Australian Dollar recovered broadly today following hawkish RBA rate hike, which signals more tightening ahead. The rebound in Aussie also takes New Zealand Dollar higher. On the other hand, Dollar is once again consolidating overnight gains. The rally in the greenback is not too committed this week so far. But Fed Chair Jerome Powell’s speech later today has the potential to trigger some fireworks. European majors are on the softer side, with Sterling having a slight upper hand. But Yen is the worst performer for the week.

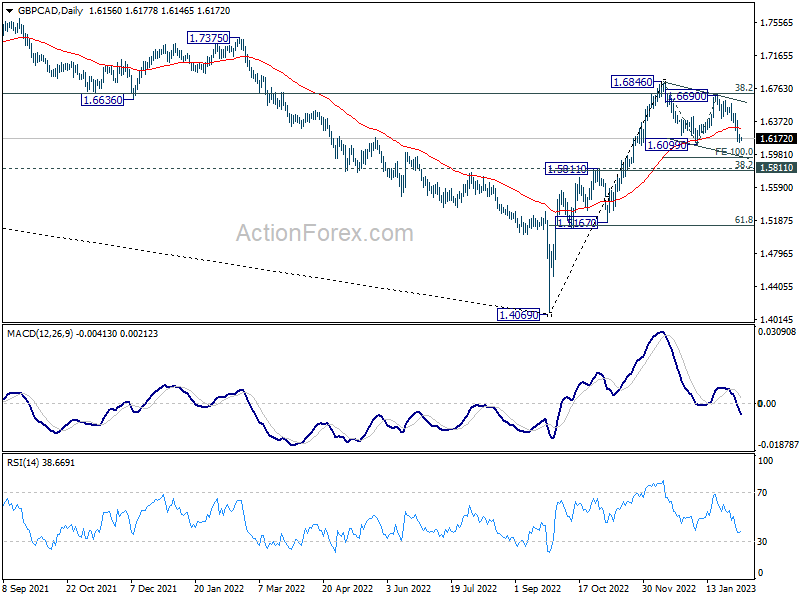

Technically, GBP/CAD is on the verge of breaking through 1.6099 to resume the whole correction from 1.6846. 100% projection of 1.6846 to 1.6099 from 1.6690 at 1.5934 is the target. However, a strong cluster support level lies ahead at 1.5811, 38.2% retracement of 1.4069 to 1.6846 at 1.5785. So, the dip below 1.5934 could be seen as a buying opportunity with stop below 1.5785. Let’s see how it goes.

In Asia, Nikkei is down -0.04%. Hong Kong HSI is up 0.30%. China Shanghai SSE is down -0.08%. Singapore Strait Times is down -0.22%. Japan 10-year JGB yield is down -0.0003 at 0.500. Overnight, DOW dropped -0.10%. S&P 500 dropped -0.61%. NASDAQ dropped -1.00%. 10-year yield rose 0.102 to 3.634.

RBA hikes 25bps, further increases needed over the months ahead

RBA raises the cash rate target by 25bps to 3.35% as widely expected. The Board also expects that “further increases in interest rates will be needed over the months ahead”. To assess “how much” further hike is needed, close attention will be paid to “developments in the global economy, trends in household spending and the outlook for inflation and the labour market.”

The central noted that underlying inflation at 6.9% in December was “high than expected” with “strong domestic demand “adding to the inflationary pressures in a number of areas of the economy.” Inflation is expected to decline to 4.75% this year, then to around 3% by mid-2025. Medium-term inflation expectation remain” well anchored”.

GDP growth is expected to slow to 1.50% in 2023 and 2024. Unemployment rate is projected to rise form current 3.50% to 3.75% by the end of 2023, and then 4.50% by mid-2025.

BoE Pill more concerned about the potential persistence of inflation

BoE Chief Economist Huw Pill said yesterday, “I do have high degree of confidence (about getting inflation to target) because we know what we’re going to do. We’ve done a lot to achieve it, we’re prepared to do more as necessary to ensure that we achieve it sustainably.”

He also said the BoE had to “guard against doing too much” given the typical 18-month lag for rate hikes to impact the economy. “We are reaching the point where those types of concerns are in the forefront of our minds,” he said. “But if you ask me where we are at the moment, I think we are still more concerned about the potential persistence of inflation.”

Inflation pressure in the labor market “probably tilts us to saying we haven’t quite got to the point where we’re confident to engage in a discussion of a turning point in rates.”

Fed Bostic: Strong job data probably translate into more rate hikes than projected

Atlanta Fed President Raphael Bostic told Bloomberg News yesterday, last week’s strong non-farm payroll report will probably mean we have to do a little more work… And I would expect that that would translate into us raising interest rates more than I have projected right now.”

Bostic previously indicated that he expects interest rate to peak at 5.00-5.25% to get policy sufficiently restrictive. Rate would then stay there throughout 2024. To him, a hike peak could come through an additional quarter-point hike after the two currently envisaged, without ruling out a half-point hike.

He expects inflation to be in the “low 3s” this year, still well above Fed’s 2% target. “Those last few tenths of a point can take a long time to be realized,” he said. “And so I want to make sure that we are in the right place before we start easing off our policy because the most important thing at this stage is to get our price stability measure as close to target as possible.”

