The forex markets are rather steady in quiet Asian session today. Dollar is paring some gains while Euro and Yen are soft too. Sterling is leading the way higher, followed by commodity currencies. But overall, almost all major pairs and crosses are bounded inside Friday’s range. The economic calendar is also rather light today. Traders might hold their bets for now, until the released of a batch of consumer inflation data from some major global economies.

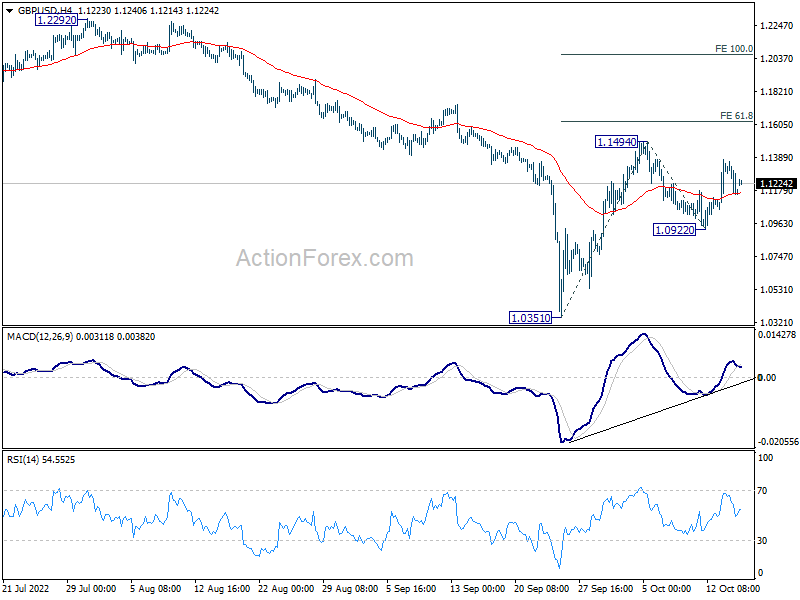

Technically, AUD/USD and USD/CAD appear to have stabilized well ahead of 0.6169 and 1.3976 respectively. It’s a sign that Dollar is losing momentum again, despite persistent strength against Yen. Some attention is now on whether the greenback’s pull back will return, in particular against Sterling. Break of 1.1494 resistance will resume GBP/USD’s rebound from 1.0351, and lead EUR/USD higher too.

In Asia, at the time of writing, Nikkei is down -1.37%. Hong Kong HSI is down -1.13%. China Shanghai SSE is down -0.10%. Singapore Strait Times is down -1.15%. Japan 10-year JGB yield is down -0.0035 at 0.250.

BoE Bailey: Inflationary pressures will require a stronger response

BoE Governor Andrew Bailey indicated over the weekend that a larger rate hike could be delivered at the upcoming meeting in November. He said, “we will not hesitate to raise interest rates to meet the inflation target… And, as things stand today, my best guess is that inflationary pressures will require a stronger response than we perhaps thought in August.”

Regarding new Finance Minister Jeremy Hunt, he said, “I can tell you that there was a very clear and immediate meeting of minds between us about the importance of fiscal sustainability and the importance of taking measures to do that.”

Japan Suzuki: Will take decisive action on excessive volatility

There is no clear sign of intervention by Japan so far, as USD/JPY is trading in tight range close to 32-yr high. Finance Minister Shunichi Suzuki just said, “if we see excessive volatility caused by speculative moves, we will take decisive action. There is no change in this view at all.”

Separately, BoJ Governor Haruhiko Kuroda said in a parliamentary session, Japan’s economy is in the midst of recovery from COVID-19. Higher commodity prices, on the back of the situation in Ukraine, have been leading to an outflow of income from Japan to overseas, adding downward pressure on the economy.”

“For now, we think it appropriate to continue with monetary easing because it’s necessary to support the economy and achieve our inflation target in a sustainable and stable fashion accompanied by wage growth,” he added.

NZ BNZ services dropped to 55.8 in Sep

New Zealand BusinessNZ Performance of Services Index dropped from 58.6 to 55.8 in September. Looking at some details, activity/sales dropped from 67.5 to 59.2. Employment ticked down from 50.7 to 50.5. New orders/business dropped from 66.6 to 62.9. Stocks/inventories dropped from 59.6 to 54.9. Supplier deliveries was unchanged at 49.7.

BNZ Senior Economist Craig Ebert said that “the composite PCI held together at 54.4 in free-weighted terms, while the GDP weighted composite came in at 55.4, from 58.2 in August. These marry with our view that Q3 GDP increased about 1.0%”.

CPI, retail sales, and consumer confidence for the week

Consumers are the focuses this week with CPI from UK, Canada, Japan and New Zealand. Retail sales from the UK and Canada will be released, while UK will also publish Gfk consumer confidence. Additionally, Germany ZEW, Australia employment will be closely watched, together with GDP from China.

Here are some highlights for the week:

- Monday: New Zealand BusinessNZ Services, Japan tertiary industry index; US Empire state manufacturing, BoC business outlook survey.

- Tuesday: New Zealand CPI; RBA minutes; China GDP, retail sales, industrial production, fixed asset investment; Germany ZEW; Canada housing starts; US industrial production, NAHB housing index.

- Wednesday: UK CPI, PPI; Eurozone CPI final; Canada CPI, IPPI, RMPI; US housing starts and building permits, Fed’s Beige Book report.

- Thursday: Japan trade balance; Australia employment, NAB quarter business confidence; Swiss trade balance; Germany PPI, Eurozone current account; US Philly Fed manufacturing, jobless claims, existing home sales.

- Friday: New Zealand trade balance; Japan CPI; UK Gfk consumer confidence, retail sales, public sector net borrowing; Canada retail sales, new housing price index, Eurozone consumer confidence.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6206; (P) 0.6261; (R1) 0.6352; More…

Intraday bias in AUD/USD remains neutral for the moment. Further decline is expected as long as 0.6362 support turned resistance holds. Firm break of 100% projection of 0.7660 to 0.6680 from 0.7135 at 0.6155 will target 138.2% projection at 0.5781. Nevertheless, break of 0.6362 will indicate short term bottoming, on bullish convergence condition in 4 hour MACD, and bring stronger rebound back to 0.6539 resistance.

In the bigger picture, down trend form 0.8006 (2021 high) is expected to continue as long as 0.6680 support turned resistance holds. Next target is 0.5506 low. Medium term momentum will now be closely monitored to gauge the chance of break of 0.5506.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PSI Sep | 55.8 | 58.6 | ||

| 23:01 | GBP | Rightmove House Price Index M/M Oct | 9 | 0.70% | ||

| 04:30 | JPY | Tertiary Industry Index M/M Aug | 0.70% | 0.40% | -0.60% | |

| 04:30 | JPY | Industrial Production M/M Aug F | 3.40% | 2.70% | 2.70% | |

| 12:30 | USD | Empire State Manufacturing Index Oct | -1 | -1.5 | ||

| 14:30 | CAD | BoC Business Outlook Survey |

{kind=link}