Euro and British Pound face some downward pressure today, following dismal PMI data that raises concerns about the prospect of further economic contraction in Eurozone and UK. With the German Ifo business climate index on the horizon tomorrow and ECB rate decision due on Thursday, Euro is likely to face additional scrutiny.

Meanwhile, Dollar seems to be in a marginally better position than both the Euro and Sterling. However, it’s worth noting that the Greenback is currently seeing a lack of dedicated buying interest. On the other hand, in an interesting twist, Japanese Yen is making a comeback, bolstered by the decline in US and European benchmark treasury yields.

As for commodity currencies, New Zealand and Canadian Dollars appear to be leading the pack. However, Australian Dollar is noticeably lagging behind. Swiss Franc, while performing well against its European counterparts, presents a mixed picture overall.

Technically, Bitcoin’s break of 55 DMA should confirm short term topping at 31815. Risk will now stay on the downside as long as 30337 resistance holds. Deeper fall should be seen to trend support support at around 26500. While it’s premature to conclude that the corrective rebound from 15,452 has run its course, bearish divergence observed in D MACD is a cautionary signal.

In Europe, at the time of writing, FTSE is down -0.23%. DAX is down -0.12%. CAC is down -0.53%. Germany 10-year yield is down -0.089 at 2.407. Earlier in Asia, Nikkei rose 1.23%. Hong Kong HSI fell -2.13%. China Shanghai SSE dropped -0.11%. Singapore Strait Times dropped -0.40%. Japan 10-year JGB yield dropped -0.0148 to 0.451.

UK PMI composite fell to 50.7, reigniting recession fears

UK’s economic landscape appears increasingly precarious, as evidenced by disappointing July PMI readings. Manufacturing PMI plunged to a 38-month low of 45.0, from 46.5 and underperforming expectation of 46.1. the Services PMI dipped to a 6-month low of 51.5, falling short of the anticipated 53.1, and down from 53.7. Composite PMI, encapsulating both sectors, dropped to a 6-month low of 50.7 from 52.8.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, expressed significant concern over these figures. “The UK economy has come close to stalling in July which, combined with gloomy forward-looking indicators, reignites recession worries,” he noted. “July’s flash PMI survey data revealed a deepening manufacturing downturn accompanied by a further cooling of the recent resurgence of growth in the service sector.”

Further bolstering this pessimistic outlook, forward-looking indicators, such as order book inflows, levels of work-in-hand, and future business expectations, suggest a potential weakening of growth in the coming months. Williamson warned, “these all point to growth weakening further in the months ahead, adding to a risk of GDP falling in the third quarter.”

While this decline in growth and demand paints a gloomy picture, there’s a silver lining in the form of cooling inflationary pressures. “Although ongoing upward wage pressures mean service sector price growth remains elevated, the survey data signal further, potentially marked, falls in consumer price inflation in the months ahead,” added Williamson.

Eurozone PMI manufacturing down o 38-mth low, PMI services at 6-mth low

Eurozone’s economic outlook appears increasingly gloomy as latest PMI readings for manufacturing and services sectors disappoint, suggesting further contraction may lie ahead. Manufacturing PMI declined to 42.7 in July from 43.4, a 38-month low and below expectations of 43.5. Simultaneously, Services PMI dropped to a 6-month low of 51.1, short of the projected 51.5, and down from 52.0. Composite PMI, reflecting both sectors, sank to an 8-month low of 48.9, down from 49.9.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, expressed his concern, stating, “Manufacturing continues to be the Achilles heel of the eurozone. Producers have cut their output again at an accelerated pace in July, while the services sector’s activity is still expanding, though at a much slower rate than earlier in the year.” He further warned, “The eurozone economy will likely move further into contraction territory in the months ahead, as the services sector keeps losing steam.”

This less than encouraging data will surely unsettle ECB, as cost pressures in the private sector remain persistent, particularly in the substantial services sector. “The latest PMI reading is not going to please ECB officials…Thus, ECB president Christine Lagarde will certainly stick to her guns and hike interest rates by 25 bp at the next monetary meeting at the end of July,” de la Rubia explained.

Meanwhile, France’s manufacturing PMI slid to a 38-month low at 44.5, down from 46.0, while its services PMI fell to 47.4, a 29-month low, from 48.0. The composite PMI followed suit, dropping to a 32-month low at 46.6, down from 47.2.

Germany’s manufacturing PMI took a dive from 40.6 to 38.8, also a 38-month low. Services declined to a 5-month low at 52.0 from 54.1, and the composite PMI fell to an 8-month low of 48.3, down from 50.6.

