Risk aversion is intensifying as US stocks tumbled significantly overnight, following First Republic Bank’s earnings report, which reignited concerns about the broader banking sector. The troubled regional bank’s shares plummeted by nearly half. Concurrently, bonds surged higher, pushing 10-year yield below 3.4% handle. Japanese Yen and Swiss Franc surged following the shift in sentiment, trailed by Dollar.

Meanwhile, Australian Dollar led the decline, as it was further pressured by plunging Copper prices. Aussie could be ready to break through 2023 low against the greenback. Canadian Dollar followed as the second worst performer, with Sterling following. Euro is mixed as partly supported by hawkish comments by ECB officials.

Technically, it appears that NASDAQ’s rebound from 10,982.80 has peaked at 12,245.42, just ahead of 12,269.55 resistance. Immediate focus returns to 55 D EMA (now at 11,779.21). Sustained break there could prompt deeper decline back towards 10,982.80 support. As long as 10,982.80 support holds, outlook would be more neutral than bearish, with another rise through 12,269.55 remaining slightly in favor. However, firm break below 10,982.80 could signal that larger downtrend from 2021 high of 16,212.22 is resuming through 10,088.82 low.

In Asia, at the time of writing, Nikkei is down -0.92%. Hong Kong HSI is up 0.59%. China Shanghai SSE is down -0.31%. Singapore Strait Times is down -0.15%. Japan 10-year JGB yield is down -0.015 at 0.465. Overnight DOW dropped -1.02%. S&P 500 dropped -1.58%. NASDAQ dropped -1.98%. 10-year yield dropped sharply by -0.119 to 3.396.

BoE Pill: We’ve had a series of transitory inflation shocks one after the other

In an interview on the “Beyond Unprecedented” podcast produced by Columbia University’s law school, BoE Chief Economist Huw Pill reiterated the central bank’s official forecast, stating that some factors maintaining high inflation are likely to recede in the upcoming months and that inflation could fall below the 2% target in the next few years.

Discussing the continuous inflationary shocks faced by the UK, Pill said, “We’ve had a series of inflation shocks that just come one after the other.” He added, “Each of those shocks was in itself transitory, but they just were timed in a way that inflation never dissipated.”

Pill emphasized the need for UK citizens to accept being worse off and to refrain from trying to maintain their real spending power by driving up prices through higher wages or passing on energy costs to customers. Pill observed, “What we’re facing now is that reluctance to accept that, yes, we’re all worse off and have to take our share.”

He also highlighted the UK’s status as a major net importer of natural gas and the resulting challenges, noting, “The UK, which is a big net importer of natural gas, is facing a situation that the price of what you’re buying from the rest of the world has gone up a lot, relative to the price of what you’re selling to the rest of the world, which is mainly services in the case of the UK.”

Pill concluded, “If what you’re buying has gone up a lot relative to what you’re selling, you’re going to be worse off.”

BoJ Ueda: Dealing with cost-push inflation is very difficult

In an address to parliament today, BoJ Governor Kazuo Ueda highlighted the difficulties central banks face when dealing with cost-push inflation.

Ueda explained, “In general, dealing with cost-push inflation is very difficult for central banks. On the one hand, you’d like to curb inflation. On the other hand, you don’t want to tighten monetary policy knowing that cost-push inflation will cool the economy.”

The governor emphasized the importance of striking the right balance, which he said, “depends on economic developments at the time, including where inflation stood at the outset.”

Ueda also noted that cost-push inflation in Japan is likely to ease as prices of imported raw materials have probably peaked.

These comments come ahead of BoJ’s two-day policy meeting starting on Thursday, during which the central bank is widely anticipated to maintain its ultra-loose monetary policy.

Australia CPI down to 7.0% yoy in Q1, 6.3% yoy in Mar

Australia CPI slowed from 7.8% yoy to 7.0% yoy in Q1, slightly above expectation of 6.9% yoy. For the quarter, CPI rose 1.4% qoq, down from prior 1.9% qoq, below expectation of 1.3% qoq. Trimmed mean CPI rose 1.2% qoq, 6.6% yoy while weighted median CPI rose 1.2% qoq, 5.8% yoy.

Michelle Marquardt, ABS head of prices statistics, said “CPI inflation slowed in the March quarter, with the quarterly rise being the lowest since December 2021. While prices continued to rise for most goods and services, many of these increases were smaller than they have been in recent quarters.”

Monthly CPI slowed from 6.8% yoy to 6.3% yoy in March, below expectation of 6.5% yoy. Excluding volatile items (Fruit and vegetables and Automotive fuel) CPI, rose from 6.8% yoy to 6.9% yoy.

NZ imports surged 10% yoy, export rose 0.6% yoy in Mar

New Zealand goods exports rose 0.6% yoy or NZD 40m to NZD 6.5B in March. Imports rose 10% yoy or NZD 719m to NZD 7.8B. Monthly trade balance recorded a deficit of NZD -1.3B, larger than expectation of NZD -0.5B.

Australia contributed the most to the growth in monthly exports, with a 30% rise. Goods exports to the US was up 4.1%, EU up 28%, but down -9.6% to Japan and down -5.7% to China.

On the other hand, imports from the US leads the monthly rise, up 39%. Imports from EU and South Korea grew 24% and 20% respectively. On the other hand, imports from China was down -13%, Australia down -4.0%.

Looking ahead

Germany Gfk consumer confidence and Swiss Credit Suisse economic expectations will be released in European session. Later in the day, US will publish durable goods orders and goods trade balance.

