Euro is lifted slightly by hawkish comments from ECB officials, as well as the meeting accounts. But overall, it’s risk-on sentiment that matters more for now, supporting Yen and Dollar too. Commodity currencies are so far the worst performers, with Aussie also weighed down by poor job data. Sterling and Swiss Franc are currently mixed.

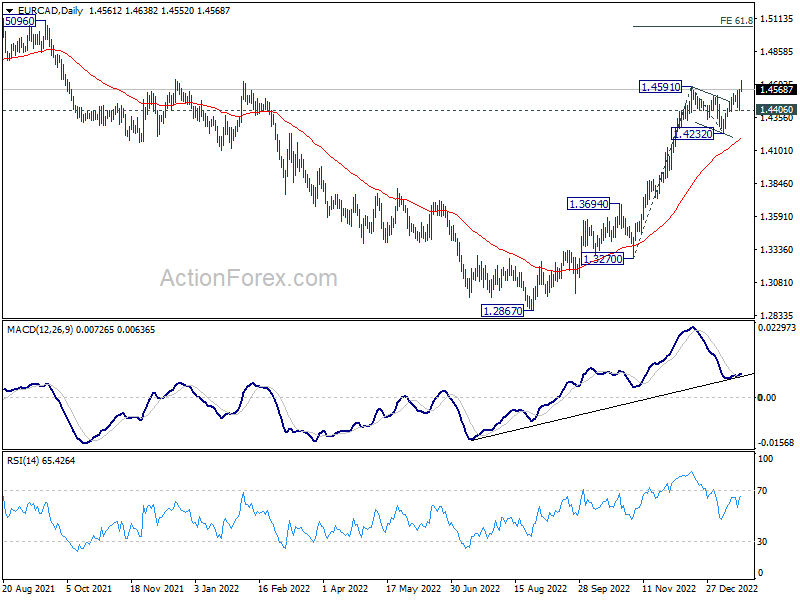

Technically, EUR/CAD finally breaks through 1.4591 resistance to resume larger up trend from 1.2867. Further rally is now expected as long as 1.4406 support holds. Next target is 61.8% projection of 1.3270 to 1.4591 from 1.4232 at 1.5048. Let’s see if USD/CAD could also pick up momentum towards 1.3704 resistance.

In Europe, at the time of writing, FTSE is down -1.20%. DAX is down -1.69%. CAC is down -1.81%. Germany 10-year yield is up 0.063 at 2.088. Earlier in Asia, Nikkei dropped -1.44%. Hong Kong HSI dropped -0.12%. China Shanghai SSE rose 0.49%. Singapore Strait Times dropped -0.41%. Japan 10-year JGB yield dropped -0.0184 to 0.404.

US initial jobless claims dropped to 190k

US initial jobless claims dropped -15k to 190k in the week ending January 14, better than expectation of 212k. Four-week moving average of initial claims decreased 6.5k to 206k.

Continuing claims rose 17k to 1647k in the week ending January 7. Four-week moving average of continuing claims declined 5.5k to 1673k.

Also from the US, Philly Fed survey improved from -13.7 to -8.9 in January.

BoE Bailey: We don’t target a particular peak interest rate

BoE Governor Andrew Bailey said two months of decline in headline inflation is “the beginning of a sign that a corner has been turned.” He said: “What we think is the most likely outcome is that it will fall quite rapidly this year, probably starting in the late spring and that has a lot to do with energy pricing.

On the outlook for the base rate, he said: “We don’t target a particular peak”. Market curve was out of line back in November, because of UK risk premium in there following the events of September and October

“If you go back to the height of that period, the peak of what the market thought we were going to get to was over 6%, but the time we did our forecast in November it was 5.2%, it is now down to 4.5%. Now I am not endorsing 4.5%, but what you may have noticed in December is that we did not include the comment that we made in November about the market being in our view rather out of line,” he said.

ECB accounts: Less frontloaded but steadier approach consistent with persistent inflation process

In the accounts of ECB’s December meeting, it’s noted that a “large number” of members “initially” expressed preference for a 75bps hike. But some of them expressed their willingness to agree on a 50bps if the majority were to support Chief Economist Philip Lane’s proposal.

That is, to rate interest rates by 50bps and to communicate that interest rates would “still have to rise significantly at a steady pace to reach levels that were sufficiently restrictive”. Meanwhile, 50bps hikes was “judged to constitute an appropriate pace”.