Japan PMI manufacturing slipped to 49.4, resurgence in price pressures

Japan’s PMI Manufacturing dropped slightly from 49.8 in June to 49.4 in July, falling short of the forecasted 50.1. Despite this, PMI Manufacturing Output showed a minor uptick, climbing from 48.1 to 48.4. PMI Services saw a small decline, edging down from 54.0 to 53.9. Composite PMI, indicative of the overall health of the economy, was unchanged at 52.1.

Usamah Bhatti, an Economist at S&P Global Market Intelligence, highlighted that activity among private sector firms in Japan extended its growth streak for the seventh consecutive month. The persistence of this trend is largely attributable to steady and considerable improvement in service providers, while manufacturers reported a softer downturn at the dawn of Q3.

However, Bhatti underscored a less robust demand situation among private sector firms compared to the previous survey period. The latest data points to only a marginal increase in new orders, signaling a possible slowdown in demand.

Notably, the second half of 2023 has seen “renewed strengthening in price pressures” within the private sector. Pace of input price inflation has quickened for the first time since January. This trend is reflected across both manufacturing and service sectors, with both reporting steeper rates of output price inflation.

Australia PMI composite fell to 48, but still on narrow path for soft landing

Australia’s PMI Manufacturing recorded a mild uptick in July, rising from 48.2 to 49.6, marking a 5-month high, but still falling short of the expansionary threshold of 50. Concurrently, PMI Services took a downward turn from 50.3 to 48.0, hitting a 7-month low. Consequently, Composite PMI, a measure of combined sectors, dipped from 50.1 to 48.3, which is also a 7-month low.

Warren Hogan, Chief Economic Advisor at Judo Bank, attributed the soft July figures predominantly to a dip in business activity in the services sector, which had previously been on a recovery path in 2023. But the “Australian economy remains on the ‘narrow path’ for a soft landing.”

The July Flash report raised some concerns regarding inflation. Despite the slowdown in activity, price indicators trended higher, particularly within the services sector. These inflationary signals remain elevated, pointing to a potential inflation rate of around 4-5%, substantially exceeding RBA’s target of 2% to 3%.

Hogan noted that the disinflationary trend evident throughout 2022 “appears to have ceased”. As such, July figures will provide critical insights into whether Australia’s inflation aligns with the declining trends seen in other countries recently, or if the nation is “set to experience a more sticky inflation trend in 2023/24.”

NZ goods exports up 1.3% yoy in Jun, imports down -14% yoy

In June 2023, New Zealand’s goods exports observed a modest rise of 1.3% yoy, an equivalent of NZD 84m, taking the total to NZD 6.3B. Conversely, the nation witnessed a significant drop in goods imports by -14.0% yoy, or NZD -1.1B, reducing the total to NZD 6.3B. This left the monthly trade balance at a surplus of NZD 9m, notably below market expectations of NZD 235m.

A deeper look into the country’s top trading partners unveiled mixed outcomes in exports. June 2023 saw a decline in total exports to China by NZD -124m (-7.2% yoy), and to EU by NZD -98m (-20%). Moreover, exports to Japan also slipped by NZD -56m (-13%). On a positive note, exports to Australia and US increased by NZD 190m (30%) and NZD 91m (13%) respectively.

In terms of imports, there were notable reductions across the board. China, one of New Zealand’s principal import partners, witnessed a drop by NZD -232m (-16% yoy), while EU observed a decrease of NZD -100m (-9.2%). Furthermore, imports from Australia and US fell by NZD -93m (-12%) and NZD -96m (-14%) respectively. South Korea recorded the most substantial decline in exports to New Zealand, with a drop of NZD -136m (-26%).