Looking ahead

Swiss unemployment rate and foreign currency reserve, Germany industrial production, France trade balance will be released in European session. Later in the day, both Canada and US will publish trade balance.

AUD/USD Daily Report

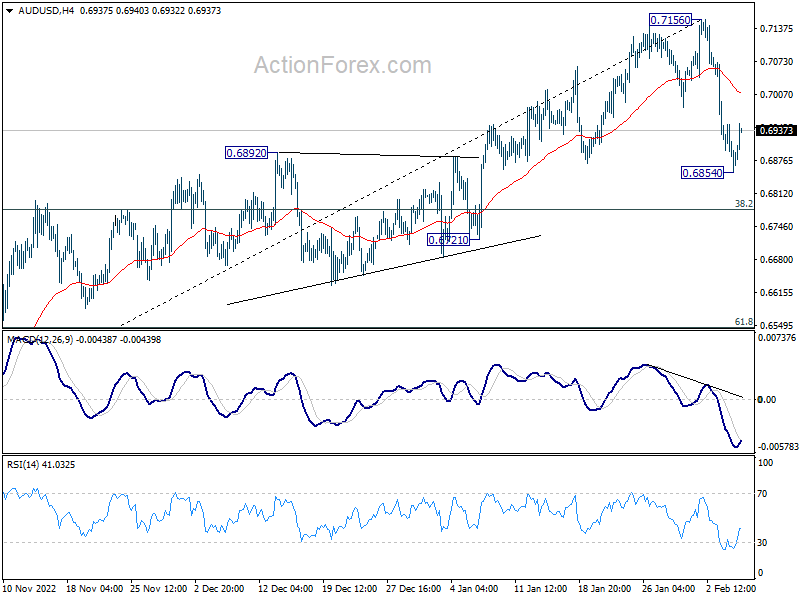

Daily Pivots: (S1) 0.6844; (P) 0.6896; (R1) 0.6937; More…

Intraday bias in AUD/USD is turned neutral first with current recovery. Correction from 0.7156 could still extend lower. But downside should be contained by 38.2% retracement of 0.6169 to 0.7156 at 0.6779 to bring rebound. For now, break of 0.7156 is not expected soon, as correction from there should extend for a while.

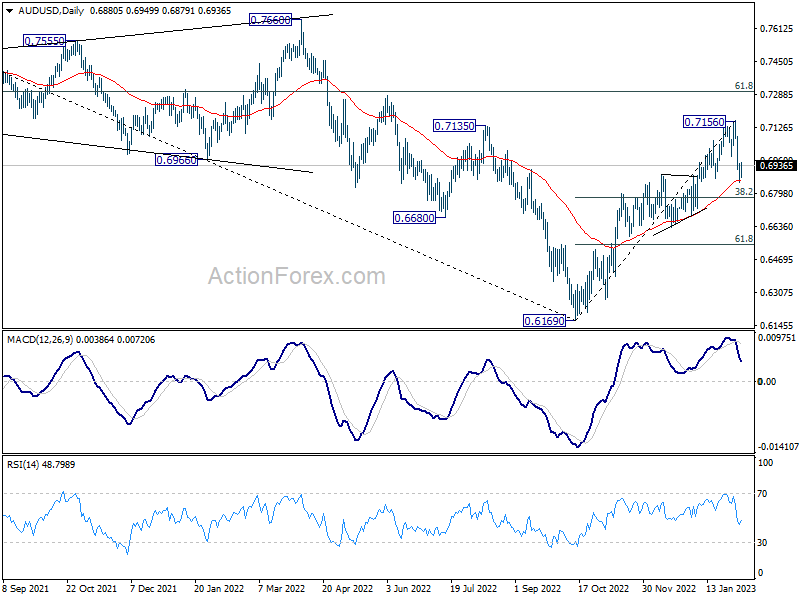

In the bigger picture, corrective decline from 0.8006 (2021 high) should have completed with three waves down to 0.6169 (2022 low). Further rally should be seen to 61.8% retracement of 0.8006 to 0.6169 at 0.7304. Sustained break there will pave the way to retest 0.8006. This will now remain the favored case as long as 0.6721 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Dec | 4.80% | 2.50% | 0.50% | 1.90% |

| 23:30 | JPY | Household Spending Y/Y Dec | -1.30% | -0.20% | -1.20% | |

| 03:30 | AUD | RBA Rate Decision | 3.35% | 3.35% | 3.10% | |

| 00:30 | AUD | Trade Balance (AUD) Dec | 12.24B | 12.2B | 13.20B | 13.48B |

| 05:00 | JPY | Leading Economic Index Dec P | 97.2 | 97.2 | 97.4 | |

| 06:45 | CHF | Unemployment Rate Jan | 1.90% | 1.90% | ||

| 07:00 | EUR | Germany Industrial Production M/M Dec | -0.60% | 0.20% | ||

| 07:45 | EUR | France Trade Balance (EUR) Dec | -12.2B | -13.8B | ||

| 08:00 | CHF | Foreign Currency Reserves (CHF) Jan | 784B | |||

| 13:30 | CAD | International Merchandise Trade (CAD) Dec | -0.6B | 0.0B | ||

| 13:30 | USD | Trade Balance (USD) Dec | -68.5B | -61.5B |

{kind=link}