Also, “a less frontloaded but steadier approach to bringing interest rates to restrictive levels could be seen as consistent with the more persistent nature of the inflation process and continued elevated uncertainty…

Nevertheless, some member still held the view that “the proposed adjustment of the monetary policy stance was insufficient – even taking into account the combination of a 50 basis point interest rate hike with the announcement of a reduction in APP reinvestments.”

ECB Lagarde: Inflation is way too high, we should stay the course

ECB President Christine Lagarde said in Davos today, “Inflation by all accounts, whichever way you look at it, is way too high.”

“There is determination at the ECB to bring (inflation) back in a timely manner and we should stay the course until we have been in restrictive territory for long enough to bring it down,” Lagarde added.

“The job market in Europe has never been as vibrant as it is now. The unemployment number is at rock bottom compared with what we’ve had in the last 20 years. And the participation rate which matters as well, is also very, very high level and that is pretty much homogeneous throughout the euro area,” she said.

“The news has been much more positive over the past few weeks,” she said. “It will not be a brilliant year (in 2023), but a lot better than feared”.

ECB Knot: Don’t assume that it’s a one-shot 50; it’s more than that

ECB Governing Council member Klaas Knot told CNBC today, “Our president has already announced that most of the ground that we have to cover we will cover at a constant pace of multiple 50 basis-point hikes”

“So we will continue that at a steady pace. Based on the information that we have available today, that predicates another 50-basis-point rate hike at our next meeting, and possibly at the one after that, and possibly thereafter, but everything will also be determined by the review of data. So don’t assume that it’s a one-shot 50; it’s more than that,” he added.

Referring to recent market speculations that ECB will slow down rate hikes in March, Knot said, “The sort of market developments that I’ve seen over the last two weeks or so, are not entirely welcome… I don’t think that they are compatible, actually, with a timely return of inflation towards 2%.”

“Core inflation shows no signs of abating,” Knot said. “I would first need to see different dynamics in core inflation before I could start thinking about a more equal balance of risk.”

Japan exports up 11.5% yoy in Dec, imports up 20.6% yoy

In December, Japan exports rose 11.5% yoy to JPY 8787B, marking the slowest growth rate in 2022. Exports to China fell -6.2% yoy in value and down -24% yoy in volume. Imports rose 20.6% yoy to JPY 10236B, led by oil, coal and liquefied natural gas.

Trade deficit came to JPY -1.45T, extending the run of deficits to 17 months. For the whole of 2022, trade balance came in at JPY -19.97T deficit, the second straight annual shortfall, and the largest since 1979.

In seasonally adjusted term, exports dropped -3.5% mom to JPY 8352B. Imports dropped -3.4% mom to JPY 10076B. Trade deficit narrowed slightly to JPY -1.72T, larger than expectation of JPY -1.63T.

Australia employment down -14.6k in Dec, unemployment rate unchanged at 3.5%

Australia employment declined -14.6k in December, much worse than expectation of 21.2k growth. Full-time jobs rose 17.6k while part-time jobs fell -32.2k. Unemployment rate was unchanged at 3.5%. Participation rate dropped -0.2% to 66.6%. Monthly hours worked dropped -0.5%.

Lauren Ford, head of labour statistics at the ABS, said: “The falls in employment and hours worked in December followed strong growth through 2022, with an annual employment growth rate of 3.4 per cent and hours worked increasing by 3.2 per cent.

“The strong employment growth through 2022, along with high participation and low unemployment, continues to reflect a tight labour market.

“In December, we saw the number of people working reduced hours due to illness increasing by 86,000 to 606,000, which is over 50 per cent higher than we would usually see at this time of the year.”