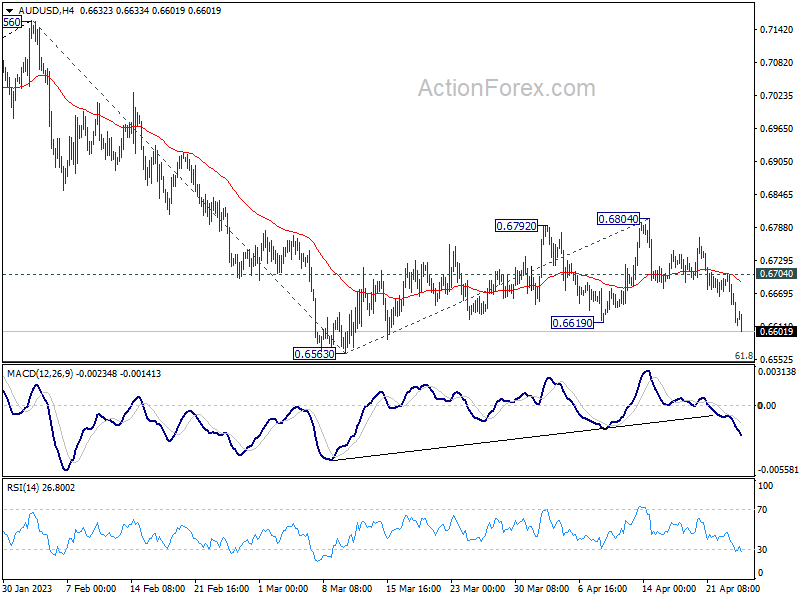

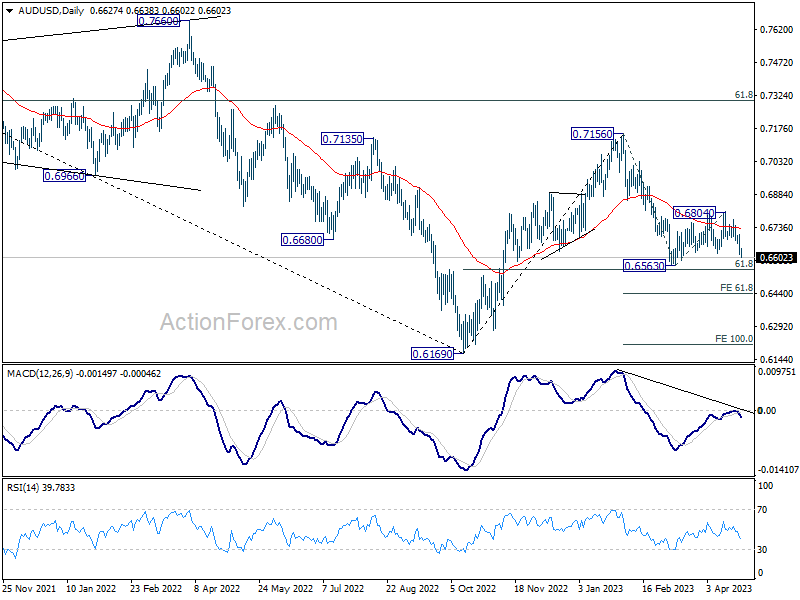

AUD/USD Daily Report

Daily Pivots: (S1) 0.6592; (P) 0.6649; (R1) 0.6683; More…

AUD/USD’s break of 0.6619 support argues that consolidation pattern from 0.6563 has completed at 0.6804, and larger fall from 0.7156 is ready to resume. Intraday bias is now on the downside for 0.6563 support first. Firm break there should bring deeper decline through 0.6546 fibonacci level to 61.8% projection of 0.7156 to 0.6563 from 0.6804 at 0.6438 next. On the upside, though, above 0.6704 minor resistance will delay the bearish case and turn intraday bias neutral first.

In the bigger picture, as long as 61.8% retracement of 0.6169 to 0.7156 at 0.6546 holds, the decline from 0.7156 is seen as a correction to rally from 0.6169 (2022 low) only. Another rise should still be seen through 0.7156 at a later stage. However, sustained break of 0.6546 will raise the chance of long term down trend resumption through 0.6169 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Mar | -500M | -714M | ||

| 01:30 | AUD | Monthly CPI Y/Y Mar | 6.30% | 6.50% | 6.80% | |

| 01:30 | AUD | CPI Q/Q Q1 | 1.40% | 1.30% | 1.90% | |

| 01:30 | AUD | CPI Y/Y Q1 | 7.00% | 6.90% | 7.80% | |

| 01:30 | AUD | RBA Trimmed Mean CPI Q/Q Q1 | 1.20% | 1.40% | 1.70% | |

| 01:30 | AUD | RBA Trimmed Mean CPI Y/Y Q1 | 6.60% | 7.20% | 6.90% | |

| 06:00 | EUR | Germany Gfk Consumer Confidence May | -27.5 | -29.5 | ||

| 08:00 | CHF | Credit Suisse Economic Expectations Apr | -41.3 | |||

| 12:30 | USD | Goods Trade Balance (USD) Mar P | -89.8B | -91.6B | ||

| 12:30 | USD | Wholesale Inventories Mar P | -0.20% | 0.10% | ||

| 12:30 | USD | Durable Goods Orders Mar | 0.80% | -1.00% | ||

| 12:30 | USD | Durable Goods Orders ex Transport Mar | -0.20% | -0.10% | ||

| 14:30 | USD | Crude Oil Inventories | -1.3M | -4.6M |

{kind=link}