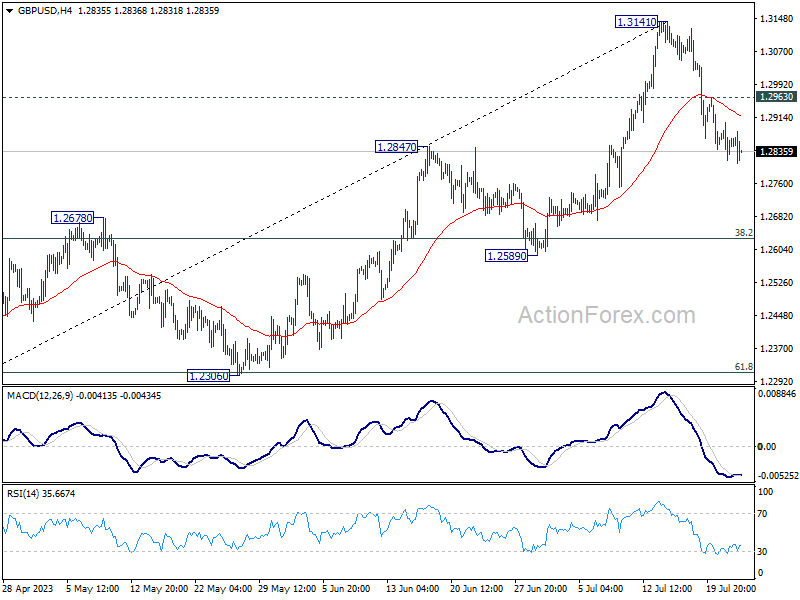

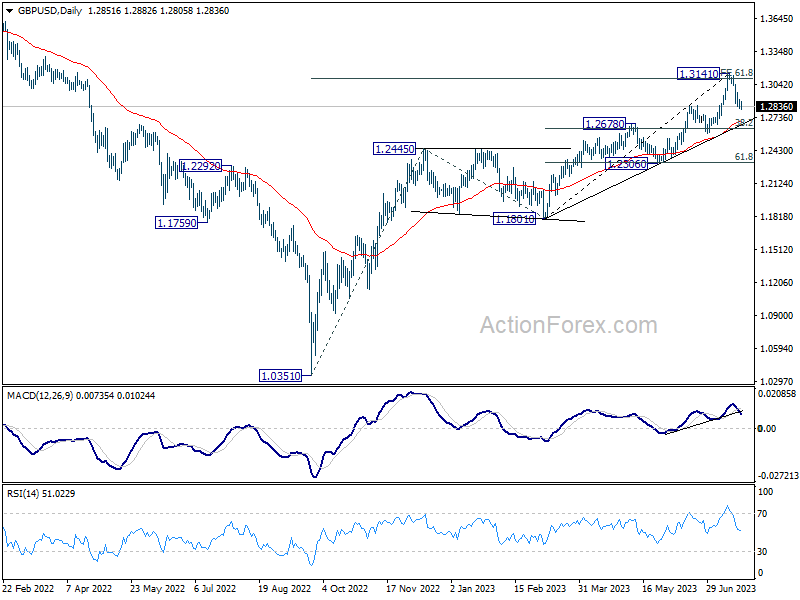

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2811; (P) 1.2858; (R1) 1.2899; More…

GBP/USD’s decline from 1.3141 short term top continued today and intraday bias remains on the downside. Deeper fall would be seen to 55 D EMA (now at 1.2697) next. On the upside, break of 1.2963 minor resistance will turn bias back to the upside retest 1.3141 high instead.

In the bigger picture, as long as 1.2678 resistance turned support holds, rise form 1.0351 (2022 low) is expected to continue. Next target is 100% projection of 1.0351 to 1.2445 from 1.1801 at 1.3895. However, sustained break of 1.2678 will argue that it’s at least correcting this rally, with risk of bearish reversal.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance NZD Jun | 9M | 235M | 46M | 52M |

| 23:00 | AUD | Manufacturing PMI Jul P | 49.6 | 48.2 | ||

| 23:00 | AUD | Services PMI Jul P | 48 | 50.3 | ||

| 00:30 | JPY | Manufacturing PMI Jul P | 49.4 | 50.1 | 49.8 | |

| 07:15 | EUR | France Manufacturing PMI Jul P | 44.5 | 46.1 | 46 | |

| 07:15 | EUR | France Services PMI Jul P | 47.4 | 48.4 | 48 | |

| 07:30 | EUR | Germany Manufacturing PMI Jul P | 38.8 | 41.2 | 40.6 | |

| 07:30 | EUR | Germany Services PMI Jul P | 52 | 53.1 | 54.1 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Jul P | 42.7 | 43.5 | 43.4 | |

| 08:00 | EUR | Eurozone Services PMI Jul P | 51.1 | 51.5 | 52 | |

| 08:30 | GBP | Manufacturing PMI Jul P | 45 | 46.1 | 46.5 | |

| 08:30 | GBP | Services PMI Jul P | 51.5 | 53.1 | 53.7 | |

| 13:45 | USD | Manufacturing PMI Jul P | 46.3 | |||

| 13:45 | USD | Services PMI Jul P | 54.4 |

{kind=link}