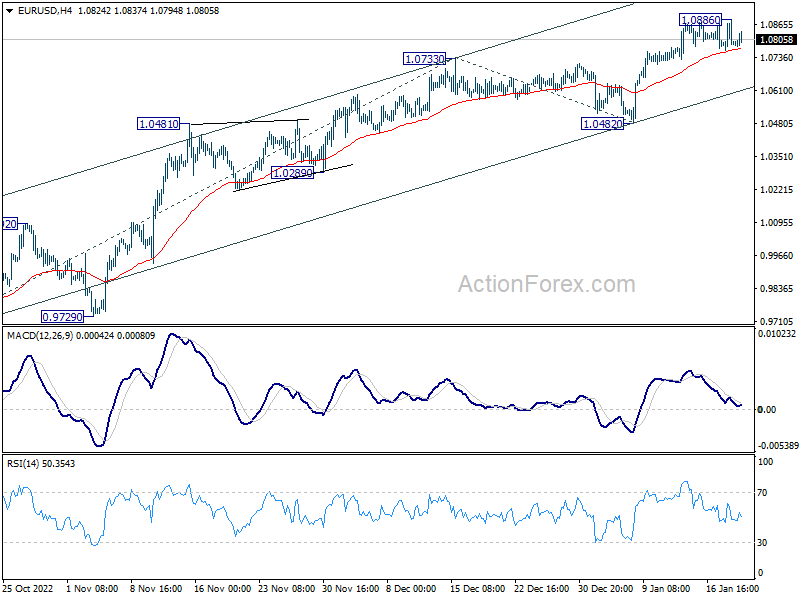

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0745; (P) 1.0816; (R1) 1.0866; More…

EUR/USD is still bounded in consolidation from below 1.0886 and intraday bias stays neutral. Overall outlook will remain bullish as long as 1.0482 support holds. Break of 1.0886 will resume rally from 0.9534 to 61.8% projection of 0.9630 to 1.0733 from 1.0482 at 1.1164 next.

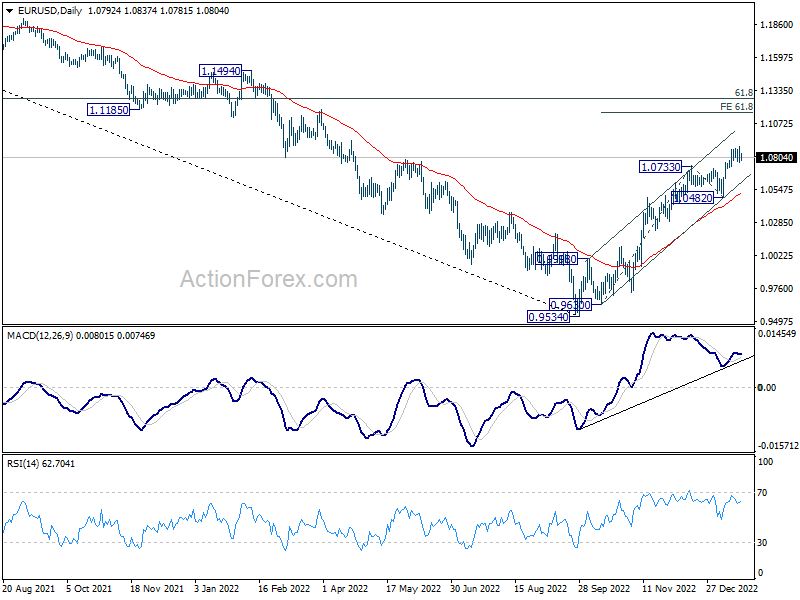

In the bigger picture, current development suggests that the rally from 0.9534 low (2022 low) is a medium term up trend rather than a correction. Further rally is in favor to 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 next. This will remain the favored case as long as 1.0482 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (JPY) Dec | -1.72T | -1.63T | -1.73T | -1.78T |

| 00:01 | GBP | RICS Housing Price Balance Dec | -42% | -30% | -25% | -26% |

| 00:30 | AUD | Employment Change Dec | -14.6K | 21.2K | 64.0K | 58.3K |

| 00:30 | AUD | Unemployment Rate Dec | 3.50% | 3.40% | 3.40% | 3.50% |

| 07:30 | CHF | Producer and Import Prices M/M Dec | -0.70% | -0.40% | -0.50% | |

| 07:30 | CHF | Producer and Import Prices Y/Y Dec | 3.20% | 3.10% | 3.80% | |

| 09:00 | EUR | Eurozone Current Account (EUR) Nov | 13.6B | -11.6B | -0.4B | |

| 12:30 | EUR | ECB Meeting Accounts | ||||

| 13:30 | CAD | Wholesale Sales M/M Nov | 0.50% | 2.00% | 2.10% | 1.90% |

| 13:30 | USD | Initial Jobless Claims (Jan 13) | 190K | 212K | 205K | |

| 13:30 | USD | Building Permits Dec | 1.33M | 1.37M | 1.34M | 1.351M |

| 13:30 | USD | Housing Starts Dec | 1.382M | 1.36M | 1.43M | 1.401M |

| 13:30 | USD | Philadelphia Fed Manufacturing Survey Jan | -8.9 | -11.2 | -13.8 | -13.7 |

| 15:30 | USD | Natural Gas Storage | -76B | 11B | ||

| 16:00 | USD | Crude Oil Inventories | -2.1M | 19.0M |

{kind=link}