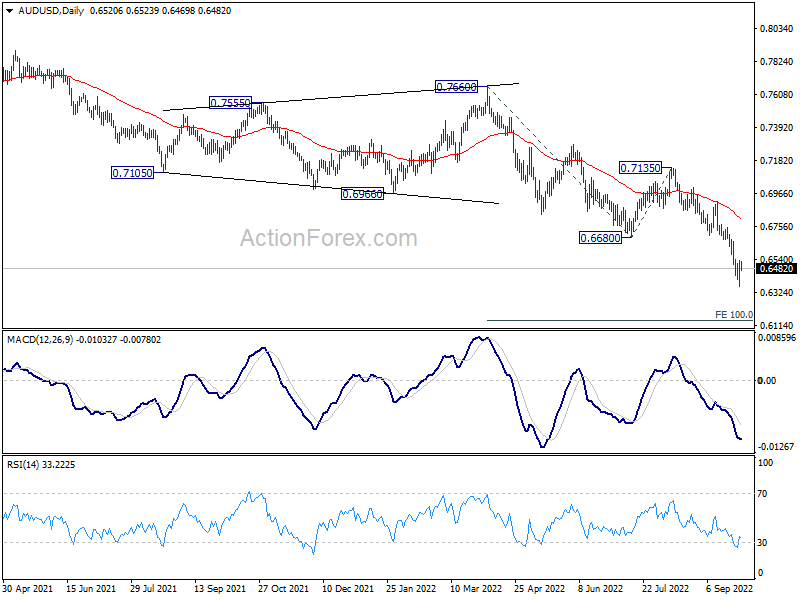

In the bigger picture, down trend form 0.8006 (2021 high) is expected to continue as long as 0.7135 resistance holds. With 61.8% retracement of 0.5506 (2020 low) to 0.8006 at 0.6461 firmly taken out, next target is 0.5506 low. Medium term momentum will now be closely monitored to gauge the chance of break of 0.5506.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Sep | 95 | 97.6 | ||

| 09:00 | EUR | Eurozone Industrial Confidence Sep | -1 | 1.2 | ||

| 09:00 | EUR | Eurozone Services Sentiment Sep | 7 | 8.7 | ||

| 09:00 | EUR | Eurozone Consumer Confidence Sep F | -28.8 | -28.8 | ||

| 12:00 | EUR | Germany CPI M/M Sep P | 1.60% | 0.30% | ||

| 12:00 | EUR | Germany CPI Y/Y Sep P | 9.50% | 7.90% | ||

| 12:30 | CAD | GDP M/M Jul | -0.10% | 0.10% | ||

| 12:30 | USD | Initial Jobless Claims (Sep 23) | 213K | 213K | ||

| 12:30 | USD | GDP Annualized Q2 F | -0.60% | -0.60% | ||

| 12:30 | USD | GDP Price Index Q2 F | 8.90% | 8.90% | ||

| 14:30 | USD | Natural Gas Storage | 103B |

{kind=link}